Another batch of emails from John Eastman, the conservative legal scholar at the heart of President Trump’s effort to overturn the 2020 election, have been obtained and published by Politico. This new exchange was between Eastman and Rep. Russ Diamond, a Pennsylvania state legislator, and provides further insight into the arguments and tactics that pushed us to the brink of a constitutional crisis.

In the emails, Eastman and Diamond discussed having the Pennsylvania state legislature (where Republicans held the majority in both chambers) decree a new set of “untainted” vote totals through some ridiculous mathematical gymnastics. In this plan, tens of thousands of votes would have been thrown out based on little more than guesswork, using prorated percentages across different categories of ballots. As noted by Phillip Bump at the Washington Post, even this proposed arithmetic would have resulted in Biden still winning the state.

Underlying the conspiracy theories and fuzzy math is a more serious and pernicious legal theory central to most of Eastman’s claims: that state legislatures have some constitutional power to overturn, alter, or “decertify” their state’s presidential election results. This theory is constitutionally erroneous and should be firmly rebuked as part of preventing future attempts at election subversion.

Cato at Liberty

Cato at Liberty

In a thought-provoking article published by the IMF in April, Ruchir Agarwal and Miles Kimball argue for moving away from a “paper money standard” and toward an “electronic money standard.” The promised benefits include shorter recessions and lower average inflation. These benefits are said to result from eliminating the “zero lower bound” to nominal interest rates, giving the Federal Reserve the power to cut nominal interest rates as far as it needs—even into negative territory—to spur recovery from a recession. Even if nominal interest rates are only 2 percent going into the recession, the Fed could cut rates by 5 percentage points (say), reaching ‑3 percent, if that’s what they think a prompt recovery requires. The ability to conduct a negative interest rate policy, Agarwal and Kimball (hereafter AK) argue, removes the need to have an inflation target well above zero in order to keep nominal interest rates high enough to allow 5 percentage points of rate-cutting.[1] It thereby encourages the Fed to lower its inflation target from 2 percent to zero.

The “zero lower bound” is created by the unlimited availability of a zero nominal return on currency: nobody will accept significantly negative returns when they can always get a zero return (or more precisely, zero minus a small cost of storage) by holding Federal Reserve Notes. Think of the scene in Breaking Bad where Walter and Skyler White survey a room-sized storage locker where they are keeping millions of dollars in stacks of $100 bills. A back-of-the-envelope estimate indicates that their storage costs were less than one-tenth of one percent per year. Under such conditions, the public will not accept bond returns more than one-tenth of one percent per year below zero.

Read the rest of this post →Related Tags

Over the last few months, a U.S. baby formula producer issued recalls both voluntarily and required by the Food and Drug Administration (FDA). These recalls are rocking the U.S. baby formula market leaving parents facing higher prices and bare shelves. Stores like Walgreens, CVS Health, and Target are limiting the number of formula products per purchase because of low inventory—just last month, national out-of-stock levels reached 40 percent!

One reason retailers are struggling to recover stock levels is the multifarious trade restrictions that limit infant formula imports. The United States subjects infant formula to tariffs up to 17.5 percent and tariff-rate quotas (TRQs); for TRQs some level imported are subject to a tariff with the excess subject to a tariff and additional duties. A few trading partners receive “special” duty rates where some infant formula imports are duty-free or receive lower tariffs and TRQs. Mexico is one of the few U.S. trading partners that has some duty-free access for infant formula, and uncoincidentally, is the top trading partner for U.S. formula imports. Though, in comparison to total imports from Mexico (worth almost $400 billion), formula imports are extremely low.

Figure 1 illustrates how little baby formula the United States imports compared to its estimated domestic consumption. While it may not seem bad (and is even encouraged by many nowadays) that the U.S. does not import much baby formula, it is important to understand why the United States is not importing baby formula—amidst the current scarcity, the inability to import is detrimental as parents are left with few to no options.

