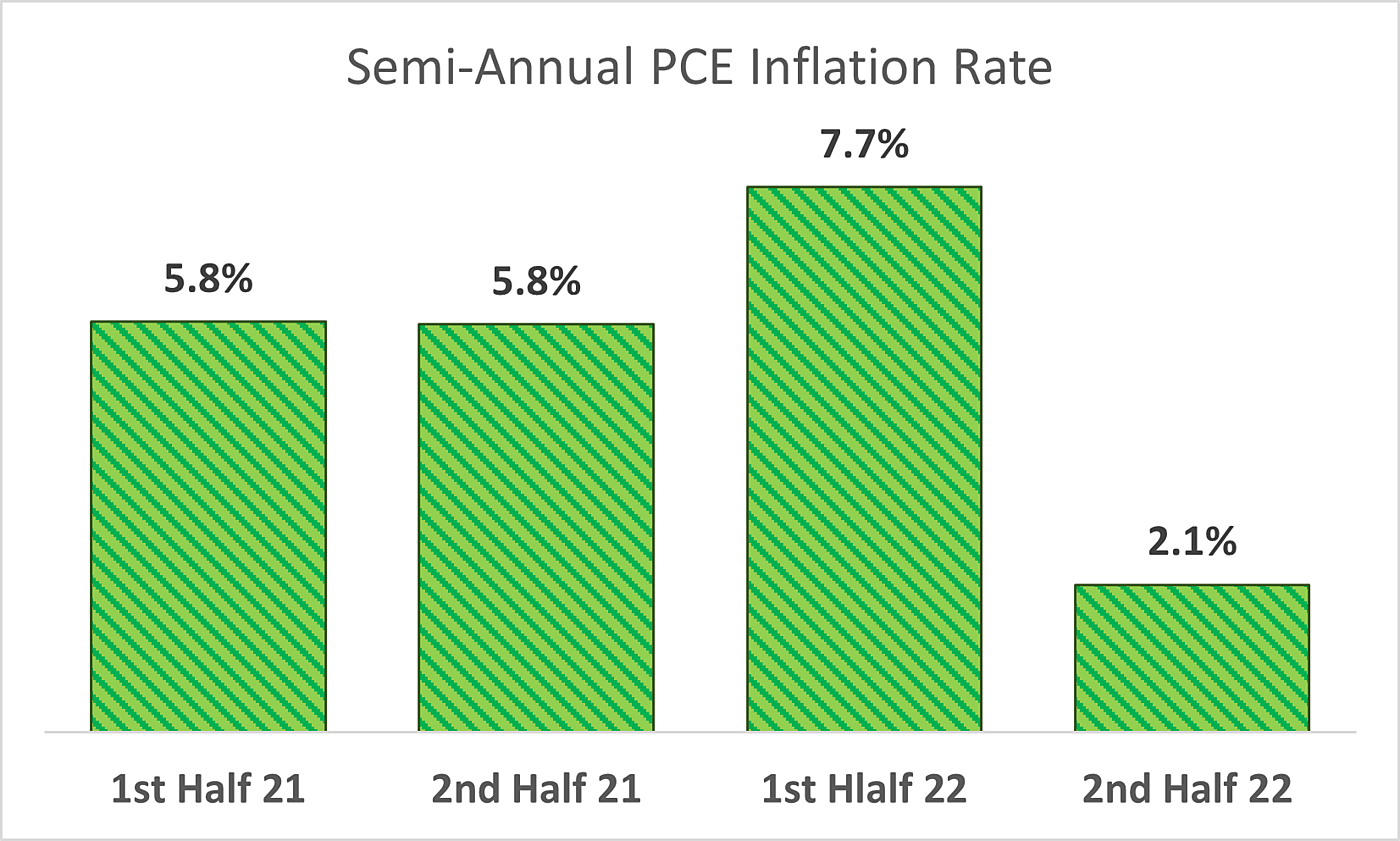

PCE Inflation Fell to 2.1% in the Second Half

Last week, the Justice Department announced criminal charges against Anatoly Legkodymov for violating anti-money laundering laws while operating Bitzlato, an off-shore crypto exchange alleged to have processed over $700 million in illicit funds over several years. Concurrently, the Treasury Department’s Financial Crimes Enforcement Network (FinCEN) ordered covered financial institutions to cease transacting with Bitzlato.

