The violence in Ferguson is inexcusable. But it should not be seen as primarily a reaction to the grand jury’s decision not to indict Darren Wilson. Rather, it should be seen as a reaction to years of racially charged policing and a discriminatory justice. Focusing on Officer Wilson’s culpability detracts from the bigger, nation-wide story: That every month there are innumerable police abuses throughout the country that go unnoticed and unreported, and, even if they are reported, the accused officers will likely never be disciplined, much less charged with a crime. Unfortunately, many of these abuses are disproportionately felt by people of color. Abuses can be small and nearly impossible to discover, such as stopping a car full of black men without probable cause, or they can be large and public, such as unjustifiably gunning down an unarmed black teenager. Sometimes the police action may be justified, and sometimes it may not, but the systems in place for determining culpability are egregiously biased in favor of police officers. Add to this an over-militarized police force that uses surplus military gear to violently break into homes 100 times per day, usually to only execute search warrants, and you have a recipe for disaster and an urgent need for reform. We should take advantage of this time of heightened awareness to reform a justice system that has too much power and too little accountability. Hopefully the violence in the street will not overshadow the legitimate protests, but I fear it may.

Cato at Liberty

Cato at Liberty

The World Trade Organization (WTO) seems on the verge of approving an agreement with India to allow the Trade Facilitation Agreement (TFA) to move forward. The TFA is to be applauded. It will make a useful contribution toward helping goods move across borders more efficiently, which will tend to increase trade and promote economic growth.

The problem is not with the TFA, but rather with the high price that the global community seems ready to pay for it. India has asked that it be allowed to exceed the level of domestic agricultural subsidies to which it agreed twenty years ago in the Uruguay Round negotiations. For the first time in history, those talks led to limits on the ability of countries to use trade distorting agricultural supports. Those subsidies had been rampant, often leading to surplus production that depressed crop prices in global markets. Farmers who were being subsidized generally were happy enough with that arrangement, but it was a very different story for unprotected farmers in other countries. Many of the world’s farmers are quite poor to start with. Government-driven decreases in commodity prices make them even poorer.

A teachable moment is slipping away because no WTO member has been willing to stand up and explain what’s going on. India sanctimoniously declares that it needs to promote food security through use of a robust public stockholding program, and would like the world to believe that existing WTO rules prohibit them from doing so. This is simply not correct. The Uruguay Round includes specific provisions detailing how public stockholding may be used for food security purposes. A great deal of time, effort and tough negotiating went into developing those provisions. There is no limit on government expenditures to provide food – including free or reduced-price food – to low-income people. However, there is a clear requirement that purchases of commodities for public stocks must be made at open-market prices. It is not allowable to purchase commodities at above-market prices in order to provide a subsidy to farmers.

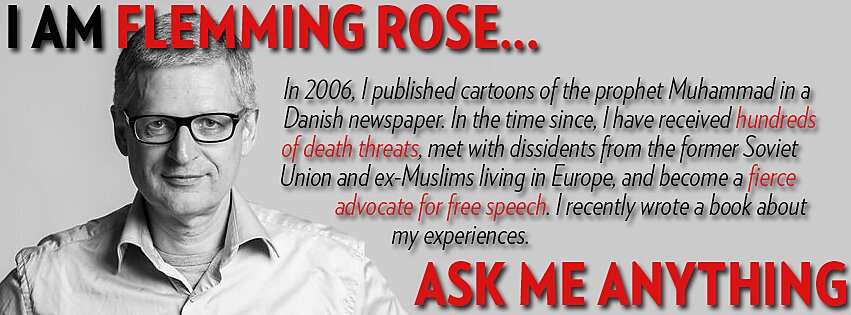

In their effort to provide the public with information about controversial yet important world events, journalists face constant intimidation. Whether it takes an extreme form—such as beheading or death threats—or a less violent one—like government censorship or enforced political correctness—it nonetheless constricts their ability to convey truthful information about key issues.