Absurdly, provisions were added to the United States-Mexico-Canada Agreement (USMCA) to restrict imports of formula from Canada, supposedly because China was investing in a baby food plant in Ontario, and this new production might eventually enter the U.S. market (heaven forbid!). Thus, the provisions in the USMCA’s agriculture annex establish confusing and costly TRQs on Canadian exports of infant formula, and the United States imported no baby formula from Canada in 2021.

Making matters even worse, infant formula is subject to onerous U.S. regulatory (“non-tariff”) barriers. For example, the FDA requires specific ingredients, labeling requirements, and mandates retailers wait at least 90 days before marketing a new infant formula. Therefore, if U.S. retailers wanted to source more formula from established trading partners like Mexico or Canada, the needs of parents cannot be quickly met because of these wait times. Businesses also have little incentive to go through the onerous regulatory process to sell to American retailers, given the aforementioned tariffs and the relatively short duration of the current crisis.

The European Union (EU) is especially noteworthy in this regard. Many parents demand formula from the EU not only because of the current scarcity but because European formula meets other preferences, including a perceived higher quality, and more varieties like goat’s‑milk-based formula. Technically, it is illegal to import baby formula from the EU for commercial purposes, but parents can (and do) import it for personal use. Recently, the FDA recalled some European infant formula because it did not comply with FDA labeling requirements. It is agreed by many medical experts that the differences between American and European formula are minor and are not worth the expense imposed by these regulations.

U.S. “marketing orders” for milk throw in another regulatory wrench. These laws cover multiple classes of milk and establish a system for dairy farmers with price and income supports, and trade barriers. The milkiness (ha) of the system makes it difficult to clearly conclude that these orders impact infant formula but given dry milk is a vital component, it can be inferred that these orders that we know raise the price of milk, distort economic activity in the dairy sector that could stymie U.S. producers’ ability to produce more formula to help make up for lost supply. And of course, the import barriers contained within the orders dampen U.S. producers’ demand for foreign classes of milk, including dry milk, thereby reducing options, which are needed most during domestic emergencies.

Congress may not be able to do much for the current crisis, but it should act now and consider how to liberalize trade in baby formula by working towards reducing the opacity of TRQs and marketing orders. Better yet, completely repealing both TRQs on baby formula and milk marketing orders could help prevent another formula crisis, and any regulations set by the FDA affecting formula imports should be out of necessity based on science. The unintended consequences that result from policies implemented in a vacuum illustrate once again, that protectionism promotes the opposite of resilience.

As if being a new parent isn’t hard enough!

Related Tags

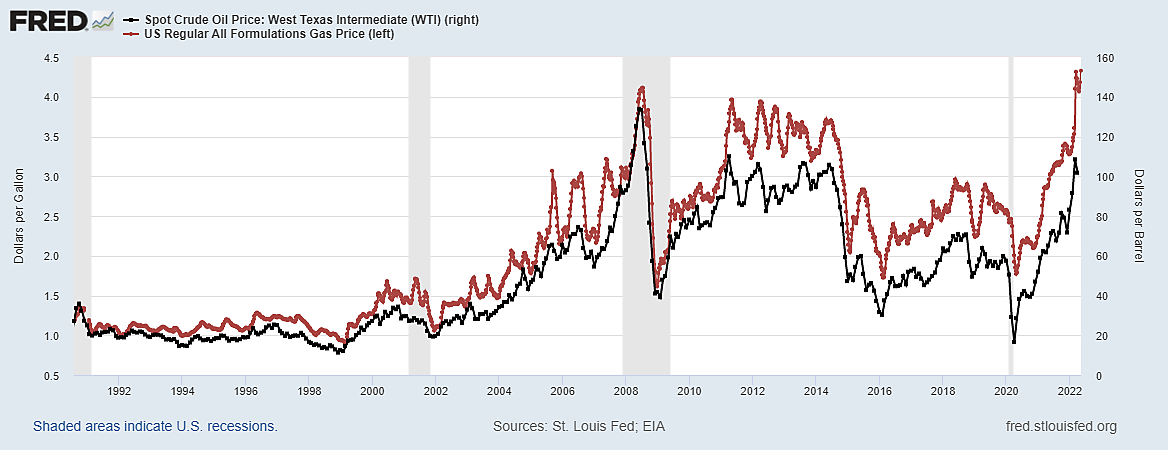

I still have a 1979 bookmark that says, “INFLATION IS A PAIN IN THE GAS.”

