Each country imagines inflation to be a national problem to be entirely blamed on national fiscal authorities or on each nation’s central bank. Yet March CPI inflation averaged 8.8% for all 38 countries in the OECD, and 7.8% for the 27 EU countries.

Economists at the Federal Reserve Bank of San Francisco, in the FRBSF Economic Letter, ask a narrower question: “Why is U.S. Inflation Higher Than in Other Countries?”

They first begin by acknowledging that there have been some uniquely huge global events driving world prices down in 2020 (COVID-19 lockdowns causing long-term loss of productive capacity) and other powerful forces driving global prices up since reopening in the Spring of 2021 – most recently the Russian invasion of Ukraine.

From April 2020 to February 2021 most states and nations imposed strict COVID-19 restrictions shutting down substantial capacity in production and distribution that could not easily be reversed, leaving a legacy of supply bottlenecks in everything from oil and semiconductors to toilet paper, pork bellies, and truck drivers.

After state and national economies reopened in the Spring of 2021, many prices snapped back from the pandemic-deflated base, contributing to big year-to-year percentage changes in monthly consumer and producer price indexes. Texas crude oil, for example, jumped from $16.55 a barrel in April 2020 to $61.70 in April 2021.

This year, the price of WTI crude oil began rising quickly from $80 in early January as Russia began amassing troops around and Ukraine to about $90 before the February 24 invasion and $108 in March. Prices of grains, metals, and natural gas also rose sharply as world supplies from Russia and Ukraine were slashed by the war itself and by U.S. and EU sanctions to thwart Russian sales. The U.N. World Food Price Index rose 1.4% in January 2022, 4.3% in February, and 6.3% in March.

Because such supply shocks increase global inflation numbers, the FRBSF economists begin their study by properly acknowledging that “Problems with global supply chains and changes in spending patterns due to the COVID-19 pandemic have pushed up inflation worldwide.”

However, they continue, “since the first half of 2021, U.S. inflation has increasingly outpaced inflation in other developed countries [defined by Canada and 8 European countries]. Estimates suggest that fiscal support measures designed to counteract the severity of the pandemic’s economic effect may have contributed to this divergence by raising inflation about 3 percentage points by the end of 2021.”

The most noteworthy finding of the FRBSF study is that last year’s relatively higher U.S. inflation was the result of last year’s fiscal policy –not monetary policy. Yet the U.S. Federal Reserve is being asked to somehow undo the hangover from last year’s fiscal excess by this year’s monetary squeeze. It would be hard to argue that U.S. inflation was higher last year because of an easier monetary policy than Europe since the Euro fell from $1.22 in January 2021 to $1.08 this April. Recent experience is the opposite of what happened as a result of the U.S. dollar devaluations of 1971–79.

If the FRBSF study is correct that the cause of two or three percentage points of relatively higher U.S. inflation last year was COVID-19 relief spending, then the relatively good news (for the U.S.) is that those “pandemic response programs” ended last year and no longer subsidize consumer spending.

As Wall Street Journal columnist Greg Ip concluded, “U.S.-specific factors such as President Biden’s stimulus last year may explain only 1 to 2 percentage points of the rise in inflation. For the rest, we need to look to global factors” [emphasis added].

The U.S. and the world still have the ugly global price pressures of war and supply-chain disruptions to deal with. There is nothing that escalating Federal Reserve interest rates on bank reserves can do about war-related losses of energy and food, except to push the dollar up and thus make oil and grain imports more expensive in Euro, pounds, and yen than in dollars.

Instructive as it is, the FRBSF effort to explain 1 or 2 percentage point divergences from global average inflation demonstrates that such differences were minor compared with powerful global forces pushing all national inflation rates higher.