No one knows this better than Flemming Rose.

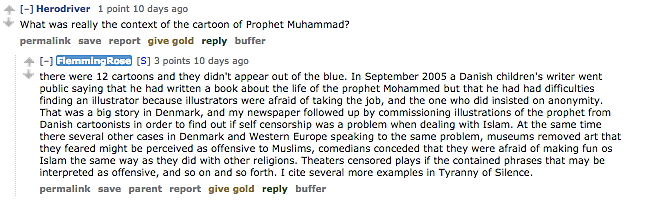

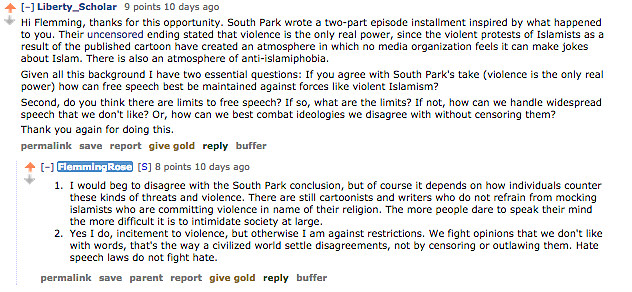

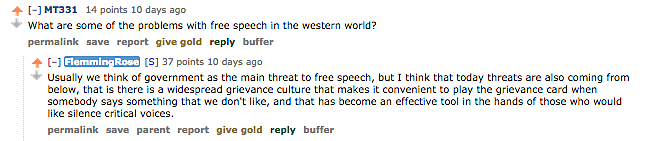

In 2006, the Danish newspaper Jyllands-Posten published 12 cartoons of the prophet Muhammad, stoking the fires of a worldwide debate about what limits—if any—should constrain freedom of speech in the 21st century.

Rose, then the paper’s culture editor, defended the decision to print the drawings, quickly becoming the target of death threats and more, all of which he recounts in his new book, published by the Cato Institute.

In The Tyranny of Silence: How One Cartoon Ignited a Global Debate on the Future of Free Speech, Rose provides a personal account of an event that has shaped the global debate about what it means to be a citizen in a democracy and how to coexist in a world that is increasingly multicultural, multireligious, and multiethnic. Rose writes about the people and experiences that have influenced his understanding of the crisis—including meetings with dissidents from the former Soviet Union and ex-Muslims living in Europe—and takes a hard look at the slippery slope of attempts to limit free speech.

Rose’s message clearly resonates with lovers of liberty around the world. A special one-on-one conversation between Rose and Jonathan Rauch of the Brookings Institution, hosted at the Cato Institute in mid-November, saw over 100 in-person attendees with another 53 people tuning in online.

That impressive showing, however, was far outpaced by the mass response to Cato’s very first Reddit AMA, featuring Rose, which has been viewed well over 200,000 times since it was first published on November 13th, and continues to draw thousands of Reddit viewers every hour, almost two weeks later.

Rose’s AMA, entitled “I am a journalist and free speech advocate who has received hundreds of death threats since 2006. AMA,” quickly broke into the top ten discussions on the iAMA forum that week. As questions continues pouring in, Rose sat down for a second full hour session the day after the original session was scheduled.

You should definitely read the AMA yourself, but here are some highlights:

Enjoyed the discussion? You can read the whole thing here. And, of course, don’t forget to buy the book to read all of Rose’s harrowing tale.

Title VIII of the Civil Rights Act, also known as the Fair Housing Act (FHA), makes it illegal to deny someone housing on the basis of race and other protected characteristics. Applicable to governments, private entities, and individuals, the FHA prohibits racially discriminatory practices in most if not all transactions relating to housing.

For example, a landlord can’t refuse to rent an apartment to an otherwise qualified tenant, solely on the basis of race. Similarly, banks and credit unions can’t take a borrower’s race into account when deciding whether and on what terms to extend credit for the purpose of buying a home.

