(This post continues my discussion of the “regime uncertainty” hypothesis, according to which the New Deal hampered recovery by causing businessmen to fear policy changes that might render their investments unprofitable.)

Insull’s Monstrosity

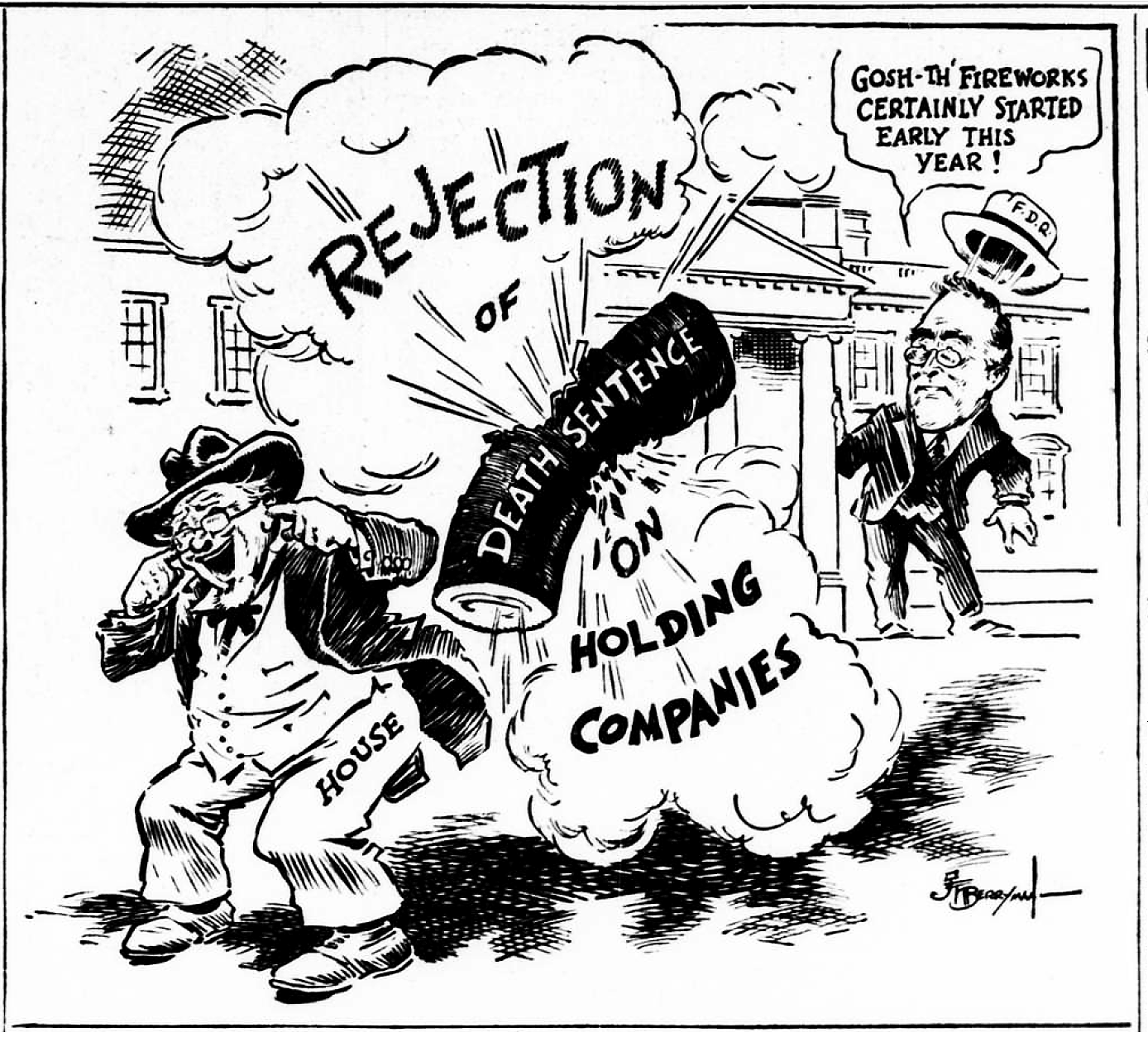

The 1935 Revenue Act wasn’t the only measure that had businessmen and investors shuddering that August. Less than a week after it became law, FDR signed the still-more controversial Public Utility Holding Company Act, granting the SEC the power to break up the nation’s utility holding companies.

On the eve of the Depression, Paul Mahoney explains, most U.S. electric and gas companies were directly controlled by trusts or holding companies. Groups of smaller utility holding companies were in turn controlled by a smaller number of larger holding companies, and so on for several layers. Three gigantic holding companies at the apex of this holding company “pyramid” ultimately controlled more than 80 percent of the nation’s power companies.

