Small businesses are the engine of the U.S. economy. Not only are they the primary generator of new jobs, but small businesses are also the incubators of innovation and the pipeline for future large businesses.1 The ability of small businesses to find capital is critical to their growth and operations. Entrepreneurs financially support their businesses in many ways, including by tapping into their own savings and borrowing on their credit cards. When they turn to outside financing, many entrepreneurs look to banks for loans. But many small businesses do not have the ability to secure a bank loan because they have no stable revenues or few assets for collateral. For those businesses, including ones that rely on intellectual property that is difficult for banks to evaluate, the equity markets are an important source of capital.

But tapping the equity markets can be difficult, especially for small businesses headquartered outside of major coastal cities or led by women or underrepresented minorities. That challenge is made more difficult by the complex web of regulations and exemptions that stand between an entrepreneur and raising capital in a securities market. Those regulations also limit the opportunities of most American investors to support small businesses through equity investment and prevent them from sharing in the potential high growth of startup firms. Taken together, these regulations mean that personal wealth often dictates the starting point for both entrepreneurs’ businesses and investors’ opportunities.

Congress can take action to support small business growth and individual investor opportunity by creating a micro-offering exemption for offers of equity securities and by increasing the pool of investors that can participate in private offerings.

The Problem

Many entrepreneurs struggle with navigating the complex equity capital–raising framework. As the Securities and Exchange Commission’s (SEC) Office of the Advocate for Small Business Capital Formation notes:

Even for the most technically sophisticated entrepreneur … the language of capital raising and the nuances of our complex rules are often inaccessible. Great entrepreneurial insight does not translate into fluency in almost a century of layered securities laws.… In other words: entrepreneurs who already find themselves cash-strapped must spend valuable—and often unavailable—resources just to understand their menu of options.2

These costs limit small business growth and economic development.

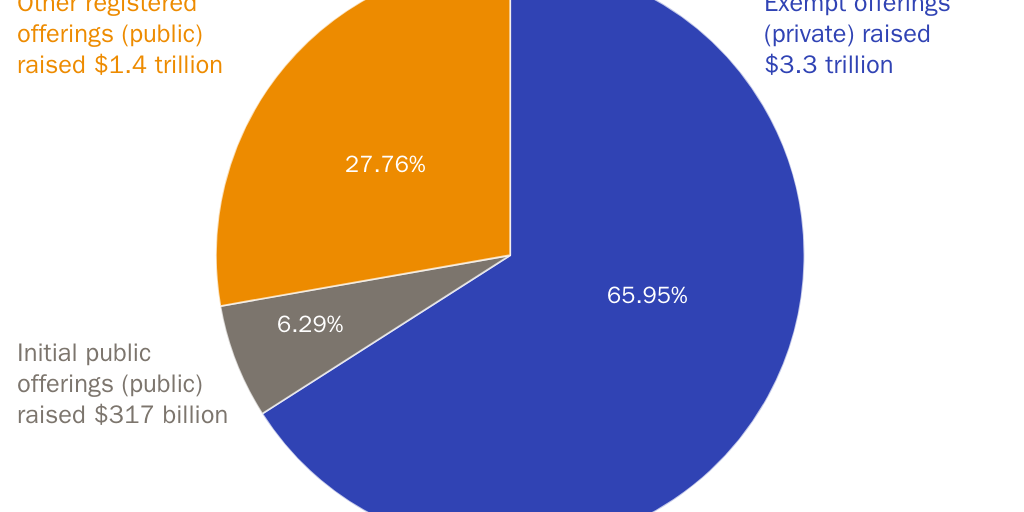

By default, securities offerings must be registered with the SEC, a complex and expensive process that includes detailed disclosures about an issuer’s business operations, financial condition, risk factors, and management, as well as audited financials. Most small businesses that seek to raise capital do so pursuant to exemptions from registration (see Figure 6). In theory, those exemptions offer a more simplified means of conducting a securities offering. But the exempt offering framework is far from simple. While legislative changes over the years, such as the Jumpstart Our Business Startups (JOBS) Act, have made equity capital raising more accessible to some investors, each new exemption and its implementing regulations have added another layer of complexity onto an already complex framework.