While it’s clear that the FHA bars such discriminatory intent, it remains an open question whether it covers claims of “disparate impact,” where a neutral policy disproportionately harms members of the protected class. Under this theory, a landlord insisting that all applicants pass a credit check could be held liable if it turns out that applicants from one protected group are disproportionately unlikely to have a sufficiently high credit score. That landlord would be held liable even though a satisfactory credit score is required of all potential tenants, regardless of race, and the landlord’s only intent was the (perfectly legal) desire to avoid tenants who would get behind on their rent—not to deny housing to any particular group.

In the decades since the FHA was passed, disparate impact has been used by the government and private litigants to exact tens of millions of dollars in fines and settlements from banks and developers whose facially neutral policies were alleged to have excluded members of a protected class from the housing market. The problem is that unlike with other anti-discrimination laws, such as the Americans with Disabilities Act—which expressly prohibits policies that have a disparate impact—the text of the FHA explicitly forbids only intentional discrimination.

Today we add the following essays to Cato’s online growth forum:

1. Enrico Moretti wants to increase the R&D tax credit.

2. Daniel Ikenson calls for more foreign investment.

3. Scott Sumner argues for better monetary policy based on nominal GDP targeting.

4. Don Peck worries about growing dysfunction in the middle class.

5. William Galston offers a potpourri of proposals for faster, more inclusive growth.

6. David Audretsch highlights the central importance of entrepreneurship.

The remaining essays will posted next week.

Dizzy

I’m so dizzy my head is spinning

Like a whirlpool it never ends

And its you, girl, making it spin

You’re making me dizzy*

Tell me I’m not with it, if you must, but the fact is that until a couple of days ago I’d never heard of Izabella Kaminska, who bills herself as a “finance blogger” and believer in something called the “collaborative economy,” in which sharing things takes the place of buying and selling them, the result being, she claims, a reduced carbon footprint.

Although I rather doubt that we’re likely to witness an end to our “propensity to truck and barter” anytime soon, I don’t doubt that such an event would in fact reduce carbon emissions: there would, for one thing, be a lot less less breathing going on. But what concerns me isn’t Ms. Kaminska’s general economic philosophy, to call it that. It’s her vertiginous spin on free banking, which she saw fit to air this past week, first on FT Alphaville, and then on a blog of her own called, appropriately enough, Dizzynomics.

All this might have gone happily unremarked had the Econ Blogosphere’s Grand Pooh Bah not seen fit to deem the last of these disorienting missives worthy of his readers’ attention. And so it happens that, Despicable Free Banking Nobody though I am, I find myself submitting, for The Rt. Hon. GPB’s consideration, my own humble post, the gist of which is that Ms. Kaminska hasn’t the foggiest idea what she’s talking about.

Because I addressed some errors in Ms. Kaminska’s FT post in comments to that post itself, I’ll embellish a bit here rather than repeat myself.

In discussing the founding of the Bank of England, Kaminska refers to the risk that “a private syndicate” took in “lending money to” the “UK” government. Let the anachronism pass. What matters is that the arrangement in question involved, not a loan directly made by the parties in question, but one made from the proceeds of a public stock offering, the lure for which consisted of monopoly powers the new Bank was expected to command. The stock sold in 12 days, and though the investors (again, not the scheme’s principals) could hardly avoid taking some risk, their gamble had every appearance of being a darn safe one. According to Sir John Clapham (History of the Bank of England i, p. 20), among the various projects being floated in those times, “the Bank with its Parliamentary backing, its high sounding name, and its guaranteed income from the taxes was a very attractive proposition. The speed of the subscription need not surprise those more familiar than any pamphleteer of 1695 could be with how and why men invest.”