Like all financial instruments, crypto is used for crime, and this fact ought to be taken seriously. But blunt claims like Senator Elizabeth Warren’s (D‑MA) assertions that “crypto has become the preferred tool for terrorists, for ransomware gangs, for drug dealers, and for rogue states that want to launder money” do not withstand scrutiny. Lawmakers’ response to crypto’s use in crime should not be based on the faulty premises that criminals primarily choose crypto and, relatedly, that crypto is primarily used for crime.

Exaggerating the connection between crypto and crime neither helps to efficiently allocate law enforcement resources nor gives due to the great majority of crypto activity that is legitimate. Inflating risks and ignoring benefits will not lead to sound policy.

In general, claims that crypto is criminals’ preferred tool shouldn’t be taken at face value. As Senator Warren herself alluded to when introducing the Digital Asset Anti-Money Laundering Act—a sweeping financial surveillance bill cosponsored with Senator Roger Marshall (R‑KS)—approximately $14 billion worth of crypto was used in connection with illegal transactions in 2021, according to estimates in crypto analytics firm Chainalysis’s 2022 Crypto Crime Report. (As Chainalysis predicted, this estimate ultimately was revised upward to $18 billion.) This number may seem large, but it must be placed in context.

When it comes to money laundering specifically, the 2022 Chainalysis report estimates that cybercriminals laundered $8.6 billion in crypto in 2021, judging by funds flowing from illicit crypto addresses. To be clear, Chainalysis has noted that such figures are lower bound estimates and do not include crime that is not native to crypto. But even if Chainalysis’s figures were a significant undercounting (as Senator Warren has suggested), crypto’s use in illicit finance likely still would be a small fraction of the 2.7 percent of global GDP ($2.6 trillion in 2021) that a 2011 United Nations Office on Drugs and Crime report estimates is laundered annually.

For instance, a high estimate of illegal crypto activity in the peer-reviewed Review of Financial Studies extrapolated based on 2017 data that around $76 billion of illegal activity annually involves Bitcoin. At the time of the study, Bitcoin accounted for about half of total crypto market capitalization. Therefore, even if one made the aggressive (and unlikely to bear out) assumption that the other half of the crypto ecosystem experienced the same degree of illegal activity, this would still make a high-end estimate of illegal crypto activity approximately $152 billion, or 0.2 percent of contemporaneous global GDP—an order of magnitude smaller than the UN’s estimate of total money laundering around the globe each year.

The Treasury Department’s 2022 National Money Laundering Risk Assessment also supports the idea that crypto is far from money launderers’ primary tool for the job, finding that, although crypto’s use in illicit finance has been increasing over time, its use for money laundering is still “far below that of fiat currency and more traditional methods.”

When it comes to illicit transactions by sanctioned entities, crypto’s usage rose markedly in 2022, but it remains difficult to conclude that crypto is the main sanctions evasion instrument. A preview of Chainalysis’s new 2023 Crime Report indicates that a large portion of 2022’s illegal crypto transaction volume (44 percent) was associated with sanctioned parties’ activity. Nonetheless, when questioned by the House Financial Services Committee in April 2022, Treasury Secretary Janet Yellen testified that “It’s harder on a large scale for an economy to actually use crypto to evade sanctions,” as “[l]arge-scale transactions would become apparent by those who regularly examine the blockchain” and “those who use crypto need to get in and out of it.” She remarked that the Treasury Department is aware of and monitoring the risk of crypto being used to avoid sanctions, but that they “haven’t seen significant evasion through crypto so far.” Notably, Secretary Yellen’s comments came after the Treasury Department had already sanctioned Moscow-based crypto exchange Garantex, which Chainalysis found to have “accounted for the majority of sanctions-related transaction volume” in 2022.

While crypto can be a preferred tool for certain categories of crime, such as ransomware attacks, the same can’t be said generally.

For example, cryptocurrency has not materialized as the primary financial tool for terrorists. A 2019 RAND Corporation report, Terrorist Use of Cryptocurrencies, concluded that although the authors expected crypto to have a significant long-term impact on efforts to counter the financing of terrorism, current fears that cryptocurrency is “a significant enabler of terrorist groups are almost certainly overblown.” Three years on, the Treasury Department’s 2022 National Terrorist Financing Risk Assessment found that while terrorists have employed crypto, that use appears to be “limited when compared to other financial products and services.” While estimates that crypto’s role in terrorism financing likely is increasing should not to be ignored, nor should estimates that traditional financial tools like cash remain the “predominant methods of terror financing.” A recent study of ISIS terrorists’ financial activity between 2012 to 2020, for example, found that only 1 percent of their transactions used crypto to move money.

