Central bank digital currencies, or CBDCs, are on the rise. Around the world, governments are increasingly working toward developing and launching CBDCs. According to the Human Rights Foundation’s CBDC tracker, CBDCs have been launched in 11 countries and the 8 islands that compose the Eastern Caribbean Currency Union; CBDCs are being piloted in 39 countries, the Eurozone, and Hong Kong; and CBDCs are being researched in another 70 countries, the Economic and Monetary Community of Central Africa, and Macao.1 For its part, the United States is currently in the pilot phase. Yet, make no mistake, the United States does not need to launch a CBDC. Rather, Congress should explicitly prohibit both the Federal Reserve and the Department of the Treasury from doing so without authorizing legislation.

The Problem

Central bankers and other policymakers have increasingly focused on the prospect of CBDCs in recent years. What started as a theoretical concept quickly turned into reality when the central banks of China, Nigeria, The Bahamas, Jamaica, and the Eastern Caribbean Currency Union each launched CBDCs. Yet, these actions should not be replicated by the United States.

In the simplest of terms, a CBDC is a digital national currency that is a direct liability of the central bank.2 Like paper dollars, a CBDC would be a liability of the Federal Reserve. But unlike paper dollars, a CBDC would offer neither the privacy protections nor the finality that cash provides. In fact, it’s precisely this digital liability—a sort of digital tether between citizens and the central bank—that makes CBDCs different from the digital dollars that millions of Americans already use.

By establishing a direct connection from the government to each citizen’s financial activity, CBDCs risk ending financial privacy, restricting financial freedom, undermining free markets, and weakening cybersecurity.3 Whereas current financial surveillance is done through the private sector under government mandates, a CBDC would put the financial information of Americans on government databases by default. With so much data in hand, a CBDC would then provide countless opportunities for the government to control citizens’ financial transactions. Furthermore, with each dollar that is held as a CBDC, the financial system will lose funding that could otherwise be used to issue loans. Finally, with each person that begins to use a CBDC, the system becomes an increasingly lucrative target for cyberattacks.

The problems do not end there. Across the jurisdictions that have already launched CBDCs, governments have consistently struggled to increase consumer adoption. For example, in China, The Bahamas, and Jamaica, what little adoption has been gained is largely because the governments have given out money as either stimulus, lotteries, or discounts in CBDC. In Nigeria, the government even went so far as to orchestrate a cash shortage when the CBDC adoption rate failed to get above 0.5 percent.4 Yet even after the resulting protests and riots, CBDC adoption only increased to 6 percent.5

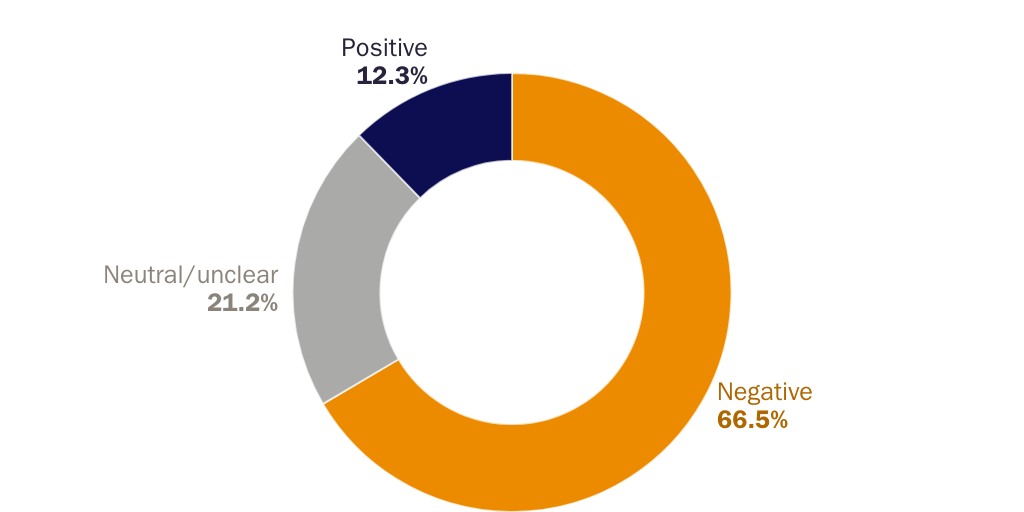

The public seems to recognize these problems. Cato Institute research found that 66 percent of respondents viewed CBDCs negatively when the Federal Reserve requested public feedback in 2022 (Figure 4).6 In fact, when the Cato Institute surveyed a representative sample of 2,000 Americans in 2023, the results were largely the same.7 After considering the costs and benefits of CBDCs, 74 percent of respondents said that they were opposed to the US government creating a CBDC.