Funny but wrong. U.S. gasoline prices follow gyrations in world oil markets, which depend on global (not domestic) supply and demand.

What actually happened in 1978–80, an important German study from Bruegel reminds us, was the Iranian revolution and the Iran-Iraq War: “The 1978 Iranian revolution decreased global supply by 4 percent and led to a price increase of 57 percent. The 1980 Iran-Iraq war decreased global supply by 4 percent and led to a price increase of 45 percent.”

What happened to world oil markets in 2020 was a global pandemic, with falling oil and gas prices followed by a sizable loss of oil and gas production capacity in the U.S. and elsewhere. What happened in 2021 was mostly the phasing-out of governmental lockdown schemes which allowed production, commerce, and transportation to bounce back faster than oil and gas production could. China, however, has lately reverted to primitive lockdown schemes, which might lower world demand for oil and everything else by shrinking the Chinese economy.

What happened to crude oil and gasoline prices in 2022 was the Russian invasion of Ukraine, though partisans falsely deny the link between war and oil markets and instead blame President Biden for U.S. gasoline prices – which, as in 1979, are considered synonymous with “inflation.”

Recently, the oil futures market has been rattled by proposed EU sanctions intended to shrink the world supply of Russian oil.

The U.S. retail price of gasoline reached a record high of $4.37 a gallon yesterday, while global news pushed the price of WTI crude oil future down by 6.1%. The next day, “Crude oil futures were sharply lower in mid-morning Asian trade May 10, extending steep overnight declines,” due to “hurdles to an European Union-ban on Russian oil and the ongoing spread of COVID-19 in China.” The Financial Times noted, “Brussels has shelved its plans to ban the EU shipping industry from carrying Russian crude as it struggles to push through its latest sanctions package because of anxiety among some member states about the economic impact of the measures.”

The Bruegel study notes, “Such a measure would not prevent Russia from exporting altogether – it would find alternative buyers, such as China, India or others, as it already does – but an embargo would certainly increase the discount on Russian oil… If, on net, Russian exports decreased, the world price would go up, unless the drop in Russian exports was offset by the decisions of other producers, from Saudi Arabia to Iran to Venezuela, to increase production.”

Regardless of the net effect of a hypothetical EU ban on Russian oil, the fact that it suddenly appeared far less likely to happen was followed by lower world oil prices and higher prices for U.S. bonds and stocks. If the world (and U.S.) price of crude oil remains lower for a while, then U.S. gasoline prices will also turn down later.

Related Tags

Each country imagines inflation to be a national problem to be entirely blamed on national fiscal authorities or on each nation’s central bank. Yet March CPI inflation averaged 8.8% for all 38 countries in the OECD, and 7.8% for the 27 EU countries.

Economists at the Federal Reserve Bank of San Francisco, in the FRBSF Economic Letter, ask a narrower question: “Why is U.S. Inflation Higher Than in Other Countries?”

They first begin by acknowledging that there have been some uniquely huge global events driving world prices down in 2020 (COVID-19 lockdowns causing long-term loss of productive capacity) and other powerful forces driving global prices up since reopening in the Spring of 2021 – most recently the Russian invasion of Ukraine.

From April 2020 to February 2021 most states and nations imposed strict COVID-19 restrictions shutting down substantial capacity in production and distribution that could not easily be reversed, leaving a legacy of supply bottlenecks in everything from oil and semiconductors to toilet paper, pork bellies, and truck drivers.

After state and national economies reopened in the Spring of 2021, many prices snapped back from the pandemic-deflated base, contributing to big year-to-year percentage changes in monthly consumer and producer price indexes. Texas crude oil, for example, jumped from $16.55 a barrel in April 2020 to $61.70 in April 2021.