A similar pattern has been found with respect to drug trafficking. A 2022 Government Accountability Office report found that while drug traffickers’ use of virtual currencies is growing—a finding consistent with the 2022 Chainalysis report—“according to the Department of Homeland Security, traffickers continue to primarily use cash.” For context, a 2021 report by the UN’s International Narcotics Control Board cites data estimating the size of the global drug trafficking market in 2014 at between $426 billion and $652 billion. By contrast, the 2022 Chainalysis report estimated the 2014 revenue of drug-focused darknet marketplaces at less than $500 million and the 2021 revenue—the high-water mark—at less than $2 billion. In addition, while direct vendor-to-purchaser darknet sales that bypass marketplaces are growing, in 2021 they made up only about 5 percent of darknet revenue according to Chainalysis data.

It’s worth noting that financial activity that seeks to be covert by design—be it through tools like crypto or cash—poses intuitive challenges to data collection and comparison. But such uncertainties cut both ways, posing the same challenges to bold claims that crypto is the ultimate criminal tool as they do to claims that its use in crime is limited.

Furthermore, even where employed, cryptocurrencies shouldn’t be viewed as silver bullets in rogue actors’ arsenals, as demonstrated by law enforcement authorities’ ability to identify and disrupt financing schemes at times because of, not in spite of, the properties of certain crypto technologies. In fact, former Central Intelligence Agency Director Michael Morell characterized analyzing blockchains as a “highly effective crime fighting and intelligence gathering tool.”

Not only do claims that crypto is criminals’ preferred tool exaggerate the role of cryptocurrency in funding illegal activity, but they also ignore estimates both that the lion’s share of crypto activity is legitimate and that the legitimate share of crypto use is growing over time. The latest Chainalysis numbers estimate that transactions involving illicit addresses made up only 0.12 percent of the total cryptocurrency transaction volume in 2021 and 0.24 percent in 2022. (Interestingly, Chainalysis’s latest research has revised down 2021’s illicit transaction share number from 0.15 percent of total transaction volume.) Money laundering specifically was estimated to make up only 0.05 percent of total crypto transaction volume in 2021. Other assessments have gauged the share of illicit Bitcoin transactions at 0.1 percent to 5.1 percent in dollar-value terms (which the intergovernmental Financial Action Task Force has interpreted to likely be a floor). Even the high-end figures in the Review of Financial Studies article estimated that less than a quarter of the total dollar value of Bitcoin transactions through time was associated with illegal activity. And, while Chainalysis’s numbers for 2021 and 2022 indicate that illicit crypto transaction volume has been growing as an absolute number, the overall trend remains one where “crime as a share of all crypto activity is still trending downwards.”

While crypto critics are keen to point to speculation as driving crypto transaction volume, they often ignore other legitimate uses of crypto. So, what are some? In certain countries where fiat currencies and traditional banking institutions have proven untrustworthy, cryptocurrencies have filled a void. Whereas the Venezuelan bolivar has experienced significant devaluation over the last decade, with hyperinflation of 65,370 percent in 2018 alone according to the International Monetary Fund, cryptocurrency use in the country has grown in recent years. A similar phenomenon occurred in Turkey, as crypto use grew in the wake of the crashing lira. Nigeria and Kenya, which have both recently experienced depreciation in the value of their national currencies, rank 11th and 19th on Chainalysis’s Global Crypto Adoption Index. Vietnam is ranked number one in crypto adoption in no small part because of its flawed banking sector: 69% of its people are estimated to lack access to traditional banks.

Crypto also may fill a void where traditional banking systems have broken down due to war or other crises. For example, the UN Refugee Agency has launched a pilot program leveraging blockchain technology to distribute humanitarian aid to those affected by the war in Ukraine.

Beyond picking up where traditional financial systems have failed, many cryptocurrencies help to power new ways of monetizing and protecting data. For example, crypto projects such as Filecoin and Arweave are designed to incentivize the maintenance of decentralized and resilient file storage systems. Far from crypto being little more than a tool for terrorists and rogue states, this application of the technology has been leveraged by those fighting and documenting human rights abuses, including by archiving pro-democracy journalism in Hong Kong and preserving genocide survivor testimony.

And that’s to say nothing of people who may have turned to cryptocurrencies for other reasons, including censorship resistance and the ability to engage in borderless transactions.

Crypto critics don’t have to support all of crypto’s legitimate uses, or even like them, but they should at least acknowledge their existence. Fighting crime and facilitating innovation requires a clear-eyed assessment of crypto’s risks and benefits. Overstating crypto’s criminal use and overlooking other applications will not yield sound policy on either front.