Solutions

With these problems and the public’s concerns in mind, Congress does have several solutions at its disposal. At a foundational level, members of Congress should disregard the idea that there is a race to issue CBDCs. It may be easy to feel a fear of missing out when looking at international headlines, but the strength of the dollar has little to do with the technology that it’s moved on. Rather, the dollar’s status is owed to the strength of the American economy and its legal protections for private citizens relative to most other countries. Congress should focus on improving those underlying reasons—not on the latest craze in central banking—if it seeks to strengthen the role of the dollar.

- Prohibit the Federal Reserve and the Treasury from issuing a CBDC. Limiting the authorities of the Federal Reserve and the Department of the Treasury to explicitly prohibit either agency from issuing a CBDC would prevent the risk that a CBDC would be launched during a time of panic (financial or otherwise).8 Doing so would therefore prevent the risks to financial privacy, financial freedom, free markets, and cybersecurity that a CBDC would pose.

- Establish proper oversight of the Federal Reserve. The 2023 launch of FedNow—a Federal Reserve program for financial institutions to send and receive faster payments on behalf of their clients—showed that the Depository Institutions Deregulation and Monetary Control Act of 1980 lacks sufficient teeth to limit the Federal Reserve’s activities with respect to competing with the private sector. The legislation requires neither a formal cost-recovery period nor a third-party audit. In other words, the Federal Reserve—unlike its private-sector counterparts—does not have to worry about recouping costs and can avoid doing so to undercut the market. For example, the Federal Reserve revealed in late 2023 that it had spent $545 million to create FedNow and would continue to keep participation fees at zero dollars for another year to spur its adoption. To prevent the Federal Reserve from further encroaching on the private sector, Congress should amend the Depository Institutions Deregulation and Monetary Control Act of 1980 to strengthen the explicit requirement for the Federal Reserve to recover its costs when exploring new initiatives. Congress should also require that the Federal Reserve’s compliance with the Depository Institutions Deregulation and Monetary Control Act’s cost-recovery provisions be subject to regular audits by third parties.

- Strengthen financial privacy and reform financial surveillance. Financial surveillance seems to be expanding more each year, and it has some people looking for alternatives to the dollar. Congress should embrace the Fourth Amendment to the US Constitution and reform financial surveillance. To do so, Congress should consider revising the Bank Secrecy Act, eliminating the exceptions to the Right to Financial Privacy Act, strengthening the right to object to surveillance, repealing the surveillance permitted under 26 U.S.C. Section 6050I, requiring inflation adjustments for reporting thresholds, and requiring public reports on how information is used. See Chapter 1 for additional details.

- Welcome currency competition. Currency competition offers a much-needed check on government activities and is a source of inspiration for possible future improvements to the dollar. To encourage currency competition, Congress should clarify the application of legal tender laws (31 U.S.C. Section 5103), so people understand that legal-tender status does not require private businesses, persons, or organizations to accept United States coins and currency as payments for goods and services. Congress should also amend 18 U.S.C. Section 486, which forbids counterfeit coins and coins of original design. Finally, Congress should, at the very least, remove capital gains taxes where cryptocurrencies and foreign currencies are used for transactions.

Suggested Readings

There Is No Good Version of a Central Bank Digital Currency by Norbert Michel, Forbes (April 23, 2024)

Digital Currency or Digital Control? Decoding CBDC and the Future of Money by Nicholas Anthony, Cato Institute (2024)

CBDC vs. Crypto: What’s the Difference? by Nicholas Anthony, Cato at Liberty (blog), Cato Institute, (May 31, 2023)

Central Bank Digital Currency: Assessing the Risks and Dispelling the Myths by Nicholas Anthony and Norbert Michel, Cato Institute Policy Analysis no. 941 (April 4, 2023)

Congress Should Welcome Cryptocurrency Competition by Nicholas Anthony, Cato Institute Briefing Paper no. 138 (May 2, 2022)

Central Bank Digital Currencies Are about Control—They Should Be Stopped by Norbert J. Michel, Forbes (April 12, 2022)

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.