While equity crowdfunding, created by the JOBS Act, provided a somewhat streamlined method for entrepreneurs seeking to raise small amounts of equity capital, that process remains burdensome for the smallest entrepreneurs, who must meet a host of regulatory requirements and ongoing reporting obligations to take advantage of this exemption. The average equity crowdfunding capital raised in 2020 was approximately $309,000, and 40 percent of the entrepreneurs using crowdfunding were women or minorities.3 There is little sense—and there should be little regulatory interest—in imposing the SEC’s oversight where entrepreneurs seek to raise exceedingly small amounts of capital. This regulatory burden places a drag on small business development that may not be justified by any sort of investor protection interest.

Moreover, small offerings—for instance, in which an aspiring restaurateur or a couple of friends building an app ask their parents, family, and friends to get in on the enterprise with the hope of getting a cut of the profits down the road—still happen outside of regulated crowdfunding, without securities registration, and not pursuant to any existing exemption to registration. The issuer is often unaware of the need for securities registration, and the failure to follow the securities laws only complicates the process when an issuer grows and moves on to more formal methods of raising capital, often resulting in having to unwind those early investments.

The Securities Act of 1933 already recognizes that “the small amount involved or limited character of the public offering” may be an appropriate reason for the SEC to exempt such securities offerings from registration as “not necessary in the public interest.”4 But the SEC has not promulgated such an exemption. A statutory exemption would ensure that the smallest entrepreneurs would be unencumbered by securities regulations that are unnecessary for the protection of investors.

Where entrepreneurs seek to raise larger amounts of capital (i.e., those who typically look to raise money under the exemptions provided by Rule 506 of Regulation D), the general requirement that their investors be “accredited” harms both small business and investors. Regulation D offerings are popular; more than $1.9 trillion was raised through Regulation D offerings between July 1, 2020, and June 30, 2021, which exceeds the $317 billion raised in initial public offerings.5 But, currently, individual investment in these private offerings is limited to those with more than $200,000 in annual income or assets in excess of $1 million, along with a limited number of individuals who hold certain securities licenses. The SEC is considering recommending updates to the accredited investor definition and is expected to increase the wealth thresholds that an investor must meet to qualify.6

The accredited investor definition dampens small business growth by limiting the pool of investors available to entrepreneurs; that effect is borne disproportionately by would-be entrepreneurs in less wealthy communities, both minority and rural, who have fewer opportunities to recruit investors from the people closest to them.

This limitation on entrepreneurs is not offset by an investor protection benefit. Indeed, the focus on wealth does not protect investors from fraud, and it arbitrarily bars investors from certain offerings. Making the SEC the judge of who is and is not fit to invest subverts the federal securities laws’ disclosure regime that permits any offering to be made to the public if the issuer provides the right disclosures. In addition, these restrictions—especially when paired with reduced initial public offering volume and longer waits for companies to tap the public markets—can exacerbate wealth inequalities by limiting investment opportunities in potentially higher growth enterprises.

Solutions

While the entire exempt offering framework would benefit from an overhaul to reduce complexity and to make the equity capital–raising process more friendly for startups and small businesses, there are a few straightforward reforms that Congress can undertake to ease the path for small business capital formation.

- Micro-offering exemption. Congress should enact an exemption to securities registration for equity offerings that raise below a certain threshold, say $500,000 per year. Congress should direct that the SEC shall impose no other regulatory requirements on issuers that seek to take advantage of the exemption to ensure that entrepreneurs bear the minimum regulatory burden possible from the securities laws.

- Accredited investor. Congress should focus on decreasing the barriers to eligibility for accredited investor status. One way to do this is to consider investors who are advised by financial advisers who meet the current accredited investor definition as accredited themselves. This would resolve the inconsistency created by the SEC’s rules that recognize some advisers as sophisticated but do not permit clients to rely on that sophistication for investment advice. Congress could also consider permitting investors to self-certify as to their level of sophistication or permitting any investor to make investments up to a certain threshold of their portfolio or net worth.

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.