I comment in the FT post itself on Kaminska’s suggestion that the Bank of England was particularly effective at enhancing England’s prosperity, so let me add here some brief excerpts from the source I referred to in that comment: Rondo Cameron’s chapters on “England” and “Scotland” from his edited volume, Banking in the Early Stages of Industrialization (Oxford University Press, 1967). “The English banking system from 1750 to 1844, ” Cameron observes, “was far from ideal in its contributions to either stability or growth of the economy as a whole.” Topping Cameron’s list of that system’s infirmities is the Bank of England itself, whose “contributions to industrial finance were negligible, if not negative.” Regarding Scotland Cameron says, in contrast, first, that despite having been “a poor country by any standard” in 1750, it “stood with England in the forefront of the world’s industrial nations” a century later, and, second, that “the superiority of its banking system stands out as one of the major determining factors” of this relatively rapid growth.

Ms. Kaminska’s estimate of the contribution of the Bank of England’s monopoly privileges toward British economic stability is just as unfounded as her opinion regarding its contribution toward British prosperity. “Before the Bank knew it,” she writes, “its notes had become the most liquid and trusted in the land.” Actually, because the Bank didn’t even bother to have branches beyond London before 1826, its notes were until that time seldom seen beyond the metropolis. (Nor, prior to the French wars, did the Bank issue notes for less than the princely sum of 10 quid.)

If the Old Lady’s notes were nonetheless judged safer than those of country banks, that was because those banks were severely under-capitalized and under-diversified. And why was that? Because they were not only denied Joint-Stock status, but subject to a rule limiting their ownership to six partners or fewer. In short the country banks–the only sort, remember, allowed to operate wherever the Bank of England chose not to–were by law prevented from achieving any reasonable degree of financial diversification and strength.

Here we see how, like most apologists for central banks, Ms. Kaminska fails to understand that the advantages commanded by such banks have as their precise counterpart limitations imposed upon all others. Little wonder so many English country banks fell victim to the Panic of 1825! Contrast, again, the situation in Scotland at the time, with three chartered banks and twenty-nine provincial ones, all commanding nationwide branch networks, and not one bank failure since a private bank failed in 1816–and even that one paying 19s on the pound! “Certainly Scotland,” Sir John observes, “appeared to have secrets of sound banking that England might inquire into.”

Ms. Kaminska is sanguine enough to allow that the Bank of England’s powers tempted it to engage in “imprudent money-printing.” But she spoils this lapse from her otherwise unalloyed confidence in the benevolence of state-sponsored monopolies by adding, gratuitously, that the bank was “not helped by the fact that [it] still had to compete with a whole bunch of private banks who were just as keen to issue money to an equally imprudent degree.” But, as I’ve noted, “compete” with “private” (meaning, presumably, country) banks is just what the Bank did not do, at least not until after 1826. Instead, by the terms of its charter it subjected them to inhibiting constraints, and then, having led them on by means of its own generous discounts, reversed course and…let them fend for themselves. (For evidence, see the relevant section of my article, “Bank Lending ‘Manias’ in Theory and History.”)

Kaminska can at least take credit for originality in reporting that, during the 1840s, “a terrible inflation” took hold in England, and that it was to combat that outbreak that Peel’s 1844 Act was passed. Alas, the claim owes its originality to the fact that there’s not an ounce of truth to it. The same may be said for her claim that the Scottish system was stable only because Scottish bankers “were so good at forging oligopolistic cartels that happily restricted competition.” As I noted in my FT comments, there’s no evidence that limited entry was a source of any significant monopoly power in Scottish banking. (On the contrary: the system was notoriously efficient.) Nor is there any evidence that Scottish banks policed one another other than by engaging in regular note exchanges, as they would have been no less compelled to do had entry into the industry been open. But let us assume, for the sake of argument, that Ms. Kaminska is correct in holding that oligopoly was the cause of the Scottish system’s superior stability. Then why, one wonders, does she not grant that a similar oligopoly might also have made England better off than it managed to be with its patently unstable blend of monopoly and hamstrung polypoly?

