Cato at Liberty

Cato at Liberty

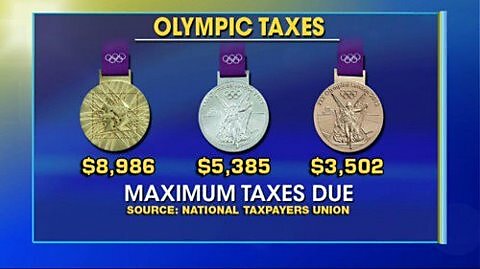

The folks at Americans for Tax Reform have received a bunch of attention for a new report entitled “Win Olympic Gold, Pay the IRS.”

In this clever document, they reveal that athletes could face a tax bill — to those wonderful folks at the IRS — of nearly $9,000 thanks to America’s unfriendly worldwide tax system.

The topic is even getting attention overseas. Here’s an excerpt from a BBC report.

US medal-winning athletes at the Olympics have to pay tax on their prize money — something which is proving controversial in the US. But why are athletes from the US taxed when others are not? The US is right up there in the medals table, and has produced some of the finest displays in the Olympics so far. … But not everyone is happy to hear that their Olympic medal-winning athletes are being taxed on their medal prize money. Athletes are effectively being punished for their success, argues Florida Senator Marco Rubio, a Republican, who introduced a bill earlier this week that would eliminate tax on Olympic medals and prize money. …This, he said, is an example of the “madness” of the US tax system, which he called a “complicated and burdensome mess”.

It’s important to understand, though, that this isn’t a feel-good effort to create a special tax break. Instead, Senator Rubio is seeking to take a small step in the direction of better tax policy.

More specifically, he wants to move away from the current system of “worldwide” taxation and instead shift to “territorial” taxation, which is simply the common-sense notion of sovereignty applied to taxation. If income is earned inside a nation’s borders, that nation gets to decided how and when it is taxed.

In other words, if U.S. athletes earn income competing in the United Kingdom, it’s a matter for inland revenue, not the IRS.

Incidentally, both the flat tax and national sales tax are based on territorial taxation, and most other countries actually are ahead of the United States and use this approach. The BBC report has further details.

The Olympic example highlights what they regard as the underlying problem of the US’ so-called “worldwide” tax model. Under this system, earnings made by a US citizen abroad are liable for both local tax and US tax. Most countries in the world have a “territorial” system of tax and apply that tax just once — in the country where it is earned. With the Olympics taking place in London, the UK would, in theory, be entitled to claim tax on prize money paid to visiting athletes. But, as is standard practice for many international sporting events, it put in place a number of tax exemptions for competitors in the Olympics — including on any prize money. That means that only athletes from countries with a worldwide tax system on individual income are liable for tax on their medals. And there are only a handful of them in the world, says Daniel Mitchell, an expert on tax reform at the Cato Institute, a libertarian think tank — citing the Philippines and Eritrea as other examples. But with tax codes so notoriously complicated, unravelling which countries would apply this in the context of Olympic prize money is a tricky task, he says. Mitchell is a critic of the worldwide system, saying it effectively amounts to “double taxation” and leaves the US both at a competitive disadvantage, and as a bullyboy, on the world stage. “We are the 800lb (360kg) gorilla in the world economy, and we can bully other nations into helping enforce our bad tax law.”

To close out this discussion, statists prefer worldwide taxation because it undermines tax competition. This is because, under worldwide taxation, individuals and companies have no ability to escape high taxes by shifting activity to jurisdictions with better tax policy.

Indeed, this is why politicians from high-tax nations are so fixated on trying to shut down so-called tax havens. It’s difficult to enforce bad tax policy, after all, if some nations have strong human rights policies on privacy.

For all intents and purposes, a worldwide tax regime means the government gets a permanent and global claim on your income. And without having to worry about tax competition, that “claim” will get more onerous over time.

P.S. Just because a nation has a right to tax foreigners who earn income inside its borders, that doesn’t mean it’s a good idea to go overboard. The United Kingdom shows what happens if politicians get too greedy and Spain shows what happens if marginal tax rates are reasonable.

