Competition improves people’s lives by pushing entrepreneurs to innovate and develop products that better satisfy customers, ultimately exposing weaknesses and inefficiencies in existing products. The financial sector is no exception. Competitive forces can reduce firms’ costs, expand consumers’ choices, and lower prices, thereby resulting in a more vibrant financial sector. Moreover, a more vibrant financial sector would complement a sounder monetary policy framework.

There are many ways for Congress to improve competition in financial markets, including leveling the current privileged position the U.S. dollar holds in competition with other potential means of payment. Two potential means of payment that have surfaced during the digital age are stablecoins and central bank digital currencies (CBDCs), both of which could affect competition in financial markets. At minimum, Congress should provide disclosure-based regulations for stablecoins while preventing the Federal Reserve from issuing a CBDC for retail customers, thus fostering innovation and competition in the financial sector.

The Problem

Strictly speaking, “digital currency” refers to electronic payments media that can pass directly and repeatedly from one digital wallet to another, much as paper currency can pass from one physical wallet to another. People thus would not need bank accounts to use and store their digital currencies. Consequently, digital currencies can allow even the unbanked—meaning those who can’t afford to keep bank accounts or who simply prefer not to deal with banks—to take advantage of the speed, convenience, and low cost of digital payments. This ability also means that digital currencies are a source of potential competition for existing financial firms, particularly commercial banks.

To date, digital currencies have not been used to the same extent as traditional government fiat currencies, but several innovations have surfaced to encourage their more widespread use. For instance, stablecoins are special cryptocurrencies designed to maintain a stable value rather than be subject to the volatile price movements seen with other digital currencies, such as Bitcoin and Ethereum. Although the details can differ widely, most stablecoins aim to achieve price stability by supporting their value with some other asset, typically cash and short‐term securities.1

A properly structured federal regulatory framework for stablecoins would likely spur innovation in financial markets, benefiting millions of people with faster and more efficient methods of payment. Yet, many in Congress and the Biden administration are advocating for a framework that would prohibit anyone other than federally insured depository institutions from issuing stablecoins, a type of framework that will discourage competition and keep payments innovations—and the companies that create them—out of the United States.2

