Climate change is an increasingly important consideration in trade policy. For instance, many countries try to limit their greenhouse gas emissions through domestic carbon pricing and regulatory schemes, and many trade agreements now include environmental provisions. In addition, some policymakers are looking to extend carbon pricing schemes to the international level. This has led to proposals for a carbon border adjustment mechanism (CBAM), which would tax the carbon emissions connected to the imported goods at the same rate as the carbon tax applied to domestic products.

The only example of a currently adopted CBAM is in the European Union, which began phasing in the policy in October 2023. Several members of the United States Congress have introduced legislation proposing border adjustments and carbon tariffs, but none have become law. However, neither the European Union’s CBAM nor any of the US proposals should be considered a true CBAM, and it is unclear whether they would comply with World Trade Organization rules.

While the idea of a government using taxes to protect the environment is established in economic theory, there are reasons to doubt that a CBAM would be effective at reducing emissions to mitigate climate change. Instead, these policies are likely to create uneven distributional effects on consumers as well as multiple pathways for rent seeking, cronyism, and protectionism.

Instead of imposing more taxes on trade, policymakers should pursue freer trade, which would provide opportunities to tackle excessive greenhouse gas emissions. Centuries of evidence have established that trade spurs economic growth, which contributes to cleaner environments. Therefore, the best path toward a cleaner and healthier world is to engage in freer trade and avoid enriching special interests through protectionism.

Introduction

Combating greenhouse gas emissions is not a new priority for policymakers. In 1992, the United Nations established an international treaty, the United Nations Framework Convention on Climate Change (UNFCCC), calling for scientific research and outlining a negotiating process to “prevent dangerous anthropogenic interference with the climate system.“1 In 1997, developed countries established the Kyoto Protocol, a set of legally binding obligations to reduce greenhouse gas emissions. Members of the UNFCCC built on the Kyoto Protocol in 2015 with the Paris Agreement, requiring all countries to set emissions-reduction pledges with the goal of holding the increase in the global average temperature below 2°C above pre-industrial levels.2 To meet this goal, the amount of greenhouse gases (GHGs) emitted into the atmosphere would have to equal the amount removed. Unlike the Kyoto Protocol, the pledges in the Paris Agreement are not legally binding.3

Now, partly in recognition that supply chains have globally integrated and emissions from production in one country can affect the whole world, policymakers are turning to interventionist trade policy to combat climate change. One of the more recent proposals is the carbon border adjustment mechanism (CBAM), which would impose a tax on the carbon emissions of imported products to provide “equal treatment” to domestic products subject to a national carbon tax.4

The only current example of a CBAM is in the European Union (EU), which began phasing in its CBAM in October 2023. In the United States, several members of Congress have introduced legislation for similar policies, including border adjustments and carbon tariffs, but none have garnered enough support to become law. The US carbon tariffs lack an accompanying domestic carbon tax, and the other US proposals and the EU CBAM differ in fundamental respects from a true CBAM, as will be explained later in this paper.

There are reasons to doubt that a CBAM would be effective at reducing emissions to mitigate climate change, while carbon tariffs would prove ineffective at achieving any such climate goal. Ultimately, a CBAM and similar proposals would likely be more costly than beneficial. They would have uneven distributional effects on consumers, raise major efficacy questions, and create multiple pathways for rent seeking, cronyism, and protectionism.

This paper explains the CBAM as proposed in the EU, examines several US proposals, and provides trade policy recommendations that could help achieve a cleaner and healthier environment.

What Is (and Isn’t) a CBAM?

A true CBAM is a carbon tax on imports that is equal to the carbon tax a country levies on its domestically produced goods. It includes a rebate for exports to countries with carbon pricing schemes to avoid double carbon taxation (i.e., taxation in both the home and export market).

Generally, a carbon tax is a tax levied on the emission of carbon dioxide or other GHGs during the production of a good or the GHG content of the good.5 The idea of a government using taxes to combat climate change can be traced to the work of British economist Arthur Pigou, who suggested using a tax to correct for a negative externality in his 1920 book, The Economics of Welfare. Consumption, production, and investment decisions by individuals and businesses often have indirect effects—sometimes good, sometimes bad—on those not involved in the transactions. These indirect effects or spillover effects sometimes fall into an economic category known as “technical externalities,” or simply “externalities.” Externalities are not reflected in the price of a good or service and are considered a form of market failure. Pollution, including the emission of certain GHGs, is the textbook example of a negative production externality—that is, a harm to a third party resulting from a good’s production.6

Pigou’s theoretical work proposes that the government might intervene to remove the “divergences” between social and private costs. That is, the tax would correctly price the activity causing the negative externality by capturing the cost imposed on those not party to the transaction. Put simply, taxing production that emits GHGs prices the GHG emissions and, in theory, should discourage (though probably not fully eliminate) their production, ultimately slowing climate change. (For more detail on correcting externalities, see the Appendix.)

According to CBAM advocates, the reason for taxing imports is to mitigate “carbon leakage” and thus minimize any potential increases in global GHG emissions. Carbon leakage can occur in two forms: First, businesses located in the carbon-taxing (or otherwise more stringently regulated) country could relocate production to a country with fewer regulations and lower taxes (including the lack of a domestic carbon tax). Second, businesses already located in less regulated countries (presumed to be dirtier) could win market share in the stricter countries because their goods might be less expensive than those produced by domestic industries that face a higher tax or regulatory burden.7 Many CBAM and carbon tariff policy proposals focus on goods that are considered carbon-intensive (e.g., oil, steel, and cement) because leakage of those products is thought to be the most harmful to the environment.

Currently, no CBAM proposals, including the EU CBAM, operate as a true CBAM, as explained later in this paper.8 Further, a charge on imports in excess of or without a corresponding domestic tax is not a CBAM; it is a protectionist carbon tariff.9 Most of the current US legislative proposals are for carbon tariffs, even though they refer to some type of “border adjustment.” A CBAM is intended to equalize the tax treatment between domestic and foreign goods and thus might not be considered protectionist or otherwise inconsistent with World Trade Organization (WTO) rules. However, a border adjustment on imports would not be necessary in the absence of a domestic tax that puts domestic producers at a competitive disadvantage. The border adjustment protects domestic industries deliberately burdened by domestic policies by making competing imports more expensive; therefore, it can be argued that a CBAM is protectionist.10

A CBAM is also not a tax applied to imports based on differences in regulatory standards, which cannot be easily quantified (and thus equalized). For example, a US tax applied to carbon-intensive imports from China based on differences between US and Chinese environmental laws and regulations is not a CBAM; it is a carbon tariff. The distinction between a CBAM and a carbon tariff is critical because the latter is a tax applied only to imports based on carbon content or intensity, putting imports at a competitive disadvantage in the market applying the tariff.11

Related Event

While the justification for carbon taxes is to correct for the perceived externality of pollution or climate change at the microlevel, advocates of CBAMs and carbon tariffs argue that these taxes would equalize the cost between domestic and foreign production. Since emissions are global, supporters of CBAMs and carbon tariffs purport that countries considered dirtier should pay to internalize the global costs associated with emissions. The next section analyzes the problems with some of the justifications for a CBAM and, by extension, carbon tariffs.

