The 2017 Tax Cuts and Jobs Act (TCJA) was projected to lower revenue by $1.5 trillion over ten years by the Joint Committee on Taxation at the time of passage. However, because the law boosted investment, wages, and economic growth, revenues outperformed the static projections that didn’t account for the economy’s dynamic response to tax cuts.

The Tax Foundation’s dynamic projections from 2017 imply the tax cuts will have paid for themselves in 2028. Actual tax collections and current Congressional Budget Office (CBO) projections—which have been significantly affected by interceding legislation and unforeseen economic events—show that revenues have almost fully recovered from the 2017 cuts. However, making the TCJA permanent in 2025 without additional reforms would likely permanently lower revenue below the 2017 baseline.

The TCJA Could Have Paid for Itself, Eventually

A tax cut that boosts the economy and thus increases revenue growth above static government estimates will have three phases. Initially, revenues fall below the pre-tax cut baseline. If post-tax cut revenue grows faster than the pre-reform baseline, it will hit a break-even point. The tax cut will have paid for itself when the cumulative revenue losses from before the break-even point equal the higher revenues from after the break-even point.

If we accept the premise that some tax cuts result in a permanently larger economy, there is some subset of reforms that will result in a revenue break-even point. And if such a break-even point exists, the question is not if the tax cut pays for itself but when it pays for itself.

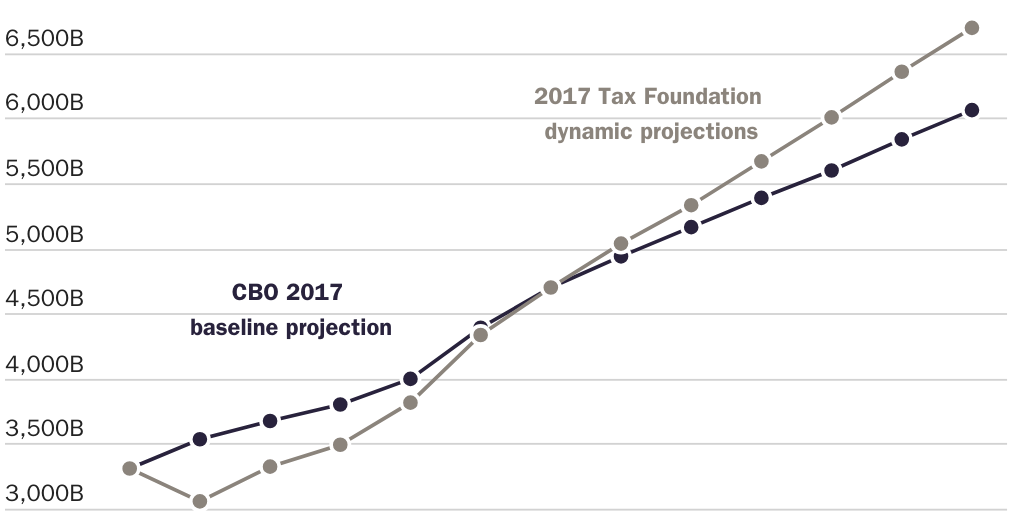

Figure 1 uses data from the Tax Foundation’s 2017 projections of federal revenue following the TCJA, adjusted for unanticipated inflation and projected past 2024 with a simple linear model.[1] The figure shows that compared to the CBO’s adjusted pre-tax cut baseline, revenues are close to breaking even in 2023 and surpass the 2017 baseline in 2024.

These extrapolated estimates imply the accumulated deficits from 2018–2023 ($1.4 trillion) will be fully offset by annual surpluses in 2028. This is due to the combined effect of economic growth and many temporary provisions that expire between 2022 and 2026. Assuming the law is made permanent, the break-even point is pushed back to roughly 2027, and the law pays for itself by 2033. Beyond 2033, the TCJA could be deficit-reducing.

These estimates likely understate the actual economic effects of the tax cuts and, thus, additional revenue due to the larger economy. Using actual firm responses to the tax cuts, Gabriel Chodorow-Reich and coauthors have estimated the TCJA will result in a long-run increase to the capital stock of 7.2 percent, roughly 50 percent larger than the Tax Foundation’s underlying estimates, which drive GDP growth.

The Actual Story is More Complicated

A recent Tax Foundation analysis of how federal tax revenue evolved since 2017 explains that revenue forecasting is a limited tool, made quickly obsolete by intervening events. In addition to unanticipated high inflation, “a growing trade war, a pandemic, a war in Europe, and a new conflict in the Middle East have each impacted tax revenues.” Congress implemented numerous tax changes in response to the pandemic, natural disasters, the CHIPS Act, and the Inflation Reduction Act, each of which lowered revenue collections. Higher-than-expected immigration has also boosted revenues more than government scorekeepers projected.

