The Wall Street Journal has published a biased news story regarding state budgets. The piece by Kate Davidson and David Harrison reflects only Keynesian thinking, exaggerates the plight of governments, and only quotes analysts in favor of more federal bailouts.

Here are some of the problematic aspects of the piece:

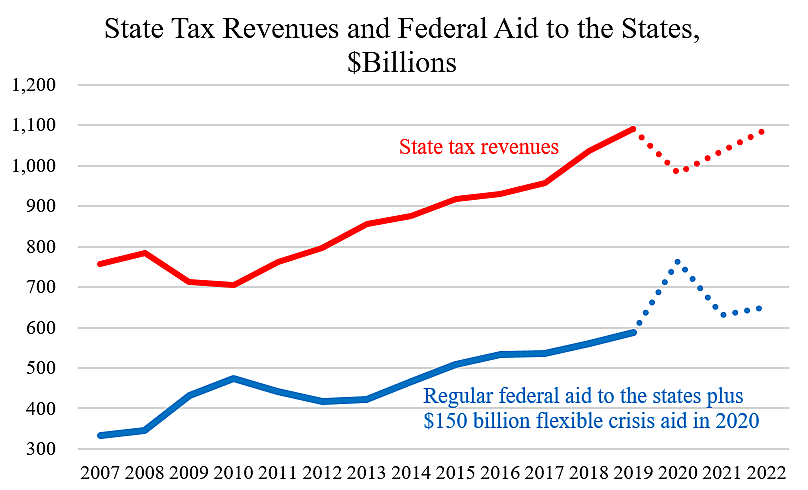

“State and local governments spent or invested $2.33 trillion in 2019.” That statement is false. The $2.33 figure is the state-local portion of GDP (BEA Table 1.1.5). But total state-local spending and investment in 2019 was $3.1 trillion (BEA Table 3.3).

“Michael Strain, director of economic policy studies at the conservative American Enterprise Institute, said Congress should take similar steps to fill the budget hole for state and local governments, which have seen revenues decline by 15% to 20% in some cases.” It is an error to conflate the budget situations of state and local governments. State governments may face a revenue decline of perhaps 10 percent, on average, but most local governments likely face little decline. Almost three-quarters of local tax revenues are from property taxes, and housing values remain buoyant so far during the recession. During the last recession, overall local government revenues did not fall for that reason.

The article cites analysts at liberal think tanks Brookings, TPC, and CBPP. It quotes a GOP senator who is one of the few Republicans in favor of another big state bailout. It quotes a scholar at conservative AEI who has a big-government view on this issue. And it cites Moody’s Analytics, which has a Keynesian economic model programed to show that government spending boosts GDP. Thus, the story cites six people in favor of another bailout and none against.

The article focuses on the most exaggerated estimate of state budget gaps, which is the Moody’s two-year figure of $500 billion. Why do they add two years together other than to produce a big-sounding number? The authoritative source of state budget data, NASBO, reports data on an annual basis.

The article includes a lower budget gap estimate by TPC, but excludes other recent lower estimates by Tax Foundation and economists Christos Makridis and Robert McNab. The Tax Foundation study shows that these three estimates are similar, and lower than the Moody’s outlier estimate highlighted by the WSJ.

The WSJ does not mention that the “gaps” and “shortfalls” it discusses are differences between pre-crisis forecasted revenues and current forecasts. If a state had forecast 2021 revenues to grow 5 percent but now expects 0 percent growth, the gap is said to be 5 percent and translated into dollars. The state would need to keep its 2021 spending flat to keep its budget balanced. That is not a crisis, especially after state general fund spending grew 5.5 percent in fiscal 2019 and 5.8 percent in fiscal 2020.

An alternative way to report budget gaps is to compare expected 2020 and 2021 revenues to actual peak 2019 revenues. That approach shows smaller gaps, as shown in the Tax Foundation study.

The WSJ article highlights Moody’s claim that without more federal aid, state budget gaps will “shave more than 3 percentage points off U.S. gross domestic product and cost more than 4 million jobs.” The Moody’s model reflects the Keynesian view that government spending boosts GDP. But other economists disagree. WSJ reporters might have interviewed Hoover Institution economists whose recent study found that cuts to government spending would boost GDP.

More broadly, Keynesian macro modeling ignores many microeconomic distortions caused by government spending that undermine GDP. I explore such distortions here. At minimum, reporters should note that the supposed stimulative effects that groups such as Moody’s claim are short-term impacts and do not include the longer-term costs of government spending.

The other day, WSJ publisher Almar Latour criticized “agenda-driven reporting” and said his paper’s “news coverage stands as a beacon.” I love the Journal and read it every day, but there is room for improvement in the news department.