As Neal McCluskey explored yesterday, education involves “developing the minds—and for many, the souls— of human beings.” This basic truth has resulted in education being a common battleground since the early days of state involvement. Not surprisingly, most of these battles have been around religion, which is a primary way morals and values are taught and upheld.

Many early public schools were at least loosely Protestant—including prayer and Bible reading as part of the school day—precisely because a strong moral upbringing was considered so essential. This resulted in court cases as early as the mid-1800s as Catholic students objected to Protestant versions of the Bible and prayers. Since the First Amendment’s protection of religious freedom was initially limited to the federal government, these cases related to religion in public schools were heard in state courts.

Some of the rulings are rather shocking by today’s standards. For example, in the 1859 Massachusetts case Commonwealth v. Cooke, Judge Maine ruled against allowing the state to prosecute a public school teacher who had struck an 11-year-old Catholic boy on his palms for 30 minutes using a long, thick rattan stick for refusing to recite Protestant prayers. The punishment only stopped when the boy agreed to repeat the Lord’s Prayer and the Ten Commandments from a King James Bible.

In his ruling, Judge Maine noted that state statues said public schools should instruct children in “the principles of piety, justice, and a sacred regard to truth, love to their country, humanity” and were to “require the daily reading of some portion of the Bible in the common English version.” He called schools “the granite foundation on which our republican form of government rests” and observed that if Roman Catholic children were permitted opt out of Bible reading, others would make the same case—and for any number of books or lessons. For Judge Maine, like many of his day, the common English version of the Bible was an unobjectionable way to teach morals and virtue. But for students and families with different (or no) religious beliefs, requiring the Protestant Bible in public schools was a violation of their freedom.

After the Fourteenth Amendment was adopted in 1868, the U.S. Supreme Court gradually “incorporated” most provisions from the Bill of Rights and made them enforceable at the state level. This allowed people who disagreed with the religious nature of public schools to take their cases to the federal level. In the 1960s, the court ruled against public prayer and reading the Bible in public schools. Since public schools are government schools, these rulings make sense considering the First Amendment’s prohibition against government establishment of religion. But what about the free exercise clause? If states are going to mandate taxpayers fund and children attend public schools, does it violate the free exercise clause if those schools must be secular?

The tension between the establishment and free exercise clauses is at the heart of many legal challenges involving education. As the School Choice Timeline shows—and as Neal discussed yesterday—Catholics were the earliest proponents of allowing taxpayer funding to follow children to nonpublic (i.e., non-government) schools. But legal challenges have accompanied school choice programs, typically focused on the establishment clause.

The first U.S. Supreme Court case on the timeline is Mueller v. Allen from 1983. This involved a Minnesota tax deduction for education expenses that was enacted in 1955. Some Minnesota taxpayers sued over the program, claiming it violated the Establishment Clause by providing financial assistance to “sectarian” institutions. The court ruled that the deduction did not violate the First Amendment since it was based on the free choice of parents and was broadly available.

The next big school choice court case came from Ohio, where lawmakers created a scholarship program in 1995 that allowed eligible students in Cleveland to receive a tuition voucher that could be used at participating public or private schools. The program was challenged by a group of Ohio taxpayers for violating separation of church and state. The Supreme Court upheld the program in Zelman v. Simmons-Harris, with Chief Justice Rehnquist writing that it “is entirely neutral with respect to religion. It provides benefits directly to a wide spectrum of individuals, defined only by financial need and residence in a particular school district. It permits such individuals to exercise genuine choice among options public and private, secular and religious. The program is therefore a program of true private choice.”

Arizona’s scholarship tax credit was the foundation for a landmark Supreme Court ruling in a 2011 case, Arizona Christian School Tuition Organization v. Winn. A group of Arizona taxpayers challenged the tax credit scholarship program since the scholarships could be used for religious schooling. The court ruled the plaintiffs had no standing to sue because tax credits involve personal income, not government money. As Justice Kennedy wrote in the majority opinion, “Respondents’ contrary position assumes that income should be treated as if it were government property even if it has not come into the tax collector’s hands. That premise finds no basis in standing jurisprudence. Private bank accounts cannot be equated with the Arizona State Treasury.”