In 1833, thanks to a the efforts of the great Thomas Joplin, the terrible Six Partner Rule was partially circumvented by way of the discovery that its language encompassed note-issuing banks only, and not mere banks of deposit. The Bank of England thus faced for the first time competition from other joint-stock banks. Such are the facts. And what does Ms. Kaminska’s make of this development? First, that it came, not in 1833–that is, well ahead of Peel’s Act–but “in the latter half of the 19th century”; and, second, that it occurred, not because a clever banker discovered a loophole in the law aimed at severely restraining the Bank of England’s rivals, but supposedly because restrictions imposed by Peel’s Act on the Bank of England itself created “conditions” favoring the rise of “a new type of unregulated” bank. “Some history” indeed.

Ms. Kaminska concludes her remarks on English versus Scottish banking with a long excerpt from the Bank of England’s web pages, telling of how it “established the concept of lender of last resort” in the wake of the crises of 1866 and 1890. Had the “concept” thrust down its throat, by Walter Bagehot, is closer to the truth. What that great man had to say concerning the respective merits of the English (“one reserve”) and Scottish (“natural”) systems is, or ought to be, too well known to warrant repeating.

In her Dizzynomics follow up Ms. Kaminska adds little to the substance of her FT argument against free banking, such as it is, preferring instead to heap anathemas upon free bankers, who according to her reckoning are thick on the ground (were it only so!), and whom she regards as “reason and logic deniers” incapable of grasping the fact “that whenever we’ve had free-banking systems they’ve resulted in chaos or alternatively co-beneficial collusion to the point were the system is not free by the standard definition of free.”

No one, so far as I know, has ever claimed that the systems generally held out as examples of “free” banking–Scotland, of course, and Canada before 1914, among others–were perfectly so. Not me. Nor Kevin Dowd. Nor Larry White. Nor any other free banker I know. Of course those systems weren’t perfectly free. No banking system ever was. Nor has Hong Kong ever witnessed free trade in all its unsullied glory. So what? The question is always whether the examples come close enough to serve as evidence of the likely consequences of the fully-realized alternative. Was Scottish banking, to return to that case, “close enough” to shed light on the consequences of truly free banking? The debate on that question was joined some years back, with Larry White weighing in in the affirmative against the counterarguments of Murry Rothbard, Larry Sechrest, and Tyler Cowen and Randy Kroszner, among others. Ms. Kaminska, having found the opposition’s case neatly summarized in a blog post, simply overlooks White’s rejoinders. She overlooks as well the not-insignificant body of theoretical work using induction aided by deduction rather than deduction alone to draw inferences about the likely consequences of unalloyed freedom in banking.

Kaminska herself needs no theory, on the other hand, to reach the conclusion that genuinely free banking, unlike the Scottish mongrel, must lead to “chaos.” How can she know? As she offers neither evidence nor argument, one must hazard a guess. Mine is that she is referring to the U.S. banking system between the demise of the second Bank of the United States, in 1836, and the outbreak of the Civil War, and that she imagines, as many people do, that because a half-dozen states passed so-called “free banking” laws during that interval, it qualifies as one of perfect freedom from any sort of bank regulation. Excuse me for having had to suppress a yawn just now–it is a long post, after all, and fatigue is setting in, quite possibly for us both. Suffice to say, then, that old banking myths die hard, and that this especially hoary one about U.S. “free banking” seems harder to kill than Rasputin himself. That it is mostly hokum is nonetheless easily established: just have a look at any post-1975 work by an economic historian on the subject, including the locus classicus, Hugh Rockoff’s The Free Banking Era: A Re-Examination (Arno, 1975). (A later survey piece is here.)