It Is Difficult to Justify a CBAM

There are serious practical concerns about a CBAM—its design, its scope, the politicization of such a tax, and its unintended consequences. CBAMs (and carbon tariffs) are often framed as necessary to maintain competitiveness as well as reduce emissions. Thus, implicit in the CBAM is the admission that domestic policies (such as carbon taxes) cause harmful economic outcomes that necessitate protection from imports not harmed in a similar manner. (There is also a vigorous debate about the efficacy of such domestic policies on GHG mitigation, but that is outside the scope of this paper.) A fundamental problem with CBAMs and carbon tariffs is that there is too much uncertainty in carbon accounting for any such tax to be administered appropriately or effectively. And, finally, in considering the implications of a CBAM or carbon tariff, the question of who is protected by such policies matters.

Why the Need for an Adjustment?

An important yet often overlooked consideration is whether the evidence supports that carbon leakage is a real, broad-based threat. While some policymakers seem to be rushing ahead with CBAM and carbon tariff proposals, few policymakers appear to have studied whether imposing carbon taxes (or environmental regulations) actually increases the risk that companies will move to more lenient jurisdictions or be put out of business by imports from “dirtier” countries.12

In theory, if a domestic carbon tax was so costly that it induced carbon leakage, then a CBAM could protect against leakage in multiple ways (all else being equal). First, it could offset the incentive for domestic companies to move carbon-intensive production abroad and export back to the home country, since those goods would be subject to the same tax regardless of where they were made. Second, a CBAM or carbon tariff would increase the price of foreign products and thus could discourage imports from those “dirtier” countries.

However, using a CBAM to mitigate carbon leakage is not as simple as described in the above scenarios. Because so many factors change, often in response to policies, it cannot simply be assumed that carbon leakage would automatically arise as a result of a carbon tax. For example, a business may struggle financially after the imposition of a carbon tax, but it may be too costly to relocate production offshore because of the firm’s sunk capital costs. On the other hand, it may relocate and maintain production and emission levels because it is still cheaper to pay the CBAM, particularly if other factors are cheaper abroad. It is also possible that a company is simply discouraged from relocating to another country because of non-economic factors such as institutional instability or corruption. All of this is to say, there are myriad considerations for both businesses and consumers, making it impossible to know if any single policy would cause—or fix—carbon leakage.

In fact, numerous studies have tried to estimate the rate of carbon leakage, with mixed results. The difficulty in isolating the effect of carbon leakage is understandable, as businesses are unlikely to move their production facilities to a foreign jurisdiction because of one single tax or regulation. Several analyses have found little evidence of such moves actually occurring. In the case of the EU, for example, a report from 2015 states, “To date there has been no compelling evidence that EU’s climate policies are forcing companies to move abroad and recent academic studies indicate that this is also unlikely to happen in the future even with a complete phase-out of free pollution permits.”13

A 2021 International Monetary Fund (IMF) working paper concludes that “there remains significant uncertainty with respect to carbon leakage as the existing literature provides at best little guidance for policy.” The authors note that a consensus has not been reached on the “approximate magnitude or even the sign of carbon leakage” (emphasis added).14 The IMF report’s authors also contend that the empirical literature on carbon leakage is limited by data and methodological issues.

It makes little sense to base a potentially damaging and far-reaching policy on an idea that lacks clear empirical support and scholarly consensus.15 On the other hand, it is clear that CBAMs and carbon tariffs can protect domestic industries from import competition. For example, the EU admits that part of its CBAM’s purpose is “to protect EU producers from foreign competition.”16 Aside from the fact that this statement implicitly acknowledges the potentially high cost of domestic carbon management policies, the question remains as to whether a border adjustment is applied for environmental reasons (i.e., to equalize the costs borne by domestic and foreign goods for the purposes of emissions mitigation) or political ones (i.e., to give domestic goods a competitive advantage).

Would a CBAM Properly Measure Emissions?

Another practical problem with a CBAM is that measuring emissions is not as straightforward as it may seem. For instance, one way the Environmental Protection Agency (EPA) tries to target emissions is through a concept known as “embodied carbon” (or embodied GHG emissions), defined as “the amount of GHG emissions associated with upstream—extraction, production, transport, and manufacturing—stages of a product’s life.”17 However, there is no standard methodology to calculate embodied carbon emissions, and even calculating domestic carbon emissions is different from “carbon embodied in goods and services consumed domestically.”18

The multitude of standards and frameworks also use different scopes (direct emissions, energy-related emissions, value-chain emissions), different origins (national, factory, bilateral, etc.), and different stages of production (finished goods, intermediate goods).19 Some of these scopes are easier to measure than others. For example, since there are already significant difficulties and differences in methodology for calculating embodied emissions at the industry level, the problem is even worse at the product level. Additionally, since carbon emissions are not readily observable, an administering agency must expend significant resources (time, money, manpower, etc.) intensely scrutinizing the measurement, validation, and auditing of product-level emissions data.20

The choice of methodology is not merely a technical or theoretical concern but one that could have major implications for the efficacy of emissions mitigation. For example, adopting a national- or industry-level emissions standard (and thus national- or industry-level taxes on imports) might make administration of a CBAM relatively easy, but by applying the same tax rate to goods regardless of their actual embodied emissions, this approach could encourage dirtier production in the country at issue. If, for example, goods from a more carbon-intensive factory are cheaper to produce yet subject to the same tax as those from a cleaner, costlier factory, the carbon-intensive goods would be more price-competitive than the cleaner goods in the jurisdiction applying the border measure. Factory-specific calculations, on the other hand, would avoid this distortion but are far more difficult, invasive, and subject to abuse by “captured” administering authorities.

Furthermore, since there is no clearly accurate methodology for calculating embodied carbon, even at the factory level, it is uncertain that a CBAM would actually equalize carbon taxes on imports and domestic products. Even with the same tax rate, for example, the carbon content of imports might be measured differently from domestically produced goods.

Related Event

Finally, small- and medium-sized businesses without the resources to calculate the intensities of their products (and fight against miscalculations) would be put at a disadvantage vis-à-vis larger firms that could more easily keep track of the different approaches and would likely pay compliance costs to increase their market share. Companies in the EU have already been vocal about the complexity of the EU’s CBAM emissions reporting and methodology. The burden falls much more heavily on small businesses. Imports valued at more than 150 euros must be reported, thus, for those companies importing in small batches, the regulatory cost is significant.21

Would a CBAM Be Consistent with WTO Rules or Invite Retaliation?