Montana’s tax credit scholarship program resulted in another Supreme Court victory for school choice. The Montana legislature enacted a small tax-credit scholarship program in 2015. Shortly after it was enacted, the Montana Department of Revenue prohibited recipients from using their scholarships at religious schools. The department cited a provision of the state constitution prohibiting “direct or indirect” public funding of religiously affiliated educational programs. In 2020, the U.S. Supreme Court ruled in Espinoza v. Montana Department of Revenue that “A State need not subsidize private education. But once a State decides to do so, it cannot disqualify some private schools solely because they are religious.”

The most recent U.S. Supreme Court ruling around school choice involves the earliest school choice programs in the U.S.: town tuitioning programs. These programs in Vermont (launched in 1869) and Maine (1873) allow towns that don’t have public schools to pay a student’s tuition at an approved public or private school—including religious schools. Religious schools were eventually banned from both the programs due to a state court ruling in Vermont and a legislative change in Maine. In the 2022 case Carson v. Makin, the U.S. Supreme Court overturned Maine’s ban on parents choosing a religious school in the tuitioning program, ruling that it violated the parent’s First Amendment religious rights.

Despite so many legal victories for school choice, opponents continue to file lawsuits attempting to block these options. The Institute for Justice, a non-profit, public interest law firm that has successfully defended many of these programs (including Espinoza and Carson), is currently involved in cases in Ohio and New Hampshire. Just last year, IJ scored a legal victory for West Virginia families when the state supreme court ruled in favor of Hope Scholarships.

Unfortunately, Kentucky’s Education Opportunity Account Program, a tax credit education savings account, did not fare as well; the state supreme court ruled against it last month. Unlike Justice Kennedy’s opinion in the Arizona tax credit scholarship case discussed above, the Kentucky ruling treats private donations as government expenditures—a development that could impact other tax credits and deductions in the state.

Looking back through the history of school choice, one thing is clear: As long as states mandate education funding and attendance, legal battles are likely to ensue. It’s the nature of the beast. But allowing parents to direct the education of their children through school choice programs can help alleviate those fights. As Neal made clear yesterday, education is different than parks and roads—it’s inextricably linked to deeply held morals and values. That’s why school choice is essential in a society that values freedom.

In the year 2020, 94 percent of the world’s population saw a fall in its freedom compared to the year before. The annual Human Freedom Index, released today by the Cato Institute and the Fraser Institute, documents how the Covid-19 pandemic was a catastrophe for human freedom.

The report uses 83 indicators of personal, civil, and economic freedom for 165 jurisdictions for 2020, the most recent year for which sufficient internationally comparable data is available. Most jurisdictions (148) saw a decline in freedom. This year’s index presents data beginning in 2000. It shows that after a high point in 2007, global freedom experienced a slow descent through 2019, after which it deteriorated sharply. The decline set global freedom back more than two decades, erasing any gains during that period.

The pandemic accelerated worrisome long-term trends—some 79 percent of the world’s population had already experienced decreases in its freedom from 2007 through 2019. Freedom of expression, the rule of law, and freedom of association and assembly were among the categories that most saw deterioration in the past two decades.

The United States has also seen a steady decline. It now ranks 23rd in the index, having fallen 7 places since 2019. In the year 2000, it ranked 6th. The top ten freest countries in order are Switzerland, New Zealand, Estonia, Denmark, Ireland, Sweden, Iceland, Finland, Netherlands, and Luxembourg.

My co-authors—Fred McMahon, Ryan Murphy, and Guillermina Sutter Schneider—and I find that there is an unequal distribution of freedom in the world. Only 13 percent of the global population lives in the top quartile of countries in the index, while 40 percent live in the least free quartile. More than 75 percent lives in countries that are in the bottom half of the index.

We are almost certainly less free today than we were in January 2020, but only time will tell to what extent the world will regain its lost freedoms as the pandemic moderates, and our annual index will continue to monitor trends in the following years. As the world’s liberal democracies regain some of their lost freedoms, countries run by authoritarian regimes may lag further behind, thus increasing the global inequality of freedom. It is telling that the ten jurisdiction that saw the largest declines in freedom since the global high point in 2007 are all led by authoritarian regimes. In order of largest declines, those are: Syria, Nicaragua, Hungary, Egypt, Venezuela, Turkey, El Salvador, Burundi, Bahrain, and Hong Kong.

To see those and other findings, see the report here.

This week, Ticketmaster found itself under the hot lights of a U.S. Senate hearing room as a bipartisan group of senators roasted the company for allegedly engaging in anti-competitve practices.