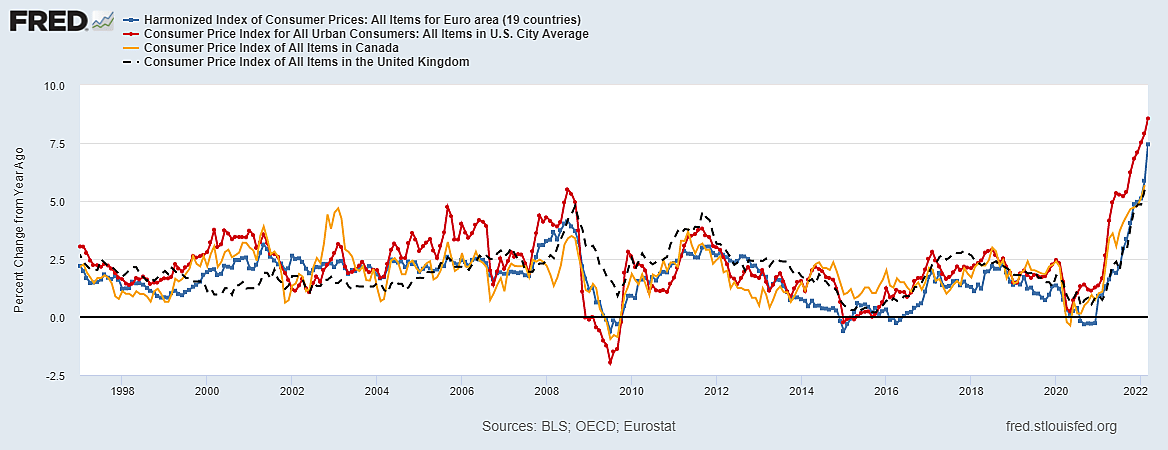

Exploring differences among national inflation rates was an interesting question last year. But the bigger question is not why national inflation rates among advanced countries differed by a few percentage points last year but why inflation movements among advanced economics are so remarkably similar over decades – sharing movements up, down, or sideways that look as synchronized as the legs of the Radio City Rockettes.

The graph compares year-to-year percentage changes in consumer prices in the Euro area, the U.S., Canada, and the U.K.

A large part of the explanation for national inflation rates moving up and down in similar waves is that consumer price indexes are greatly affected by big oil price spikes – such as 2008 and 2022 in this graph, but also 1973, 1980, 1990, and 2000. That is why many economists argue that if central banks try to fine-tune national inflation statistics they should focus on “core” inflation data which ostensibly excludes food and energy. Yet the core U.S. PCE price index slowed to a 3.5% annual rate in February and March before the Fed announced a series of interest rate hikes. And even core inflation rates are greatly affected by global prices of oil and natural gas which, in turn, affect farm and food costs.

“The bloody conflict in Ukraine is already driving food and energy prices higher,” notes former Fed Vice-Chairman Alan Blinder, “which will boost headline inflation in the coming months. Core inflation won’t be immune because food and energy prices seep into virtually all other prices, albeit in muted form. What product doesn’t include energy in its cost, either directly (to keep the lights on) or indirectly (via delivery trucks)?”

I wrote “Inflation is Largely a Global Problem” four years ago, but that point has become crucial today. The most obvious “global factor” shared among otherwise different countries is prices (in dollars) of internationally traded commodities, such as grains, crude oil, and natural gas.

Because household budgets are limited, a sustained increase in the cost of some important things (gasoline and meat) must eventually reduce the demand for and price of other things. A recent CNBC survey thus shows households with fairly high incomes cutting back sharply on spending. In the short run, however, the global surge in food and energy prices pushes every country’s headline inflation numbers higher.

Looking only at “core” inflation rates –as the San Francisco Fed study does– evades this year’s soaring food and energy prices that are getting by far the most attention from angry consumers, the media, politicians, and central bankers.

Soaring food and energy prices have been repeatedly emphasized by journalists and economists as the reason for urging the Fed and ECB to raise interest rates repeatedly to “end inflation” (in food and energy prices) and “lower the price at the pump.” But how are higher domestic interest rates and a soaring dollar supposed to lower global fuel and food prices, if not by generating a global recession?

Even global recessions have only ephemeral cyclical effects, with no predictable influence on longer-run inflation trends. Once recessions are underway, previous increases in central bank interest rates are always and everywhere followed by rapid reductions in central bank interest rates. We have often travelled this road before. Do we really need to take the same trip again?