Carbon border measures also raise concerns regarding consistency with member governments’ WTO commitments. Specifically, a measure could run afoul of provisions under the General Agreement on Tariffs and Trade (GATT) and WTO Agreement on Subsidies and Countervailing Measures (SCM Agreement) that prevent members from

- discriminating among different members (the “most-favored-nation” principle of GATT Article I),

- applying tariffs on imports in excess of agreed “bound” levels (GATT Article II), treating imported goods worse than the same domestic goods (the “national treatment” principle of GATT Article III), and

- subsidizing exports (SCM Agreement Article 3).

Measures that violate these provisions, however, might be permitted where they qualify for one of the “general exceptions” of GATT Article XX, namely those that allow for measures necessary to protect human, animal, or plant life or health.22

Some legal scholars believe that a true CBAM would comply with WTO rules or meet one of the general exceptions as long as the measure meets three conditions:

- The domestic carbon tax applies equally to domestic goods and imports.

- The import tax is calculated in the same way for all WTO members.

- Any rebates on exports do not exceed the amount of carbon tax paid or applied to those goods.

Other scholars disagree with this conclusion, but the general view is that the border adjustment would in this case resemble domestic taxes (e.g., sales taxes or value-added taxes) applied to imported goods and widely considered to raise no serious WTO concerns.23

The same conclusion, however, cannot be said for any other type of carbon border measure, including the EU’s CBAM or a carbon tariff. In particular, most scholars believe that a carbon tariff without a corresponding domestic measure would violate several WTO rules and not qualify for any general exception because there are less protectionist measures available to achieve the same public policy objectives. Scholars also disagree as to whether the EU’s CBAM—described more fully in the following section—would be fully compliant with WTO rules.24 For example, former WTO Appellate Body chairman (and Cato Institute adjunct scholar) James Bacchus wrote in 2021, “Without revision and without careful application, the EU’s proposed CBAM may turn out to be inconsistent with fundamental WTO rules, and it may not qualify for one of the general health or environmental exceptions permitted under the WTO treaty.”25

Regardless, a CBAM or carbon tariff is intended, at least in part, to protect domestic industry and could therefore provoke retaliation from foreign trading partners who see the measure as WTO-inconsistent protectionism and are unwilling to wait for a WTO dispute-settlement panel to rule otherwise. For example, India’s Commerce Ministry is exploring retaliatory measures; at the WTO’s 13th Ministerial Conference in February 2024, India brought formal complaints about the EU’s CBAM.26 The commerce minister raised concerns about “the increasing use of trade protectionist unilateral measures, which are sought to be justified in the guise of environmental protection.”27 Other countries, including Brazil, China, and South Africa, are vocal opponents of the EU’s CBAM.28 It seems the EU is attempting to preemptively safeguard against such disputes by noting that its CBAM methodology may be “refined” before its official starting period in 2026.29

Would a CBAM Invite Rent Seeking and Abuse?

US history demonstrates that protectionism often attracts interest groups seeking to win additional and unwarranted financial support from the government.30 Successful lobbying efforts can turn even well-intentioned laws and regulations into corrupt vehicles for blocking fair competition and delivering favors to certain domestic businesses and workers. As a result, businesses will expend more effort on lobbying federal agencies and less effort on satisfying their customers. Competition to do business with consumers will increasingly become competition for government favor, in a practice called rent seeking. And, instead of acting as independent arbiters advancing the public interest, US agencies that deliver these rents can become “captured” agents of the most sophisticated or well-connected firms.

President Donald Trump’s Section 232 tariffs on steel and aluminum, which have been continued by the Biden administration, are a current example of how protectionist rent seeking works.31 Ostensibly implemented to protect US national security, the tariffs cover goods (e.g., low-value commodities made by close allies) with no legitimate defense or security nexus and were implemented against the recommendation of the US secretary of defense. The tariffs delivered a massive financial windfall to the domestic steel-producing firms that championed them (firms with strong personal connections to the Trump administration and longstanding clout in Washington). However, the steel industry’s windfall profits came at the expense of American steel-consuming companies, which had to lay off workers, raise prices, reduce production, or decrease investment.32 Meanwhile, the exclusion system implemented in the tariffs’ wake, which allowed some steel-consuming firms to avoid the tariffs, was, per a 2019 US Department of Commerce inspector general memorandum, “neither transparent nor objective” and raised concerns about “the appearance of improper influence in decision‐making.”33

The same risks would apply to a US carbon border measure. Firms produce and consume carbon at different volumes, all firms compete with others, and all possess varied ability to pass on higher costs to consumers. Thus, a carbon tariff system or CBAM could serve as a vehicle for protecting special interests—not the environment—at the expense of American businesses, consumers, and the economy more broadly.34

Emissions Are Global, and Unilateral Approaches Invite Free Riding and Trade Diversion

Because the effects of climate change are global, the result of one country adopting a carbon tax—even with a CBAM—is minimal.35 “Free riding”—where some countries bear the costs, for example through regulatory schemes, and others take no action and enjoy any accompanying environmental improvements—would result unless all countries agree to implement the same policy and enforce it uniformly.

This free-riding problem would exist even if multiple countries entered an agreement (such as a carbon club) to lower emissions and implemented border measures on imports from countries outside the club.36 In that case, multinational producers with multiple production sites could reorient their trade and supply chains to avoid tax liability: one system for within-club trade and another for everyone else. In the end, this trade diversion and circumvention would create a fragmented world with cleaner imports traded to some areas and dirtier imports traded to others, resulting in likely the same (if not worse) global emissions. It is also important to consider that higher tariffs that change trade patterns would be most harmful to the poorest countries as well as people in the lowest income brackets in richer countries, thus hindering their development and progress up both the environmental and prosperity ladders.37

For all these reasons, the ability to use a tax to correct for spillovers from production, thus lowering global GHG emissions, is questionable. Policymakers should be wary of implementing a tax (or any policy) that is based on weak theoretical foundations and practical difficulties. It might not achieve its main goal—reducing emissions—but it is certain to limit people’s freedom and damage their capacity to prosper. The next section bolsters this prediction by analyzing the EU’s emissions trading system and its new CBAM.