When Ticketmaster angered musician Taylor Swift’s die-hard army of fans, known as Swifties, with a poorly managed pre-sale, those fans certainly felt harmed and they were not alone as policymakers quickly started calling the concert giant a monopoly. Is this a case of “Bad Blood” between Ticketmaster and ticketless fans or might fans find that antitrust action is “Better Than Revenge”?

In November, Ticketmaster’s website crashed after record breaking demand, leaving millions of Swift fans unable to purchase tickets to her upcoming tour despite having “exclusive” pre-sale codes. This brought renewed attention to competition in the ticket market and particularly to the impact of Ticketmaster’s merger with LiveNation. Music fans, artists, and policymakers have argued that the company’s practices, enormous market share, and alleged relationships with the largest ticket resellers allow it to add large service fees to tickets and limit fans’ access to tickets driving up costs and making it more difficult to attend events.

During the January 24 Senate Antitrust Committee hearing, Senators from both sides of the aisle accused the company, which merged with Live Nation in 2010, of engaging in anticompetitive behavior, and thus harming consumers. Several senators suggested the Ticketmaster/Live Nation merger should be undone. (Live Nation schedules shows, books venues, and in some cases, manages artists; Ticketmaster holds exclusive ticketing rights to an estimated 80% of the concert ticket market.) There are already tools at enforcers’ disposal to examine these concerns in an objective way.

The consumer welfare standard is designed in a way where courts can look at the market and Ticketmaster’s actions impact on consumers and decide whether they need to tell Ticketmaster and LiveNation they should be “Never Ever Getting Back Together.” In fact, the Justice Department is already investigating whether Live Nation, as Ticketmaster’s parent company, is engaging in monopolistic, anti-competitive practices. Some state attorneys general have also launched probes.

So, while fans and policymakers may be upset, this latest accusation of “monopoly” does not require Congress to change existing competition laws, but is instead exactly the type of scenario they were designed to analyze and respond to. Changing away from an objective standard that focuses on the consumer – not competitors or political motivations – could turn quickly turn into a “nightmare dressed as a daydream”.

While Live Nation itself has said it “takes its responsibilities under the antitrust laws seriously and does not engage in behaviors that could justify antitrust litigation, let alone orders that would require it to alter fundamental business practices,” we shouldn’t necessarily take Live Nation’s word for it. After all, this is not the first time post-merger they’ve been accused of anti-competitive behavior. In 2019, the company reached a settlement with the Department of Justice after the DOJ determined it had violated a consent decree that stipulated certain requirements after the merger with Ticketmaster in 2010. Notably, the original consent decree barred Live Nation from requiring venues to use Ticketmaster to sell tickets to shows it was promoting, but investigators looked into whether Live Nation had ignored the order. The original consent decree was supposed to lapse in 2020, but the 2019 settlement extended it to 2025.

It may be easy to presume that the 2019 settlement is evidence Live Nation needs further restrictions on its actions in the market, but it also shows the current competition law system worked as it should. Post-2019, the Justice Department has greater latitude to investigate and punish Live Nation, and it now has the authority to fine the company up to $1 million per violation. The DOJ may now recover any of the costs it incurs from having to investigate Live Nation. In other words, further violations already have significant penalties on top of any new claims the enforcers may bring following their investigation.

Bending or rewriting the antitrust laws to address only fans upset about Live Nation/Ticketmaster would ignore the existing consumer welfare standard of antitrust policy, which is specifically designed to ensure consumers benefit from a competitive market. Under the consumer welfare standard, the Federal Trade Commission and DOJ could each file a lawsuit against Live Nation right now if there is sufficient evidence of anti-competitive behavior that harms consumers.

Government interference in the market could distort the market rather than encouraging competition. Some proposed changes would leave consumers behind and instead prop up government favored numbers of competitors rather than spurring real innovation and change in markets like the ticket industry. In fact, as I have argued before, progressive politicians have spent an inordinate amount of time attacking so-called “big tech” companies for “monopolistic” practices that are anything but – yet here, they have an opportunity to go after an actual company engaged in anti-competitive practices.

Federal authorities have everything currently at their disposal to go after Ticketmaster and Live Nation if the market is not competitive. Sadly Congress cannot solve the natural monopoly that there is only one Taylor Swift, but Swifties may find that the consumer welfare standard is the “Anti(trust) Hero” they need for their concerns about Ticketmaster.

Having been thwarted at the federal level, Progressives are now turning to states to implement a wealth tax, with California taking the lead. But whether Progressives can repeat their success with state and local level $15 minimum wage laws remains to be seen.