P.P.S. The International Olympic Committee apparently insisted that London couldn’t host the games unless the UK government agreed not to tax any of the athletes on their winnings.

Related Tags

Cato scholars aspire to high standards for accuracy and analysis. Because of that, I feel obligated to note an error in Dan Mitchell’s recent post on the ongoing failure of Washington’s economic stimulus efforts.

Dan writes:

The politicians in Washington flushed about $800 billion down the toilet and we got nothing in exchange except for anemic growth and lots of people out of work.

About $800 billion? I wish. By my calculation, federal fiscal stimulus efforts for the recent recession are now close to $2.5 trillion—at least.

Of course, Dan had in mind the $820 billion American Recovery and Reinvestment Act that President Obama pushed through Congress within a month of becoming president. But ARRA was just one of several fiscal stimulus bills that Washington adopted, beginning with the February 2008 Economic Stimulus Act and continuing through to early this year. Some of those bills were explicit stimulus measures; others were ostensibly intended to address other policy goals, but were engineered to provide fiscal stimulus by borrowing and spending money now, and then using future government revenues to pay off that borrowing (perhaps when God grants St. Augustine chastity and continence).

Below is a list I’ve kept of these stimulus measures. I use multiple-sequence numbering to differentiate between major and minor legislation.

| # | Name | Stimulus (Billions) | Became Law | Public Law | Note |

| 1.0 | Economic Stimulus Act of 2008 | $167 | 2/13/2008 | 110–185 | A “timely,” “targeted,” and “temporary” fiscal stimulus. |

| 1.0.1 | Unemployment Compensation Extension Act of 2008 | $5.7 | 11/21/2008 | 110–449 | Extends unemployment insurance, using borrowed funds so as to provide stimulus. |

| 2.0 | American Recovery and Reinvestment Act of 2009 | $819 | 2/17/2009 | 111–16 | This package of public works projects, tax breaks, unemployment insurance extension, and other spending would keep unemployment below 8%. |

| 2.0.1 | Cash for Clunkers Extension | $2 | 8/7/2009 | 111–47 | Continues the subsidy for new car purchases that was first enacted as part of ARRA. |

| 2.1 | Worker, Homeownership and Business Assistance Act of 2009 | $44.7 | 11/6/2009 | 111–92 | Extends and expands the homebuyer tax credit program. |

| 2.2 | Temporary Extension Act of 2010 | $8.1 | 3/2/2010 | 111–144 | Extends unemployment insurance, using borrowed funds so as to provide stimulus. |

| 2.3 | Hiring Incentives to Restore Employment Act | $17.6 | 3/18/2010 | 111–147 | AKA the “Jobs for Main Street Act,” this “jobs bill” would “spur job growth and strengthen the private sector.” |

| 2.4 | Continuing Extension Act of 2010 | $18.1 | 4/15/2010 | 111–157 | Extends unemployment insurance, using borrowed funds so as to provide stimulus. |

| 2.5 | Homebuyer Assistance and Improvement Act of 2010 | $145 | 7/2/2010 | 111–198 | Extends the deadline for submitting paperwork for homebuyer credit. |

| 2.6 | Unemployment Compensation Extension Act of 2010 | $33.9 | 7/22/2010 | 111–205 | Extends unemployment insurance, using borrowed funds so as to provide stimulus. |

| 2.6.1 | United States Manufacturing Enhancement Act of 2010 | $3 | 8/11/2010 | 111–227 | Reduces or suspends various import duties. |

| 2.7 | Small Business Jobs Act of 2010 | $85.4 | 9/27/2010 | 111–240 | Expands SBA loan programs and provides other small business assistance. |

| 3.0 | Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 | $916.8 | 12/17/2010 | 111–312 | A package of tax breaks, including a cut in the Social Security payroll tax, an extension of the Bush income tax rates, and an extension of unemployment insurance. |

| 3.1 | Temporary Payroll Tax Cut Continuation Act of 2011 | N/A | 12/23/2011 | 112–78 | Extends the Social Security payroll tax cut, extends unemployment insurance, and other provisions. |

| 4.0 | Middle Class Tax Relief and Job Creation Act of 2012 | $167.6 | 2/22/2012 | 112–96 | Extends the Social Security payroll tax cut, among other provisions. |

| SUM: | $2,433.9 | ||||

Keep this list in mind when someone says there was “only” $800 billion in stimulus—or when someone says the only reason the stimulus failed is because it was too small.