The EU’s CBAM Aims for—and Misses—Carbon Neutrality

In December 2019, the EU announced its Green Deal, a roster of policies intended to achieve carbon neutrality by 2050.38 The Green Deal includes numerous funding mechanisms to “make the EU’s climate, energy, land use, transport and taxation policies fit for reducing net greenhouse gas emissions by at least 55% by 2030, compared to 1990 levels.”39 This goal inspired the “Fit for 55” banner the European Commission embedded in its legislative package to the European Council.40

This package proposes various new laws to align current EU laws with the climate ambitions outlined in the Green Deal.41 One of these laws is a CBAM, and on October 1, 2023, the EU entered the transitional phase of replacing part of its emissions trading system (ETS) with its new “landmark” CBAM.42

The EU’s Emissions Trading System

In 2005, the EU was the first jurisdiction to establish an ETS, and it remains the largest international ETS in the world. The EU launched its ETS to allocate GHG emissions allowances to companies, and the system has undergone numerous revisions, with the most recent round in 2018. Generally, the system functions through a “cap and trade” mechanism. Under this approach, the European Commission caps overall GHG emissions for the EU and grants allowances—basically permits—to companies to emit a certain amount of GHGs. The Commission decreases the number of permits each year, thus incentivizing companies to lower emissions.

At the end of each year, firms must surrender a quantity of their allowances by a specific date to compensate for their emissions.43 If a company emits more than is permitted, it must acquire more allowances, either at an auction or directly from other companies. If companies emit less than the amount they are permitted, they can bank the excess for the future or trade the extra allowances.

Related Media

The ETS is strictly enforced: If companies do not comply with the cap, the European Commission imposes significant fines.44 The Commission also grants authority to member state agencies to collect GHG data from companies and issue their own fines if firms are noncompliant. Companies may be fined for various types of noncompliance, including exceeding the allowance, failing to report according to the rule, and underreporting emissions. In 2006, the food processing company Mars was penalized for not surrendering allowances on time.45

Under the ETS framework, the EU provides some allowances free of charge to prevent carbon leakage. Ironically, it provides such allowances to industry sectors explicitly “at risk … due to the EU ETS.”46 In other words, the EU acknowledges that the ETS places a high-enough burden on some firms that they are at risk of moving to less regulated jurisdictions. The industries are classified as “at risk” based on “the impact of production costs as a proportion of gross value added, and trade exposure as the ratio between the value of trade to countries outside the European Economic Area (EEA) (exports and imports) and market size within the EEA.”47 However, since carbon leakage from policies like the ETS is not guaranteed to occur, the “free” allowances could undermine GHG emissions mitigation.

Transitioning to the CBAM

According to the EU, the CBAM will complement the ETS system but not replace it. The CBAM will eventually replace the free allowances currently granted to EU producers over a transition period.

The EU’s CBAM is not a true CBAM for several reasons. First, the EU does not have a domestic carbon tax. Instead, the certificates sold under the EU ETS act as a domestic carbon price. The EU CBAM also does not include export rebates. As noted above, because the EU uses an emissions trading system instead of a carbon tax, it is unclear whether the EU CBAM—in its current form or with any future introduction of export rebates—will be compliant with WTO rules.48

Initially, the EU will apply the CBAM to imports of cement, iron, steel, aluminum, fertilizer, electricity, and hydrogen.49 Those industries are “deemed at greater risk of carbon leakage.”50 The border adjustment tax will equal the cost of an allowance paid by European producers. That is, for European producers that pay for allowances, the cost of an allowance is treated as equal to a domestic carbon tax.51 For those European producers that currently receive free allowances, the CBAM will not apply to the corresponding imports until those allowances are phased out.

European importers will need to report the embedded GHG emissions in their volume of imports; data collection requirements for the “transitional period” began in the fourth quarter of 2023. These reports had to be submitted by January 31, 2024, and the last report of the transitional period is for the fourth quarter of 2025 (submitted by January 31, 2026).52 The reports, submitted electronically, will be managed by the European Commission and must include the following information:

- The type of goods as identified by their Combined Nomenclature code.

- The quantity of imported goods and the direct and indirect emissions embedded in them.53

- Any carbon price already paid abroad for the emissions, including the carbon price paid for any precursor material embedded in the final product.

- The country where a carbon price is due.

- The country of origin of imported goods.

- The identity and location of the installations where the goods were produced.

- The production routes used for the manufacture of the goods.54

Once the CBAM officially starts, importers must submit reports on an annual basis that declare the quantity of goods imported and the embedded GHGs for the preceding year.55 Both government officials and companies have already called this a cumbersome task.56 Once the CBAM is officially operational, the number of covered goods will increase gradually. Currently, the EU’s plan is to phase in these products in direct proportion to the reduction in the ETS free allowances for the same sectors. The free allowances are scheduled to be phased out completely by 2035.57 Unless—and until—the EU follows through on eliminating the free allowances, the CBAM cannot be said to fully equalize the treatment of the imports and domestic goods. Put differently, the CBAM will fully equalize the treatment for certain products only.

US Proposals Targeting Imports and Carbon Emissions

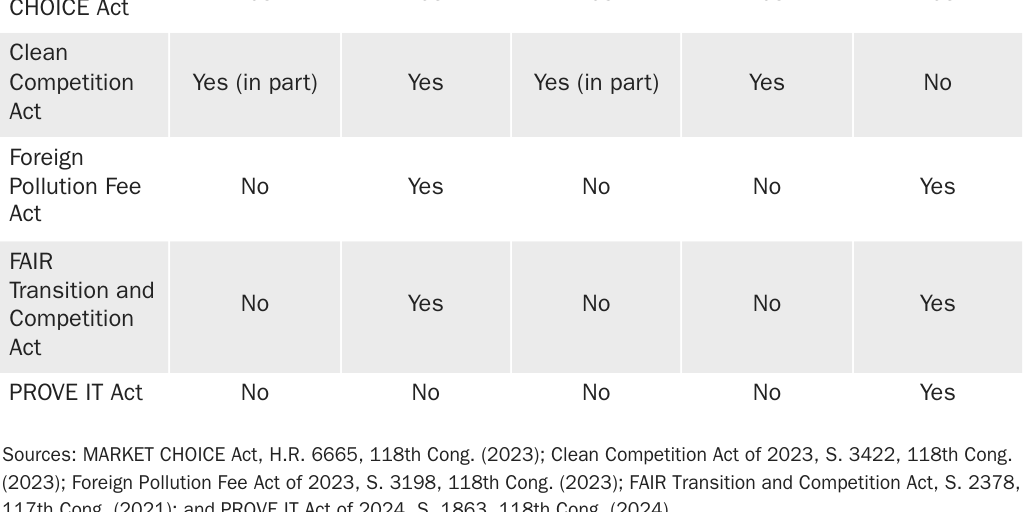

US proposals targeting trade-related carbon emissions range from comprehensive measures that approach a true CBAM to protectionist carbon tariffs and narrower emissions reporting and transparency measures. This section and Table 1 summarize these measures and their problems.