This year, the price of WTI crude oil began rising quickly from $80 in early January as Russia began amassing troops around and Ukraine to about $90 before the February 24 invasion and $108 in March. Prices of grains, metals, and natural gas also rose sharply as world supplies from Russia and Ukraine were slashed by the war itself and by U.S. and EU sanctions to thwart Russian sales. The U.N. World Food Price Index rose 1.4% in January 2022, 4.3% in February, and 6.3% in March.

Because such supply shocks increase global inflation numbers, the FRBSF economists begin their study by properly acknowledging that “Problems with global supply chains and changes in spending patterns due to the COVID-19 pandemic have pushed up inflation worldwide.”

However, they continue, “since the first half of 2021, U.S. inflation has increasingly outpaced inflation in other developed countries [defined by Canada and 8 European countries]. Estimates suggest that fiscal support measures designed to counteract the severity of the pandemic’s economic effect may have contributed to this divergence by raising inflation about 3 percentage points by the end of 2021.”

The most noteworthy finding of the FRBSF study is that last year’s relatively higher U.S. inflation was the result of last year’s fiscal policy –not monetary policy. Yet the U.S. Federal Reserve is being asked to somehow undo the hangover from last year’s fiscal excess by this year’s monetary squeeze. It would be hard to argue that U.S. inflation was higher last year because of an easier monetary policy than Europe since the Euro fell from $1.22 in January 2021 to $1.08 this April. Recent experience is the opposite of what happened as a result of the U.S. dollar devaluations of 1971–79.

Read the rest of this post →Related Tags

I know a lot of people get tired of “firsts”–first black this, first Asian-American that. But today’s papers report that Karine Jean-Pierre will be the first black person and first openly gay or lesbian person to be the White House press secretary, and that’s worthy of notice. (Also surely the first Martinique-born press secretary and quite possibly the first native French speaker.)

For roughly the first two centuries of American independence, no black or gay person and no woman could aspire to such a senior position. In 1993 Dee Dee Myers became the first woman to hold the press secretary job. It’s a mark of progress that such positions are increasingly open to every American. In The Constitution of Liberty, Hayek cited the 19th-century liberal phrase, “la carriere ouverte aux talents,” or “the career open to the talents,” that every person should be able to rise on the basis of their own talent and hard work rather than by inherited status.

This is not an argument for affirmative action, quotas, or even diversity as a goal in itself. I assume that the Biden administration selected Ms. Jean-Pierre to represent them to the media and the country because she was the best available person for the job. And it is to the administration’s credit, and to the credit of the country, that she was not rejected on the grounds of her gender, race, or sexual orientation. To be sure, I expect I’ll have ample reason to criticize the administration’s policies and her defenses of them over the coming months, but that’s a normal part of politics and policy in a democracy. And note that we say “first openly gay” because it’s quite possible there’s been a gay press secretary in the past, just not one who was open about being gay.

It’s a sign of progress that even young LGBT people may not find the appointment of a lesbian press secretary newsworthy. I had an exchange on Facebook last year with a young, married gay man who said, Who cares about somebody being the first openly gay person in the Olympics or whatever? Why not just admire his accomplishment and ignore his irrelevant sexual orientation? And I responded:

It’s news because for decades — or centuries — or more — it was pretty much impossible to be openly gay. And it’s still very rare for athletes. So that makes it news. And I hate to sound like the crotchety old gay guy yelling “you kids don’t appreciate!” But here I am. You and your husband can be happily, apolitically out because a few gay people came out when it was much more dangerous. Some of them lost their families, their homes, their jobs, their liberty, even their lives. So appreciate! And yeah, it may be that we’re past that time, and it shouldn’t be news any more. But as noted, it’s still rare among athletes. And there are still kids out there wondering if they’re the only one, if there’s something wrong with them. So thanks, Adam Rippon!

So that process of opening all the careers to the talents is still ongoing. First popularly elected black U.S. senator, 1967. First black woman in the Senate, 1993. First openly gay senator, 2013. First openly gay CEO of a Fortune 500 company, 2014. First openly gay Cabinet member, 2021. First woman president, TBD.