Until the Depression, the consolidation of the utilities industry awarded consumers and investors with falling electricity prices and robust returns. Even after the crash, utilities held up pretty well. Then, in June 1932, Insull Utility Investments, one of three holding companies at the top of the pyramid, failed, forcing many other holding companies to fail in turn. Some 600,000 utility shareholders faced huge losses.[1]

The Insull empire’s collapse turned Samuel Insull, its septuagenarian founder, into a symbol of the greed and corruption many blamed for the boom and bust. It also encouraged FDR, who had already crossed swords with utilities as New York’s governor, to make reforming them part of his New Deal. Roosevelt threw down the gauntlet during his September 21st Portland speech, assailing the “Insull monstrosity” and calling its business methods “wholly contrary to every sound public policy.”[2]

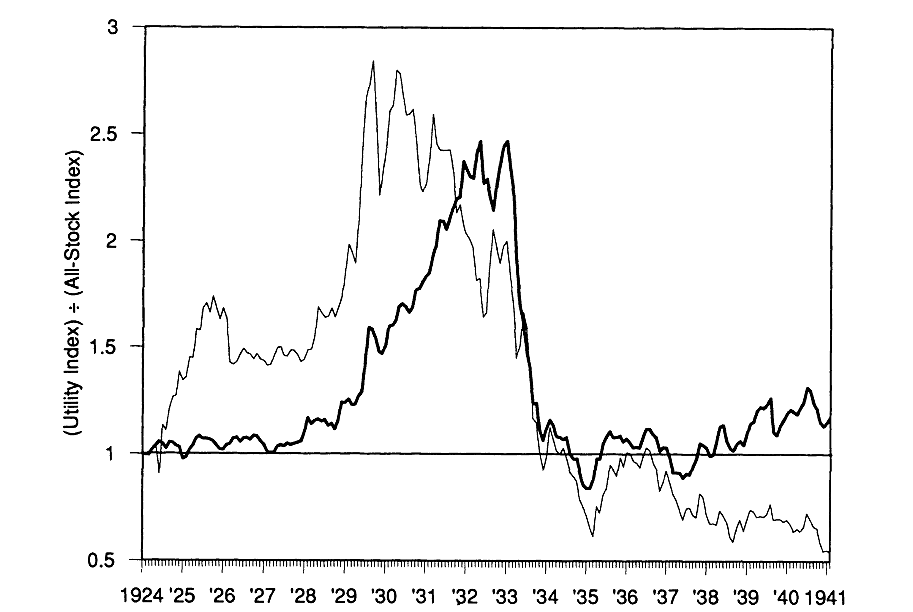

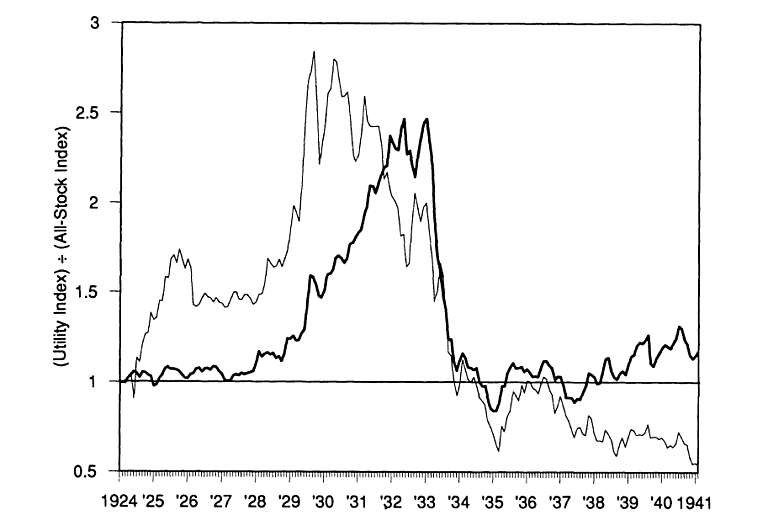

Roosevelt’s election left no doubt that a reform of the electric utility industry was coming. But no one knew just when, or what form it would take. Some New Dealers favored regulation; others wanted to ban utility holding company pyramiding, if not all utility holding companies. This uncertainty caused surviving utility share prices, which were still outperforming the market despite Insull’s downfall, to plummet, as can be seen in the chart below, from a 1992 article by William Emmons III.

Utility reform stayed on FDR’s back burner until July 1934, when he appointed a National Power Policy Committee to study the utility companies and propose legislation. The committee wouldn’t complete its report until late January, 1935. In the meantime, investors remained on edge, with many fearing the worst. In a January 19th column titled “Utility Baiting,” The Commercial and Financial Chronicle reported on what it called the “wholesale slaughter” of utility holding companies. “The attack of the Administration upon the utility industry,” it noted, “does not seem to abate with the passage of time.” Instead “the plans of the President to conduct a vigorous, and apparently an indiscriminate, attack upon utility holding companies [are] proceeding with dispatch.”

Read the rest of this post →