Almost a True CBAM

The MARKET CHOICE Act (Introduced 12/07/2023)

The Modernizing America with Rebuilding to Kickstart the Economy of the Twenty-First Century with a Historic Infrastructure-Centered Expansion (MARKET CHOICE) Act, introduced by Reps. Brian Fitzpatrick (R‑PA) and Salud Carbajal (D‑CA), is close to a true CBAM because it imposes a domestic carbon tax, a border adjustment, and export rebates. The bill would replace federal excise taxes on motor and aviation fuels with a tax on GHG emissions from fossil fuels and other sources. For 2025, the replacement GHG tax would be set at $35 per metric ton of carbon dioxide–equivalent emissions paid by producers at the facility level. The bill explicitly lays out that for each year after 2025, the tax would be calculated as the amount equal to the previous year’s tax “plus the sum of 5 percentage points, plus a percentage increase in the previous year’s tax rate equal to the increase in the Consumer Price Index for the previous calendar year.”58

The bill includes a schedule for emissions targets whereby each year the treasury secretary and EPA administrator would report the taxed emissions to determine whether the cumulative amount of annual emissions exceeded the targeted levels. The bill also includes a penalty of $4 per metric ton if the cumulative carbon dioxide emissions surpassed the amount specified for that year.59

A CBAM would be applied to imported covered goods equivalent to the amount of tax paid by domestic producers for “comparable domestic manufactured goods.”60 A rebate would also be included for US exports. However, the MARKET CHOICE Act is not a true CBAM because the rebates would not be offered to US producers exporting to countries with carbon pricing schemes. Instead, the rebates would be offered to eligible industrial sectors as determined by the treasury secretary based on GHG intensity and an arbitrary trade intensity of at least 15.61

Other provisions in the proposal include revenue recycling, particularly for the Highway Trust Fund, which is funded by the federal gas tax, and tax credits for consumers that pay state governments for GHG emissions.62 The bill also includes refunds to domestic manufacturers that “can demonstrate … that the fossil fuel has been transformed via the manufacture of the product so that the … emissions will be reduced or eliminated over the product’s lifetime.”63 Refunds would also be offered for carbon capture and storage.

Finally, the MARKET CHOICE Act includes a “moratorium on federal regulations relating to GHG emissions.” After the tax is collected by the Department of the Treasury, the bill requires a 12-year moratorium on EPA regulations to limit GHG emissions.64 However, the EPA could revoke the moratorium early in certain instances and otherwise would maintain its authority over GHG emissions.

Clean Competition Act of 2023 (Introduced 12/06/2023)

The Clean Competition Act, introduced by Sen. Sheldon Whitehouse (D‑RI) and Rep. Suzan DelBene (D‑WA), is also close to a true CBAM.65 The stated goal of the legislation is to “lower emissions across high-polluting sectors at home and abroad.”66 The bill first sets up a narrow domestic carbon tax referred to as a “carbon intensity charge.” This charge would be applied to certain “carbon-intensive” domestic industries such as fossil fuels, fertilizer, hydrogen, cement, iron, and steel that also must report GHG emissions under the EPA’s Greenhouse Gas Reporting Program (GHGRP).67 This program requires American businesses to report “greenhouse gas (GHG) data and other relevant information from large GHG emission sources, fuel and industrial gas suppliers, and CO2 injection sites in the United States.”68 The facilities of the listed sectors must also report the GHGRP data, annual electricity consumption, and yearly production of primary goods by weight to the Department of the Treasury.

The bill grants Treasury the authority to calculate and administer the carbon intensity charge. Treasury would be directed to calculate the average carbon intensity for the energy-intensive industries using the North American Industry Classification System (NAICS) codes at the six-digit level and set up baselines for 20 national industries.69 These baselines would be equal to the mean intensity of the eligible facilities within the national industry.70 The 2025 base carbon price would be set at $55 per ton for those covered facilities emitting over the baseline, but the companies would pay only a fraction of the emissions a facility emitted over the baseline.71 The proposal reduces the baseline by 2.5 percentage points each year for four years and then by 5 percentage points in each subsequent year. After 2025, the carbon price would be calculated as the amount equal to the previous year’s price plus the carbon price multiplied by the difference in inflation of the previous two years plus 5 percentage points.72

On the import side, covered carbon-intensive goods would be subject to the same charge as domestic producers, but exceptions would be granted to imports from least developed countries.73 According to a press release for the bill, imports from countries considered “opaque” would have the levy applied based on Treasury’s calculations of the “ratio of the country of origin’s economy-wide carbon intensity to the US economy-wide carbon intensity.”74 That is, if the average carbon intensity was higher than the US baseline, importers would pay a fraction of the charge based on how much it exceeded the US baseline.

Importers would also follow the same schedule as domestic industries for the changing emissions baseline. Between 2026 and 2029, the baseline would fall by 2.5 percentage points per year. Then, starting in 2029, it would decline by 5 percentage points each year. If a foreign country’s industry-specific average carbon intensity was lower than its US counterpart, the charge would not apply.

Until 2027, the charge (on both domestic and imported products) would apply only to covered primary goods.75 In 2027, the list of covered imported goods responsible for the carbon intensity charge would expand to any finished good that contained “at least 500 pounds of covered energy intensive primary goods.”76 Thus, starting in 2027, this proposed bill would essentially impose a carbon tariff on finished-goods imports. Put differently, under the Clean Competition Act of 2023, the carbon charge applied to finished-goods imports is a carbon tariff, not a CBAM, because domestic finished goods would not be subject to a corresponding domestic carbon tax. Domestic producers exporting covered primary and finished goods would be eligible for rebates. Thus, under this proposal a CBAM would be applied to primary goods and a carbon tariff would be applied to finished goods.77

The act also includes a provision on “carbon clubs.” The treasury secretary would be granted authority to determine whether a full or partial refund may be granted to a foreign country with “implemented policies which impose explicit costs on the emission of greenhouse gases which are materially similar to the charges imposed [to those set out in the proposed legislation].”

Legislation to Impose a Carbon Tariff (but Calling It Something Else)

Foreign Pollution Fee Act of 2023 (Introduced 11/02/2023)

The Foreign Pollution Fee Act, sponsored by Sens. Bill Cassidy (R‑LA) and Lindsey Graham (R‑SC), would impose a tariff on carbon-intensive imports. The bill calls the tariff a fee defined as “an ad valorem fee which is specific to a covered product” and determined by tiers of pollution intensity.78 These tiers would be based on the import’s average emissions intensity (not factory-specific intensity) as compared to the intensity of the same goods in the United States. The list of covered products includes aluminum, biofuels, cement, crude oil, glass, hydrogen (along with methanol and ammonia), iron and steel, lithium‐ion batteries, certain minerals, natural gas, petrochemicals, plastics, pulp and paper, refined petroleum products, solar cells and panels, and wind turbines. The bill would also grant the secretary of energy the authority to expand this list.