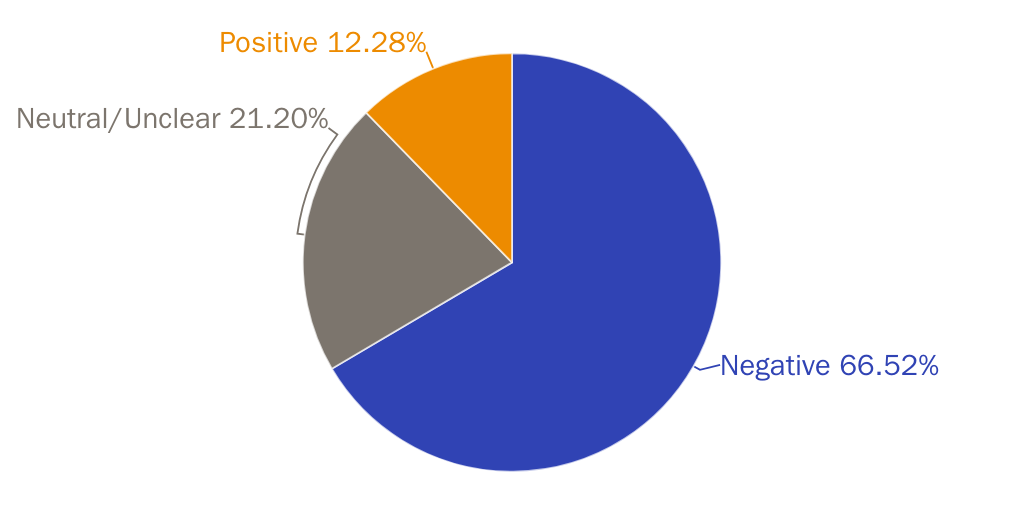

Many opponents of stablecoins—as well as some supporters—believe that CBDCs for retail customers could provide the same benefits as stablecoins.3 (Cato research shows that the majority of people view CBDCs negatively; see Figure 2.) While stablecoins are privately issued digital currencies, retail CBDCs would be issued by the Federal Reserve and consist of digital liabilities of the Fed that are widely available to the public. Thus, a CBDC could allow unbanked persons to transact digitally, if “unbanked” is understood to mean not banked by any private‐market depository institution. Put differently, a retail CBDC would be a government-issued method of payment that serves as a close substitute for a privately issued stablecoin.

The prospect of the Fed providing a close substitute for stablecoins or other electronic transactions is why Congress should make sure that the Fed never issues a retail CBDC. Some CBDC supporters argue that privately issued stablecoins can coexist with a CBDC,4 but this view is extremely short-sighted. Private firms cannot compete with a government entity that does not have to cover its costs, much less with the government agency that regulates them, and governments have tended not to tolerate monetary competition. It would be particularly difficult, for instance, for private stablecoin issuers to compete with a government-backed digital alternative that offers zero liquidity or credit risk to intermediaries and merchants. Ultimately, the existence of such a Fed-provided alternative would mean that the federal government, not privately owned commercial banks, would be responsible for issuing deposits.

The two payment methods—CBDCs and privately issued stablecoins—cannot peacefully coexist unless the government hands out special privileges or subsidies to privately issued stablecoins. Otherwise, private issuers could not compete with the Fed’s CBDC, an alternative that automatically comes with zero credit or liquidity risk. Moreover, the Fed’s current operating framework depends on paying interest to banks for their reserves, and there will be enormous political pressure for the Fed to pay individual CBDC holders at least the same rate of interest as it pays banks on reserves. This feature would raise the costs to private stablecoin issuers who would have to compete with government-provided interest, as well as the usual political economy concerns associated with government transfers of funds. Even if a CBDC is initially restricted to a small number of underserved users, there will certainly be political pressure to expand the pool of people using the CBDC, thus further disintermediating the private banking sector.

The fact that something called a CBDC even exists is only due to payment innovations that occurred in the private market.5 Congress should foster these innovations rather than protect the federal government’s privileged position and control over money. Aside from the direct harm to the private financial sector, retail CBDCs are also dangerous because there is no limit to the control that the government could exert over people if money is purely electronic and provided directly by the government. A retail CBDC would give federal officials full control over the money going into, and coming out of, every person’s account—a level of government control that is incompatible with economic and political freedom.

Solutions

The competitive process is, ultimately, the only way to discover what people view as the best means of payment. To foster competition in financial markets, Congress should work to lessen government regulation while ensuring that the Fed cannot issue a CBDC. Implementing the following recommendations would produce more competitive and vibrant financial markets.

- Create a disclosure framework for a limited purpose stablecoin issuer. Congress could create this type of regulatory framework for stablecoin issuers using several different approaches. Congress could, for instance, amend the Investment Company Act to create a limited purpose investment company. This narrowly defined company would then be subject to basic reserve requirements and mandatory disclosure of relevant information about reserve holdings. The most important detail is that the framework should be designed to regulate—through a disclosure regime—the reserves that stablecoin issuers claim to hold. An alternative would be to create a similar financial entity regulated by a federal banking agency, such as the Comptroller of the Currency.

- Require the Fed to grant master accounts to narrow stablecoin issuers. Currently, nonbank financial firms, including stablecoin issuers and other fintech companies, can only access the Fed’s wholesale services indirectly through bank correspondents. Instead of having the Fed enter the retail CBDC business, it should offer wholesale accounts and services to a broad set of stablecoin providers—and not just to insured banks and thrifts. Congress should amend Section 13 of the Federal Reserve Act to clarify that the Fed must grant master accounts to nonbank payments service providers, such as fintech firms that issue stablecoins backed exclusively by U.S. Treasury securities.

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.