Post Script(2016): As part of its final Economic Report of the President report, the outgoing Obama Council of Economic Advisers offered a lengthy (and positive) assessment of its handling of the recession, including efforts to fiscally stimulate the economy. The report (p. 34) notes that “Together with automatic stabilizers, the total fiscal stimulus over these four years averaged 4 percent of GDP,” or about $2.5 trillion.

Related Tags

Earlier this week I wrote about the perils of the NRA’s single-issue politics. Now it’s breastfeeding moms in the crosshairs – different issue, same principle.

In the NRA case, it seems that they’re going after a Tennessee state legislator – a long-time NRA member and supporter, no less – who opposed a bill that would have allowed employees to keep guns in their cars while parked in their private employers’ parking lots. The principle at issue there could not be simpler or more basic to a free society: individuals, including private employers, should have a right to determine the conditions on which others may enter their property. The NRA’s mistake is in asking the state to restrict that right in the name of the Second Amendment, which of course applies only against governmental, not private, restrictions.

The breastfeeding moms make a similar mistake. We learn from NPR this morning that a number of them have just gathered en masse and staged a “Great Nurse-In” at the U.S. Capitol. Their aim is to secure “federal protection of breastfeeding everywhere.” Everywhere? In my home, my business?

Don’t get me wrong: I’m no more against the right to breastfeed than I am against the right to keep and bear arms. That’s not the point. Rather, the point is that, in a free society, the property right is fundamental, starting with your property in your person and your liberty, which you can exercise only to the extent that you respect the equal rights of others. Property rights set the lines that determine where one person’s rights end and the next person’s begin, which is why getting those lines right is so crucial to a society that aspires to protecting equal rights.

The breastfeeding moms might well object if they were forced to allow people to carry guns into their businesses, just as the gun owners might object to being forced to allow breastfeeding in theirs. And it isn’t that some values are better than others. We can argue over that all day and get nowhere. With rights, by contrast, there’s a good possibility of agreement. In fact, the nation is based on a live-and-let-live principle we largely agreed on at the outset – and lived by, for the most part, until we started asking government to impose our values on others, leading to the war of all against all that we see all about us today and to the politicization of everything, including parking lots and breastfeeding.

In June, 2010 the Cobden Centre in London released a report on “Public Attitudes on Banking,” based on a questionnaire to which 2000 Britons responded. The findings of that report have since been offered, both by the Cobden Centre itself and by others, as proof that many people today believe that banks store rather than lend money surrendered to them in exchange for deposits payable on demand.

This week, for instance, a blogger named James Miller (whose article appears as well at Mises.ca and ZeroHedge, among other sites) wrote:

[U]sually depositors don’t fully realize that their funds are not really there in whole. In a 2010 study commissioned by The Cobden Center, it was found that 74% of U.K. residents polled believed they were the legal owners of their banking deposits. And while 61% answered that they wouldn’t mind if their money was used for additional lending, 67% responded that they wanted convenient access to what they saw as their money. Whether or not one regards fractional reserve banking as a clear case of fraud, it seems that a good portion of the public is wrongly informed on the mechanics of modern day banking.

But as even a careful reading of Miller’s own summary of it should make clear, whatever else the Cobden survey may demonstrate, it most certainly does not demonstrate that most depositors think that the money they hand over to banks sits in the banks’ vaults (or perhaps in those of a central bank) until some or all of it is either withdrawn or transferred to specific others by order of the original depositors.

Unless the questions they pose are chosen very carefully, survey results can easily mislead, and are indeed sometimes designed precisely with that end in mind. That isn’t to say that the Cobden survey was intended to mislead–I am in fact inclined to believe that it wasn’t. But it misleads nonetheless, thanks to the utter ambiguity of several of the questions it poses.