During the 2020 Presidential primary campaign, Senators Bernie Sanders and Elizabeth Warren both proposed federal taxes on the assets of high-net-worth individuals. Sanders and Warren bowed out of the primaries in favor of now-President Biden, who did not propose a wealth tax per se, but instead offered a minimum income tax on households with net worth exceeding $100 million. The White House’s original Build Back Better framework contained a similar proposal, but no special taxes on ultra-wealthy individuals or families made it into the final legislation, renamed the Inflation Reduction Act.

With the return of divided government, any wealth tax proposal has no chance of advancing at the federal level, leaving advocates to focus on states. But a challenge with state wealth taxes is that they are easily avoided by moving across state lines.

California State Assembly Member Alex Lee (D‑San Jose), the Golden State’s main legislative advocate of wealth taxes, is aware of this concern and has both policy and rhetorical responses. On the policy side, Lee is collaborating with legislators in Connecticut, Hawaii, Nevada, New York, Maryland, Illinois, and Washington to offer parallel wealth tax measures to his AB 259. If multiple states enact the same tax, it will be harder to avoid (although as the Wall Street Journal notes there are differences between the various state proposals).

But the list of collaborators leaves out several states that have been attracting migrants from California, including Idaho, Utah, Texas, Tennessee, and Florida.

Although Nevada is on the list of supporting states, its legislative session does not begin until February 6th and so no legislation has been filed as of this writing. Further, with a Republican Governor and a non-veto-proof Democratic majority in the State Senate, it is hard to see how a wealth tax could be adopted by Nevada in 2023 or 2024.

That may be crucial because Nevada, with its lack of an income tax and proximity to the Golden State, has been drawing wealthy Californians for many years. Incline Village, a Census Designated Place on the Nevada side of Lake Tahoe has been attracting billionaires since the days of Howard Hughes and, more recently, became a vacation home for Meta’s Mark Zuckerberg.

Assembly Member Lee denies that “wealthy flight” is a serious worry, stating in his release: “despite the fear mongering, the people that are leaving California aren’t the wealthy — in fact, California ranks among the lowest for residents with incomes above $200,000 leaving their respective states.” Lee’s assertion relies on a research preview from the Center for Budget Policy Priorities (CBPP) which says: “California, a higher-tax state often cited in tax flight claims, ranks among the lowest of states in terms of residents with incomes above $200,000 leaving in an average year, from 2011 to 2020.”

The CBPP preview does not provide underlying data, so this claim is difficult to assess. IRS data for 2020 show that almost 37,000 taxpayers in the $200,000+ category left the state; more than double the number that entered. My Cato colleague Chris Edwards found that California had the third worst ratio of high income taxpayer inflows-to-outflows, just above New York and Illinois.

Further, CBPP’s analysis does not include 2021 and 2022, years in which many professionals and entrepreneurs reached the conclusion that physical location no longer matters so much.

The reality is that data on $200,000+ income earners tell us little about how individuals will react to a wealth tax. The vast majority of individuals in the $200,000+ income bracket cited by Lee and CBPP have not accumulated the $50 million of wealth needed to trigger California’s wealth tax, so statistics at that level of imprecision are minimally useful.

We do know that Forbes found that the number of California billionaires fell from 189 in 2021 to 186 in 2022 due to relocations. In prior years, Elon Musk and Larry Ellison, among the world’s ten richest individuals, both left the state. Absent any history of state wealth taxes, we do not know how many more would leave if Lee’s tax measure passes.

But, if the wealth tax drives out even a few of the top billionaires, the revenue implications could be catastrophic. Although many of the ultra-rich shield their income from taxation, many more pay California’s maximum 13.3 percent income tax. If a large cohort of these individuals leave, the state will not only miss the opportunity to collect the wealth tax but could also lose billions of income tax revenue.

With the state swinging from large surpluses to substantial deficits, now is not a great time to take fiscal gambles. Instead of seeking innovative ways to collect more tax revenue, California legislators (and their counterparts in other high tax states) should be looking for opportunities to eliminate wasteful spending. Other states have demonstrated the ability to provide a sufficiently high level of public services to attract Californians (and New Yorkers and Illinoisans) while taxing away a much lower proportion of state personal income. They should serve as a model for California policymakers.

“If I’m not happy with my public park, should I get a voucher for a country club?”

“If I don’t like the highways, should I get money for private roads?”

“What if I don’t like the fire department? Should I get taxpayer dollars for my own fire service?”

If you’ve been involved in the school choice debate for very long, you’ve almost certainly seen these objections to choice. Basically, we would never “voucherize” these things – that would be crazy! – so why should we let people use public funding for private education?