A misreading of the same U.S. experience seems also to inform several of the obiter dicta that follow Kaminska’s opening thrust, including her claim that free bankers fail to “appreciate that it was standardizing certain subjective [?] values like weights, distances, time [sic] itself that has allowed society to cooperate, grow and thrive.” (Because antebellum state banking laws generally prohibited branching, state banknotes tended to be subjected to discounts when encountered any distance from their source; in contrast, in the Scottish and Canadian systems, where banks were free to establish branch networks, banknote discounts, if they ever existed, eventually disappeared. Ditto her belief that free bankers “advocate a Wild West model where no one can trust anyone and everyone has to do due diligence themselves.” (Though it’s true that the antebellum [old] west was inundated by all sorts of phony bank paper, that result came about, not because banking was unregulated there, but because territorial authorities, by having outlawed it, made their citizens perfect targets for phony notes purporting to come from legitimate banks down east. Where banking was more, though not perfectly, free, as in 19th century Canada or Scotland, in contrast, it sufficed to trust one bank, and to accept only those notes regarded as current at that bank, to avoid trouble.)

I hope I’ve said enough to suggest why I find it remarkable than anyone should take Ms. Kaminska’s ramblings on free banking (or, I now feel justified in saying, on any subject whatsoever) seriously. Perhaps no one does. Still I wish Tyler hadn’t given those ramblings more currency by advertising them, without the benefit of critical comment, on Marginal Revolution: here, surely, is a case where sharing adds to rather than subtracts from the world’s burden of hot air.

____________________

*Tommy Roe, “Dizzy.”

Related Tags

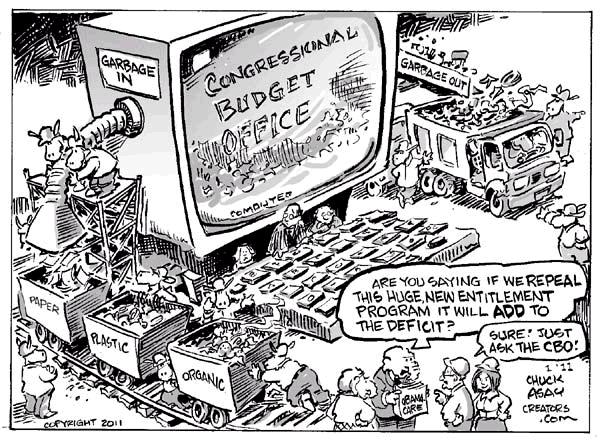

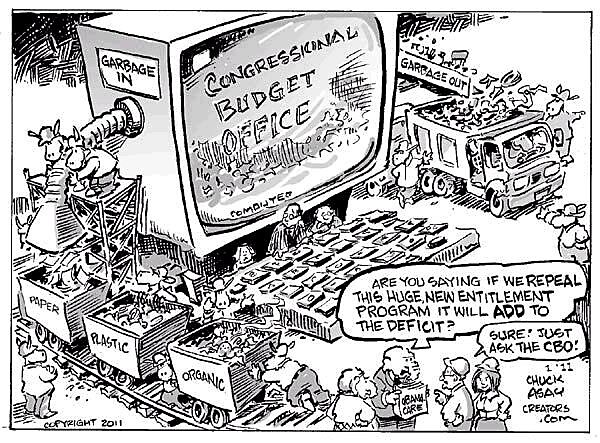

Since I’ve accused the Congressional Budget Office of “witch doctor economics and gypsy forecasting,” it’s obvious I’m not a big fan of the organization’s approach to fiscal analysis.

{kind=link}

I’ve even argued that Republicans shouldn’t cite CBO when the bureaucrats reach correct conclusions on policy (at least when such findings are based on bad Keynesian methodology).

So nobody should be surprised that I think the incoming Republican majority should install new leadership at CBO (and the Joint Committee on Taxation as well).

So why, then, are some advocates of smaller government — such as Greg Mankiw, Keith Hennessey, Alan Viard, and Michael Strain — arguing that Republicans should keep the current Director, Doug Elmendorf, who was appointed by the Democrats back in 2009?

Before answering that question, let’s look at some of what was written today for the Washington Post’s Wonkblog.