Consider the first survey question: “Why do you keep some of your money in a current account?” 15% of respondents answered “For safekeeping” and 67% answered “For convenient access,” while only 10% answered “Because it earns interest.” The predominance of the first two replies over the third might appear to suggest that most people suppose that their money is being stored. But the responses may be just as readily interpreted to mean that they consider fractionally-backed deposits to be both more convenient and safer than cash kept on one’s person, at home, or in a cash register. Indeed, in these days of deposit insurance, it is hard to see why anyone concerned with safety, even exclusive of other considerations, would hesitate to prefer a fully-insured demand deposit balance to cash, while being perfectly indifferent to the dangers stemming from the lending of “their” deposits.

In reply to the survey’s second question, “Who do you think owns the money in your current account(s)?”, 74% answered “The account holder,” while only 8% said “The bank.” Another 20% answered, “Both the bank and the account holder.” Proof that many British bank depositors don’t know what their banks are about? Hardly. The responses instead prove nothing more than that the question posed can be interpreted in two different ways, depending on the meaning given to the word “money.” Cobden Centre types, steeped in Austrian monetary economics, may insist that “money” ought to mean what others call “base” or “high-powered” money; but the fact remains that for most people, including most economists, a fractionally-backed bank deposit or note is itself “money.” The latter, more common usage is implicit in standard working measures of national money stocks such as M1, M2, and so forth.

So, who owns the “money” in someone’s current account? Well, it is in fact owned by the account holder, or by the bankers, or by both depending on how money is defined. If “money” is taken to mean “base money,” than when someone accepts a demand-deposit credit from a banker in exchange for “money,” that person surrenders ownership of the “money” to the banker, while becoming the owner of a deposit credit–a claim against the bank–of the same nominal value as the surrendered sum. But now suppose that by “money” we mean money in the broader sense, including demandable bankers’ IOUs. By this definition, of course, the depositor continues to “own” the deposited sum, because instead of merely surrendering ownership to “money” he must now be understood to have merely exchanged one kind of money for another. The banker now owns the surrendered base money, while the depositor owns broad money consisting of a redeemable deposit balance. It thus follows that all of the respondents to the survey question, including the 2% who said “I don’t know,” may have been perfectly well informed of what their banks were up to, differing only in their interpretation of the question, or in the extent to which they were (understandably) baffled by it.

The survey’s third question is equally ill-posed. It asks respondents to say what percentage of their current accounts is (1) held as reserves; (2) lent; (3) used to speculate on financial derivatives. That 66% answered “I don’t know” is surprising only because one would expect the percentage replying so to such a question, calling as it does for a specific magnitude of which even many expert economists must have been unaware, while posing as alternatives two possibilities that are not in fact mutually exclusive (money might be simultaneously “lent” and “used to speculate on financial derivatives”), to have been closer to 100! The response proves, in any event, that at least two-thirds of those surveyed were not convinced that their “deposits” were fully backed by reserves.

Oddly, we are not given (as we are with regard to the other questions) a breakdown of the other responses to question 3, and so cannot say more than this. But it is at least possible that none of the 2000 respondents actually believed that his or her current account was backed 100% by reserves. If anything, the fact that we are not told what percentage of those surveyed answered this key question in accordance with the presuppositions of the anti-FR crowd ought to lead one to suspect that the percentage was in fact very low. Survey question 4, however, asks respondents to indicate “how they feel” about their banks making loans using current account deposits, and finds that 33% think the practice wrong because “they have not given [their bankers] permission to do so.” Thus support appears to be given to the upper-bound ignorance quotient of 2/3.

But here once again the question is ill-conceived, not to be sure because it is ambiguous, but because it is what survey designers call a “suggestive” question, and as such one that nudges respondents in a particular direction. The question, in full as it appears in the report, reads as follows:

You may or may not have been previously aware that banks lend out some of the money deposited within current accounts by their customers to fund loans [sic]. Which of the following best describes how do [sic] you feel about the fact that your bank lends out some of the money in your account as loans [sic]?