The bill would task the Department of the Treasury as the lead agency for implementing the new tax but give the energy secretary the authority to perform the calculation using the methodology laid out in the bill. Separately, section 4696 of the bill would create a carbon pricing board, formally referred to as the National Laboratory Advisory Board on Global Pollution Challenges.79 The duties of the board would include calculating the baseline pollution intensity of the covered American goods and the respective pollution intensity of the covered foreign goods. The board would comprise federal scientists, officials, and private-sector CEOs.80

As is the norm with these types of proposals, the bill would provide multiple exceptions, including under the establishment of “International Partnership Agreements,” which very much resemble climate clubs. These agreements would require countries to institute the same combination of tax and regulatory policies to be exempted from carbon tariffs on imports between the members, essentially set by American carbon accounting.81 Other exemptions would include imports of goods with less than 50 percent carbon intensity compared to the US average for free trade partners with the United States.82

FAIR Transition and Competition Act (Introduced 07/19/2021)

The Fair, Affordable, Innovative, and Resilient (FAIR) Transition and Competition Act, sponsored by Sen. Christopher Coons (D‑DE) and Rep. Scott Peters (D‑CA), sought to amend the tax code “to establish a border carbon adjustment for the importation of certain goods,” including natural gas, petroleum, coal, steel, cement, aluminum, and iron. Coons and Peters’s joint press release stated that the goal of the legislation was to protect jobs while “levying a fee on imported pollution to address carbon leakage.”83 The fee was to be based on a calculated “domestic environmental cost incurred” by US businesses equal to the cost of compliance with federal, state, regional, or local laws, and with regulations limiting GHG emissions.84 As with similar policies, the bill sought to mitigate carbon leakage with a new import tax in an effort to lower US businesses’ incentives to produce in countries with fewer environmental restrictions.

However, the proposal did not include a domestic tax on carbon emissions. Thus, although the bill called the fee a “border carbon adjustment,” it was a tariff, not a CBAM. The legislation simply calculated an estimated cost of complying with US law and tacked that price onto imports.85 Furthermore, the coverage of the proposed border carbon adjustment was limited because the bill exempted numerous countries from it. For example, any country listed as a “Least Developed Country” on the Organisation for Economic Co-operation and Development’s “Development Assistance Committee List of Official Development Assistance Recipients” was exempted. The bill also exempted any country, as determined by the treasury secretary, that enforced environmental laws and regulations “at least as ambitious as” those of the United States, provided the country did not impose a border carbon adjustment on products produced or manufactured in the United States.

Legislation for Emissions Reporting and Transparency

PROVE IT Act (Introduced 06/07/2023)

The Providing Reliable, Objective, Verifiable Emissions Intensity and Transparency (PROVE IT) Act, sponsored by Sen. Christopher Coons (D‑DE), would require the secretary of energy to “conduct a study and submit a report on the GHG emissions intensity of certain products produced in the United States and in certain foreign countries.”86 The legislation covers 22 categories of the US Harmonized Tariff Schedule (HTS) between the four- and six-digit level (the more digits, the more specific the product), including articles of aluminum, articles of iron and steel, crude oil, natural gas, fertilizer, copper, cobalt, uranium, refined petroleum products, solar panels, and wind turbines.87 This list may be expanded by the secretary of energy.

The product emissions intensity would be calculated as “the quantity of greenhouse gases emitted to the atmosphere as a result of the extraction, production, processing, manufacture, assembly, and transport, as applicable, of 1 unit of a covered product, including the greenhouse gas emissions of an upstream input that is incorporated into a downstream covered product.”88 As such, the average product emissions intensity would be the various national averages of the product emissions intensity of a category for the United States and covered countries.89

The energy secretary, secretary of state, and the US trade representative would be able to coordinate with governments of covered countries to inform and consult on emissions accounting methods and data. If the covered country was “credibly collaborating,” then the energy secretary could provide that country with “a right to consultation with respect to the determination of the average product emissions intensity … an opportunity to discuss chosen data; and … an opportunity to fill data gaps.”90

Administrative and Methodological Problems in the US Proposals

The US proposals targeting imports and carbon emissions raise measure-specific concerns but also broader concerns common to all the proposals under consideration.

Abuse of Discretion

Each US proposal grants vast discretion to a federal agency, raising serious concern that the carbon intensities and any corresponding import taxes would not be calculated in a sound and impartial manner. Most notably, the proposals carve out authority for the US government to provide proxy information if the relevant secretary deems information on the record as unreliable or insufficient. The Clean Competition Act, the Foreign Pollution Fee Act, and the FAIR Transition and Competition Act grant the Department of the Treasury broad discretion in this regard, while the MARKET CHOICE Act provides the Department of the Treasury and the EPA with similar discretion.91

Given the lack of emissions data available broadly, such authority could be central to any carbon border adjustment or carbon tariff policy. The discretion afforded to US agencies is likely to result in methodological distortions analogous to those seen in US antidumping and countervailing duty calculations that—thanks to decades of rent seeking and agency capture by domestic firms—result in duties on imports that far exceed any actual dumping or subsidization that exists. For example, if the Commerce Department deemed information provided by a foreign company during an investigation to be unreliable or insufficient, the agency would use “facts available” instead. The department could also reject timely and reliable import price data and instead use “construct” proxy prices based on less reliable surrogate cost values. In both cases, replacement data are often provided by the petitioning domestic industry itself.92 Inevitably, these and other methodologies would result in import duties that unreasonably favored the US companies that lobbied the government for relief.93 If any federal agency followed similar procedures for carbon intensity, biased results would surely emerge.

The PROVE IT Act would likely suffer from a similar abuse of discretion as well. For example, if the energy secretary deemed emissions data to be insufficient, the secretary would have the discretion to consider “the public availability of statistics on greenhouse gas emissions for particular industries from government sources and international organizations … [and] data on the quantity and source of inputs, such as electricity, consumed by particular industries.”94 In other words, the secretary would have the authority to determine what constitutes insufficient data and then fill in alleged informational gaps, including by using “the average product emissions intensity of the next highest aggregation of categories of covered products for which data are available.”95 This methodology is dangerously vulnerable to impartiality and political influence, and it could make some imports look more carbon-intensive than they really are.

Ultimately, the discretion afforded to US agencies under these legislative proposals would be likely to create another avenue to levy higher taxes on imports, turning a purported environmental tool into a vehicle for economic protectionism. Even in the MARKET CHOICE Act, which is the closest to a true CBAM proposal, there is a high risk of rent seeking and abuse of discretion to inflate foreign emissions, resulting in higher taxes applied to imports. In such a case, American import-consuming businesses and consumers would pay higher prices, and domestic industry would be isolated from competitive forces that foster efficiencies and innovations that improve the environment.