By the way, the New York Post has raised questions of a conflict of interest because Jean-Pierre’s partner is a CNN reporter. Well, welcome to the big leagues, LGBT people. LGBT relationships are as real as the marriages and domestic partnerships of heterosexual officials, and they can legitimately be subjected to the same scrutiny.

Progress happens. As I have written before, we have extended the promises of the Declaration of Independence — life, liberty, and the pursuit of happiness — to people to whom they were long denied. Classical liberals and libertarians have pressed for this sort of moral progress for more than two centuries. So raise a glass this evening to this small new bit of evidence that our society has become more open, more accepting, and more able to draw on the talents of every person.

Related Tags

In 2011, President Obama announced a goal of putting one million electric vehicles on the road. To this end, he twice went to Congress seeking funds for electric vehicle infrastructure. Both times, however, Congress demurred. Thus rebuffed, the Obama administration turned to other means to achieve his preferred policy. In late 2016, the Justice Department and the Environmental Protection Agency reached a partial settlement with Volkswagen over “Dieselgate,” which required the automaker to invest $1.2 billion on electric vehicle infrastructure—almost four times what the president unsuccessfully had sought from Congress. The upshot is that the Obama administration leveraged its prosecutorial discretion to perform an end-run around Congress’s power of the purse. More broadly, Obama’s EPA routinely resorted to these slush fund settlements to fund green energy projects, as I discussed in a 2017 study for the Competitive Enterprise Institute.

The Obama administration reached similar settlements in enforcement actions against financial institutions after the 2008-09 financial crisis. For example, as part of the Justice Department’s 2014 settlement with Citigroup, the bank had to pay $25 million to progressive non-profit groups. And in a $16 billion settlement with the government, the Bank of America agreed to pay $50 million to progressive non-profits. In return for making these payments, the banks faced smaller fines. In this manner, the Obama administration used regulatory enforcement to strongarm banks into rewarding political allies of the White House.

Lawmakers took note. During the 114th Congress, former Rep. Bob Goodlatte, who chaired the Judiciary Committee at the time, introduced the Stop Settlement Slush Funds Act. As should be evident from the bill’s title, the purpose of the legislation was to stop the executive branch from abusing its enforcement authority to fund pet projects. Rep. Goodlatte championed the bill in hearings, and, ultimately, the legislation won a comfortable majority in the House of Representatives. But the bill died on the vine in the Senate after Trump won the presidency.

To its credit, the Trump administration acted unilaterally to curb these slush fund settlements. In early 2017, then-Attorney General Jeff Sessions issued a memo that prohibited Justice Department lawyers from participating in settlements that involve third-party payments. In December of 2020, the agency codified the Sessions memo into the Code of Federal Regulations.

Alas, what can be done by one presidential administration can be undone by the next. On his first day in office, President Biden ordered the Justice Department to review his predecessor’s policy on third-party payments in settlement agreements. Yesterday, the agency complied with the president’s directive. Specifically, the agency issued an “interim rule” that rescinds the Trump-era policy. Although the rule is effective immediately, the agency is taking public comment on the measure.

What’s next? Well, it certainly seems that the Biden administration is keen on resuming the Obama-era practice of using regulatory enforcement to fund policy preferences outside of the legislative appropriations process. We’ll be paying attention to this space, so stay tuned.

If, as many expect, the next (118th) Congress features new majorities in both chambers, then perhaps lawmakers will revisit the Stop Settlement Slush Funds Act, versions of which have been introduced in the House and Senate by Rep. Lance Gooden (H.R. 5773) and Sen. Tommy Tuberville (S. 2079).

For more on these slush fund settlements:

- In 2016, I co-authored (with the Center for Class Action Fairness) a non-profit coalition comment letter on the proposed “Dieselgate” settlement with VW, which elaborates on the constitutional problems inherent to these slush fund settlements.

- Early last year, the Regulatory Transparency Project published an excellent report that explains the rise of this legal strategy during the Obama administration. (“Improper Third-Party Payments in U.S. Government Litigation Settlements”)