The obvious answer, as I’ve explained before, is that education is about far more – for some people, infinitely more – than where you take a walk and have a picnic, or lay asphalt. It is about nothing less than shaping human beings, which inescapably involves deeply held, diverse convictions about the goals and meaning of life, and the very nature of the world and universe. It encompasses beliefs that no government should be in a position to decide can – or cannot – be taught with the education tax dollars that all people must pay.

That education deals with nothing less than the formation of human beings is why religion has been so central to the choice movement and debate, as one can see in our new School Choice Timeline. Arguably nothing is more intertwined with the meaning of life, and how one should live, than religion, and it is a major reason that public schooling cannot be squared with a free and equal society.

The huge difficulty of aligning religion and government schooling has been encountered from the earliest days of state education. The Prussians – infamous for their use of public education to bind people to the state – had to make accommodations for families to get either Protestant or Catholic instruction. Benjamin Rush, one of the earliest advocates of education to attach people to the new United States, wrote that children should receive education from the denominations to which their parents belonged. Horace Mann – the “father of the common school” – devoted a major chunk of his last annual report as Massachusetts education secretary to assuring people that he had no desire to remove the Bible – which he called “the acknowledged expositor of Christianity” – from schools, as he fended off objections that common schooling would trample crucial but controversial Christian tenets.

Of course, the content of the Bible itself, and who should interpret it, is in dispute. Among Christians, the Protestant version on the Bible typically has fewer books than the Catholic, and while Protestants tend to not see a central, earthly authority for interpreting scripture, Catholics believe the Roman Catholic Church has the God-given authority to do so.

This split is a major reason that the School Choice Timeline has numerous entries about Roman Catholics pursuing choice, or at least pleading for funding for their schools rather than just de facto Protestant public schools. Even lowest-common-denominator Christianity often could not bring the two together, which is why at their peak in 1965, Catholic schools – private schools funded by tuition and Catholic communities – enrolled about 12 percent of all school-aged children. That is a lot of families first paying taxes for public schools, then tuition for schools consistent with their religious convictions.

What about people with no religion? They, too, were long treated unequally by the pan-Protestant public schools, which sometimes began the day with the Lord’s prayer and had other religious expression interwoven. Many fought the imposition of religion, ultimately with lawsuits culminating in the Supreme Court’s 1963 Abington School District v. Schempp decision prohibiting public school prayer and Bible reading. But that rendered the public schools inhospitable to anyone who believed that religion was important to education, or central to life.

As Roman Catholics became more secular, moved to the suburbs, and saw declines in the ranks of priests and nuns, their schools entered a long decline. They still educate more than 1.6 million children, but Protestant private schools, particularly nondenominational, have been ascendant. More conservative Protestant families, as well as increasing numbers of Catholics, have also flocked to homeschooling. And all typically pay once for public schools, a second time for education consistent with their deeply held religious beliefs. And Christians are not alone – increasingly, Jews have turned to private schooling to instill in their children a rich understanding of their religion and culture, and Islamic schools are growing.

Because religion is, and has been, of such deep importance to many people, it should be no surprise that most private schools are religious. Nonetheless, when school choice bills are debated, many choice opponents suggest that this a problem for choice. But it is not a choice problem. It is a condemnation of public schooling – concrete evidence that such a system cannot treat people with diverse convictions equally.

As I mentioned on Monday, this has been recognized by no less a choice opponent than retired U.S. Supreme Court Justice Stephen Breyer, who has twice observed in dissents against pro-choice rulings that if government cannot exclude schools from choice programs for being religious – if doing so is discrimination against religion – then public schooling itself is guilty because it funds only secular education.

Religion makes choice essential because, constitutionally, government must neither discriminate in favor of religion nor against it.

But eking out basic equality under the law is a minimal reason to embrace choice. Far more important is fully embracing freedom and pluralism.

Universal choice would enable people to much more easily pursue education imbued with deep commitments and rich meaning, and to create from the bottom up a society filled with strong, diverse communities. That would not only make the country a more pluralist, dynamic – and frankly, interesting – place, it could give individuals greater opportunities to find communities that give them a powerful sense of belonging and fulfillment. It could also help people discover new ways of seeing the world, and discern what matters most in life.

Education is not a mere park or road. It is about nothing less than developing the minds – and for many, the souls – of human beings. As history makes clear, that is why religion is so central to school choice, and why a truly free and equal society must not have government decide what is, or is not, taught with education money that all are forced to pay.