Lack of Compliance with WTO Rules

It is unlikely that any of the current border measure proposals would be consistent with the United States’ WTO obligations. As discussed above, serious WTO concerns may be avoided only by a true CBAM that applies a carbon tax equally to domestic goods and all WTO member imports and includes export rebates that do not exceed the tax amount on the same products. Only the MARKET CHOICE Act comes close to a true CBAM proposal, but it still raises WTO concerns over export rebates.96 The other measures—the Clean Competition Act (for imports of finished goods), the Foreign Pollution Fee Act, and the FAIR Transition and Competition Act—are just carbon tariffs and would thus likely violate the WTO’s nondiscrimination (most-favored-nation and national treatment) rules.

To avoid obvious WTO violations, any US proposal would need to require domestic companies to pay the price for the carbon they emit. A proposal cannot simply tax imports. Ironically, this requirement would fail the Foreign Pollution Fee Act’s stated purpose of avoiding a domestic carbon tax because establishing an explicit domestic carbon tax would be necessary for the policy to be consistent with WTO rules.

Additionally, the US proposals that set up climate clubs—the Clean Competition Act and Foreign Pollution Fee Act—might violate the most-favored-nation rule by discriminating against imports from certain WTO members outside the “club.” Lack of compliance with WTO rules is just one reason that developing a CBAM policy in the United States would be difficult and, given all the other issues already noted in this paper, it might be the least economically meaningful one.

Freer Economies Are Cleaner Economies

Instead of imposing more regulations and taxes on the American economy, policymakers could combat climate change and help protect the environment through greater economic freedom. The positive correlation between freedom and environmental performance is well established.97 As explained in the Conservative Coalition for Climate Solutions annual report, “Free Economies Are Clean Economies,” environmental stewardship is borne of well-defined and legally protected property rights. Combined with open and competitive markets, property rights provide “the foundation for the private sector to produce more goods even as people use fewer resources.”98 As a result, people are empowered to flourish and help protect the environment. This is evident in developed countries, which are producing more than ever but at the same time using fewer resources, a phenomenon known as dematerialization.99 The evidence of dematerialization provides important context for the relationship between economic growth and the environment (Figures 1 and 2), especially when comparing developed and developing countries.

![Copy: Figure 1 [print]: 20240321_LINCICOME_Beaumont-Smith_CBAM](https://infogram-thumbs-1024.s3-eu-west-1.amazonaws.com/9ae25328-1b7d-4c28-97ee-c554934696f5.jpg)

![Figure 2 [Web]: Environmental Kuznets Curve](https://infogram-thumbs-1024.s3-eu-west-1.amazonaws.com/c5aa670c-6281-4752-9642-25452eb66b02.jpg)

In economic terms, developed countries benefited from a process explained by what is known as the environmental Kuznets curve: As countries industrialize, environmental damage increases. But at a certain point, the increased income created by rapid growth leads to environmental improvements, and environmental quality begins to improve as growth continues. This results in an upside-down U‑shaped curve as the relationship between economic growth and environmental degradation turns negative. Many developed countries appear to have already reached this point (Figure 2).100

There is concern, though, about parts of the developing world where industrialization is underway, citizens’ lives are improving, and both energy consumption and carbon emissions are increasing. A CBAM or carbon tariff in the developed world could hamper these countries’ exports and development. Leaders of developing countries argue that they should be allowed to follow the same trajectory that developed countries did, and thus push back on environmental regulations and threaten to retaliate against CBAMs and carbon tariffs to protect their own domestic industries.101

Unfortunately, many of these leaders also argue against trade liberalization, believing they must protect their countries’ nascent industries, some of which are connected to multinational corporations (MNCs). In this, they are mistaken. Trade liberalization is the key to their prosperity and to a more protected environment. A major though often underappreciated benefit of trade is that it transmits knowledge and technological advancements.102 In other words, industrial processes do not need to be rediscovered from scratch. When MNCs produce in a country with less stringent environmental regulations, they typically bring the latest methods that use less energy and raw materials.103 As a result of more liberal trade policies, greener methods and products become cheaper, making them more accessible not only to local companies and consumers but also to international customers. This experience suggests that more liberalized trade and global investment mitigates carbon leakage and that climate protectionism is unnecessary and even counterproductive. In fact, individuals and businesses already take voluntary steps to reduce GHG emissions. For example, many MNCs are responding to consumer pressure to reduce emissions and have high environmental, social, and governance (ESG) standards, suggesting that working to reduce emissions is not a significant driver of carbon leakage.104

Protectionism, particularly as a tool for industrial policy whereby the government picks winners and losers, would hamper the progress developed countries can make in clean technology innovation. This would have a secondary effect on developing countries’ growth, slowing their move along the environmental Kuznets curve. Indeed, developing countries could be saved from repeating the mistakes of richer countries that used dirtier production methods and instead become leaders in adopting cleaner methods more quickly and cheaply.105

Finally, reducing emissions needs to be carried out on a global scale because the effects transcend national borders. It would be impossible for one country to carry the weight of counteracting the potential effects of the entire world’s emissions. Multilateralism provides channels for diplomatic cooperation that could create pressure to improve local environmental regulations, and as consumers demand more “clean” goods, businesses and organizations begin to demand more environmental responsibility in the supply chain.106 As this trend continues, the WTO could play an important role in providing a forum for such diplomatic cooperation, thus reducing green protectionism. To succeed in reducing excessive emissions contributing to climate change, it is vital that countries maintain the commitment to liberalizing the trading system and work together to meet global environmental challenges.

Policy Recommendations

Environmental issues are complex and affect many people, and there are major challenges to finding workable policy solutions. To develop effective solutions, policymakers must scrutinize the evidence that environmental claims are based on. They must clearly define their terms and purposes, engage in robust discussions of the cost-benefit trade-offs, and pay close attention to opportunity costs. Moreover, policymakers will have to be vigilant to refrain from empowering rent seekers.

A good first step toward mitigating climate change would be for Congress to pursue trade liberalization.107 Specifically, lawmakers should

- refrain from imposing carbon tariffs or a CBAM,

- remove antidumping and countervailing duties on imports of solar cells and modules,

- remove all US tariffs on environmental goods and key inputs in their manufacture,108 and

- engage in multilateral trade negotiations to lower trade barriers to and encourage the proliferation of environmental goods, including by finalizing the WTO Environmental Goods Agreement.

Conclusion

It is far from certain that any unilateral carbon tariff or CBAM would provide significant climate benefits. At best, these policies protect domestic industry against foreign competition and contribute to the political acceptance of carbon accounting and pricing. At worst, they are disguised economic protectionism providing avenues for rent seeking and cronyism. While economic theory supports the idea that taxing a carbon-intensive item would reduce emissions production, the likelihood of calculating the right price for emissions and appropriately administering it is minimal.109 Indeed, the level (country, industry, factory) at which a tax is applied could have the opposite effect by encouraging more carbon‐intensive production. Further, since GHG emissions are not limited to the countries that tax them or the imports from countries chosen for a tariff, the efficacy of unilateral policies would be limited at best.

