I periodically post TV interviews and the second-most-watched segment — edged out only by my debate with Robert Reich on Keynesian economics — was when I discussed how President Obama’s statist policies are bad for young people.

So there’s obviously some concern about the future of the country and what it means for today’s youth.

The Center for Freedom and Prosperity has examined this issue and taken it to the next level, cramming a lot of information into this six-minute video.

The video highlights four specific ways that government intervention disadvantages younger Americans.

1. Labor market interventions such as minimum wage mandates make it more difficult for young people to find employment and climb the economic ladder.

-

2. Obamacare harms young people by requiring them to pay substantially more to prop up an inefficient government-run healthcare system.

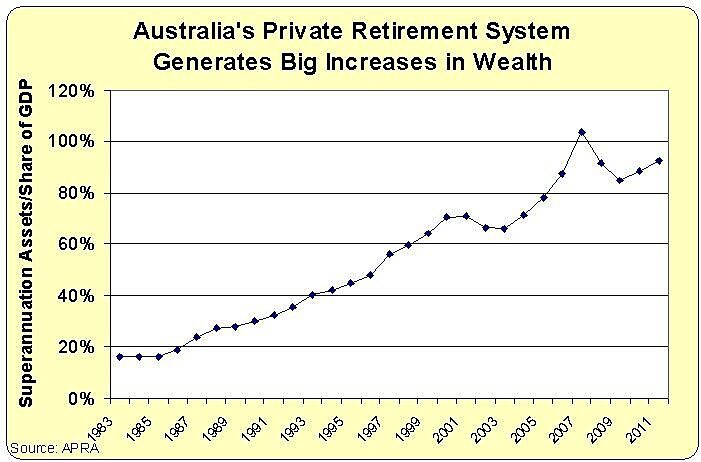

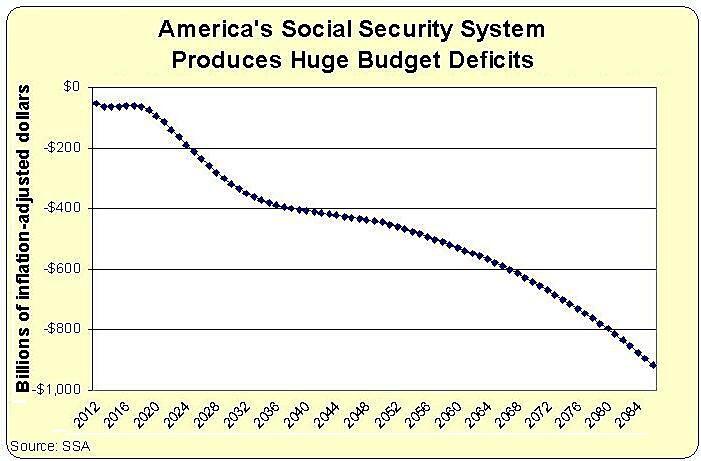

3. Young people are trapped in a poorly designed Social Security system and politicians such as Obama think the answer is to make them pay more and get less.

4. Government has created a major third-party payer problem in higher education, putting young people on a treadmill of ever higher tuition and record debt.

What makes this situation so surreal is that young people — as noted at the start of the video — are the one group who think the “government should do more”!

I hope you share this video with every young person you know and help them understand that statism is the enemy of hope and opportunity.

And maybe also show them this poster if they need some extra help grasping the problem.