The subtle, implicit suggestion here, perhaps unintended, is that banks are not systematically informing their customers about what they do (so that customers “may or may not” be aware of it), and that their conduct is such as might be expected to arouse some definite “feelings” among those customers.

If you doubt that the manner in which the question is posed favors the most-frequently offered response–that is, if you doubt that the question is such as tends to favor expressions of dismay regarding what bankers’ regard as business as usual–imagine getting the following message in your voicemail, where the words indicated by **** are inaudible: “Hello. You may not be aware of it, but **** has been **** your ****. How do you feel about that?” Forced to say either “fine” or otherwise, I venture to guess that you’d admit that such a message leaves you “feeling” like someone who has been decidedly, albeit mysteriously, snookered.

Addendum (August 4 at 5:05PM): I had not bothered to comment on the Cobden survey’s fifth and final question, because I found it so loopy that I hardly knew where to begin. I ought to have observed, nonetheless, that 26% of those surveyed responded to it by choosing, of several alternatives, the one that said “We should ensure that banks keep reserves equal to 100% of deposits.” Would the respondents have made the same choice had the response in question been lengthened by adding the words “while allowing them to collect from us annual fees of somewhere between 5% and 10% of our average balances”? Unless Cobden redoes the survey, I suppose we’ll never know.

Related Tags

Overall, this Tennessean article summarizes well yesterday’s House Oversight Committee hearing on the IRS rule that Jonathan Adler and I write about here and here. Unfortunately, the article does perpetuate the misleading idea that the nation’s new health care law is “missing” language to authorize tax credits in federally created Exchanges. (The statute isn’t missing anything. It language reads exactly as its authors wanted it to read.)

Excerpts:

Rep. Scott DesJarlais’ argument that the health-care reform law lacks wording needed to implement a crucial part of it took a major step forward Thursday.

The Jasper Republican got a hearing before the House Committee on Oversight and Government Reform on his claim that the Internal Revenue Service lacks authority to tax employers who fail to offer health policies and leave workers to buy coverage through federally established exchanges.

His arguments, while not uncontested during the hearing, apparently won over the committee chairman, Rep. Darrell Issa, R‑Calif. Issa signed on Thursday as a co-sponsor of DesJarlais’ bill related to the issue. Other House Republican leaders also have shown interest, DesJarlais said in an interview afterward. He said he expects a vote on the House floor sometime this fall.

And a Senate version has been introduced by Sen. Ron Johnson, R‑Wis…

DesJarlais contends that Congress worded the law in a way that authorizes the taxes and tax credits only for insurance bought through state-based exchanges, not federal ones…

The distinction is important because many states are balking at setting up their own exchanges. DesJarlais’ argument would mean federal exchanges couldn’t be implemented in those states, either…

“They have rewritten a law Congress haphazardly drafted,” DesJarlais said.

His bill, which has 35 cosponsors, would keep the IRS from moving forward with its regulatory language.

“I have employers watching this very closely,” DesJarlais added. Essentially, he said, the issue is “about whether ObamaCare can continue to exist.”

Related Tags

Can we finally all agree that Keynesian economics is a flop? The politicians in Washington flushed about $800 billion down the toilet and we got nothing in exchange except for anemic growth and lots of people out of work.

Indeed, we’re getting to the point where the monthly employment reports from the Labor Department must be akin to Chinese water torture for the Obama administration. Even when the unemployment rate falls, it gives critics an opportunity to recycle the chart below showing how bad the economy is doing compared to what the White House said would happen if the so-called stimulus was enacted.

But for the past few months, the joblessness rate has been rising, making the chart look even worse.

I never watch TV, so I’m not in a position to know for sure, but I haven’t seen any articles indicating that the Romney campaign is using this data in commercials to criticize Obama. That seems like a missed opportunity. But since it’s not clear to me that Romney would actually do anything different than Obama (check out this post if that seems like an odd assertion), I don’t focus on the political implications.

Instead, I’m hoping the American people will learn an important long-run lesson: If you want more growth and prosperity, the recipe is smaller government and free markets. In other words, our economic policy should be more like Hong Kong and Singapore, but the Obama administration has been making us more like France.