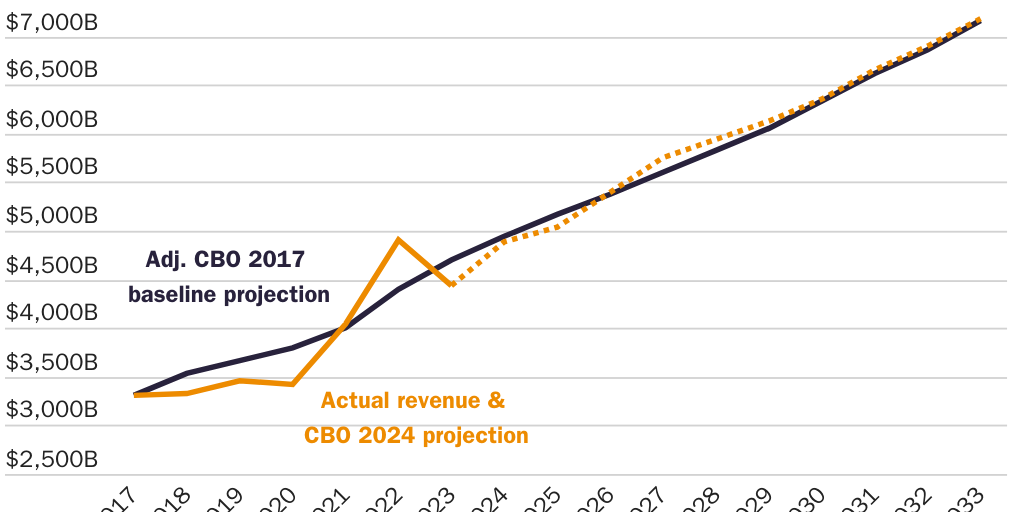

Figure 2 builds on the Tax Foundation’s methodology to show the inflation-adjusted CBO 2017 revenue forecast (adjusted for the unanticipated pandemic-era inflation), actual federal revenue through 2023, and CBO forecasted current-law revenue through 2033.

The data show that in 2021 and 2022, actual revenue surpassed the pre-TCJA CBO forecast due, in part, to the pandemic and changes to corporate taxes. However, revenue declined below the pre-TCJA forecast in the following year. Accepting all intervening economic and legislative changes that lowered revenues, actual revenues are projected to break even again in 2026 and then remain close to the pre-TCJA trend. The accumulated deficit (the gap between the 2017 baseline and actual revenue) between 2018 and 2025 is about $680 billion. By 2033, the total net deficit will fall to $220 billion, but the cumulative deficit is not currently projected to fall to zero.

The law’s many temporary provisions complicate assessing the long-run revenue effects of the TCJA. Making the tax cuts permanent in 2026 without additional reforms would permanently lower actual revenues below the 2017 CBO baseline.

Tax Cuts, Deficits, and Economic Growth

As the TCJA demonstrated, if the tax cuts are sufficiently pro-growth, positive revenues in later years can outweigh the initial deficit effects. However, if a tax cut is not sufficiently pro-growth, it will permanently reduce revenues. Ultimately, the goal of a tax cut should be to reduce revenue. If the resulting economic and behavioral effects of a tax cut are so large that it results in a fully offsetting increase in revenue, it means the tax rate is likely still too high and should be lowered further.

The most pro-growth tax cuts tend to be permanent changes that increase the after-tax return to investment, such as business expensing, lowering business taxes, and cutting capital gains taxes. These types of changes can be at least partly deficit-financed without worsening the long-run fiscal outlook (and could improve it).

Tax cuts for workers and consumers also have positive economic effects—such as encouraging additional work and entrepreneurship—but most are not sufficiently pro-growth to expect a larger economy to make up most of the lower revenue. Individual tax cuts are still worthwhile, but they should be paired with spending cuts to ensure the reduced revenue is sustainable.

As Congress prepares for the expiration of the TCJA, deficits and debt will dominate the discussion. Congress currently spends $2 trillion more than it raises in revenue, and no pro-growth tax cut can fix a $2 trillion (and growing) budget imbalance. To keep taxes low for the long run, Congress must decisively cut spending and prioritize the most pro-growth tax reforms.

[1] Tax Foundation’s adjusted 2017 projections from here. The adjusted CBO 2017 baseline uses the June 2017 baseline and March 2017 long-term budget outlook, adjusted using the accompanying economic assumptions. Original revenue projections are adjusted by an annual adjustment factor, which is the 2017 CPIU projection divided by the 2017 CPIU index projection inflated by the difference between projected and actual inflation rates or 2024 updated projections.