Freer economies are cleaner economies. Given the centuries of evidence establishing that trade promotes prosperity and economic growth and contributes to a cleaner environment, the logical path toward a greener world is to engage in freer trade, not protectionism. Globalization is key to helping developing countries avoid the mistakes of developed countries and to advancing global efforts to reduce emissions. It is vital that policymakers resist the protectionist path that continually demonstrates the dirty business of rent seeking and does little for clean technologies innovation.

Appendix

Supporters argue that CBAMs and carbon tariffs, as part of a Pigouvian tax scheme, are necessary to correct an externality. However, even if an externality exists, that fact alone does not justify a CBAM or any tax or tariff to correct it.

The negative production externality is illustrated in a supply-and-demand graph in Figure A1, where the demand curve is equivalent to the marginal social benefit (MSB) and marginal private benefit (MPB).110 That is, the demand for the product producing emissions has a demand curve in which the social and private benefits are the same. On the supply side, the private and social costs are different and illustrated by two different supply curves in which the marginal social cost (MSC) is greater than the marginal private cost (MPC).111 Theoretically, the cost to the firm of producing an additional unit of the good is lower than the cost to society of the firm producing an additional unit. Thus, the difference between the two represents the negative externality caused by production.

![Figure A1 [Web]: Negative production externality](https://infogram-thumbs-1024.s3-eu-west-1.amazonaws.com/41669ce1-face-4849-ba90-8c1d54118586.jpg)

In this textbook model, correcting a negative production externality is illustrated in a supply-and-demand graph by achieving equilibrium between the marginal social and private costs and the marginal social and private benefits. Theoretically, correcting the externality should achieve Pareto optimality (meaning no one can be made better off without making someone else worse off) because the spillover effects of the activity are not captured by the price. As mentioned, the externality is shown as the gap between the MSC and MPC because the social cost is greater than the private cost. Thus, to close the gap or “internalize” the externality, the MPC needs to be raised to meet the MSC, equalizing the private and social costs and creating a Pareto-optimal equilibrium between the social costs and benefits. That is, the externality is considered internalized when MSB = MPB and MPC = MSC.

While the social costs are assumed to be higher than the private costs in the negative production externality model, in practice it is necessary to know the social and private costs to calculate any externality-correcting tax. One problem with calculating the social costs is that they are not incurred in a uniform manner, yet they must represent the total cost to society. Therefore, so many assumptions are needed to estimate social costs that the resulting figures have proven to be highly subjective and unreliable.

Additionally, the textbook model is incomplete because the externality cannot be represented on the consumption side. It is apparent only from production, but the emissions would not be produced without consumption of energy—in other words, supply does not exist without demand.112 However, in the case of consuming energy that produces emissions, an individual cannot be separated from the consumption’s effects on society because the individual is part of society. That lack of separation is key to why the model is incomplete because externalities can spill over only onto those not party to the transaction. But an individual, as a member of society, would still theoretically be harmed by the potentially harmful emissions caused by the consumption of energy. Thus, the textbook model puts the onus of harm on producers even though the emissions would not be produced if energy consumption was not demanded.

When the policy prescription for correcting a negative production externality is a tax, considering the consumption side of the externality—that is, demand—matters because of the incidence of the tax. Levying a tax on any good with inelastic demand is unlikely to have a large effect on consumer behavior. Energy is an inelastic good, and energy taxes like the gasoline tax have proven that demand for energy is not very sensitive to changes in prices. While energy taxes could provide a reliable revenue stream for the government, they would not have an outsized effect on the quantity of energy consumed. More important, the burden of a tax on energy would fall on the consumer because it is an inelastic good, even if it is imposed at the producer level. Though the purpose of the tax placed on energy is to mitigate emissions, it is highly unlikely that a unilateral tax would effectively reduce them, even at the local level.

Another limitation of the textbook model of an externality is that it is static, meaning that it does not consider changes over time. Therefore, any policies to correct an externality based on this textbook model say nothing about the ability of any policy to mitigate the externality in the long run. This is problematic because there is no reason to assume the externality will remain in the long run, even in the absence of explicit government intervention. Indeed, evidence demonstrates that over time with technological advancements, many production processes have become cleaner, and externalities have been mitigated without a tax. Therefore, policymakers should consider how raising taxes on a producer could stymie advancements in further improving the cleanliness of the production process.

Externalities can be mitigated without explicit government interventions. A few economists, most notably Ronald Coase and Paul Samuelson, have proposed such solutions for correcting externalities. In “The Problem of Social Cost,” Coase discusses how the inefficiencies of externalities could be resolved by private parties through bargaining.113 Coase also argues that the political bargaining and lobbying associated with correcting externalities might not maximize economic welfare, as correcting externalities is intended to do.114 Ultimately, he proposes that private bargaining and trade of relevant property rights could be used to “internalize” (correct) the externality, an idea now known as the Coase Theorem.

In its pure form, the theorem states that if transaction costs are zero, there is no information asymmetry, and there are well-defined property rights, the solution from bargaining will be efficient regardless of the initial property rights allocation.115 Coase even cites his colleague George Stigler in providing the example of the contamination of a stream:

If we assume that the harmful effect of the pollution is that it kills the fish, the question to be decided is: is the value of the fish lost greater or less than the value of the product which the contamination of the stream makes possible. It goes almost without saying that this problem has to be looked at in total and at the margin.116

Indeed, in the real world, zero transaction costs or information asymmetry is unfeasible. However, since externalities are ubiquitous and social costs do not apply uniformly, solutions informed by the idea of Coasean bargaining are often a successful market-based solution to internalizing an externality.117 For example, in Detroit, Marathon Petroleum offered to purchase part of a residential neighborhood that might be adversely affected by the expansion of its refinery to create some green space and a buffer.118 None of the homeowners were forced to sell. The program is a good example of Coasean bargaining because the property rights were well defined and the homeowners and Marathon could negotiate to price the externality as such to eliminate it.119 For those who chose to remain, the company created a green space to make “a nicer, cleaner neighborhood.”120 Thus, the bargaining internalizes the externality for both those who want to stay and those who want to leave because the spillover effects become priced into the transaction. This example also demonstrates how Coase explores the reciprocal nature of externalities, highlighting that supply does not exist without demand. Coase proposes that the spillover should be absorbed by the party it costs the least, as evinced by the Marathon Petroleum example.

Citation

Beaumont-Smith, Gabriella. “Are Carbon Border Adjustments a Dream Climate Policy or Protectionist Nightmare?,” Policy Analysis no. 978, Cato Institute, Washington, DC, July 30, 2024.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.