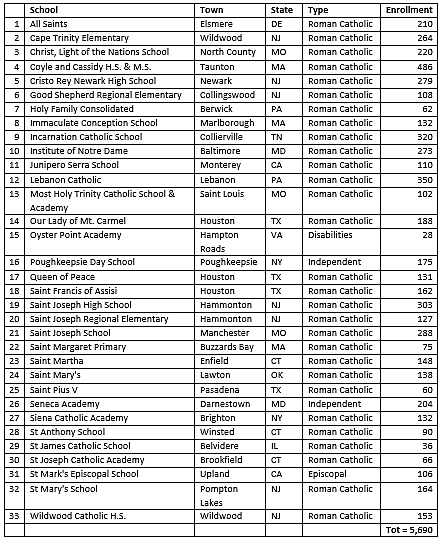

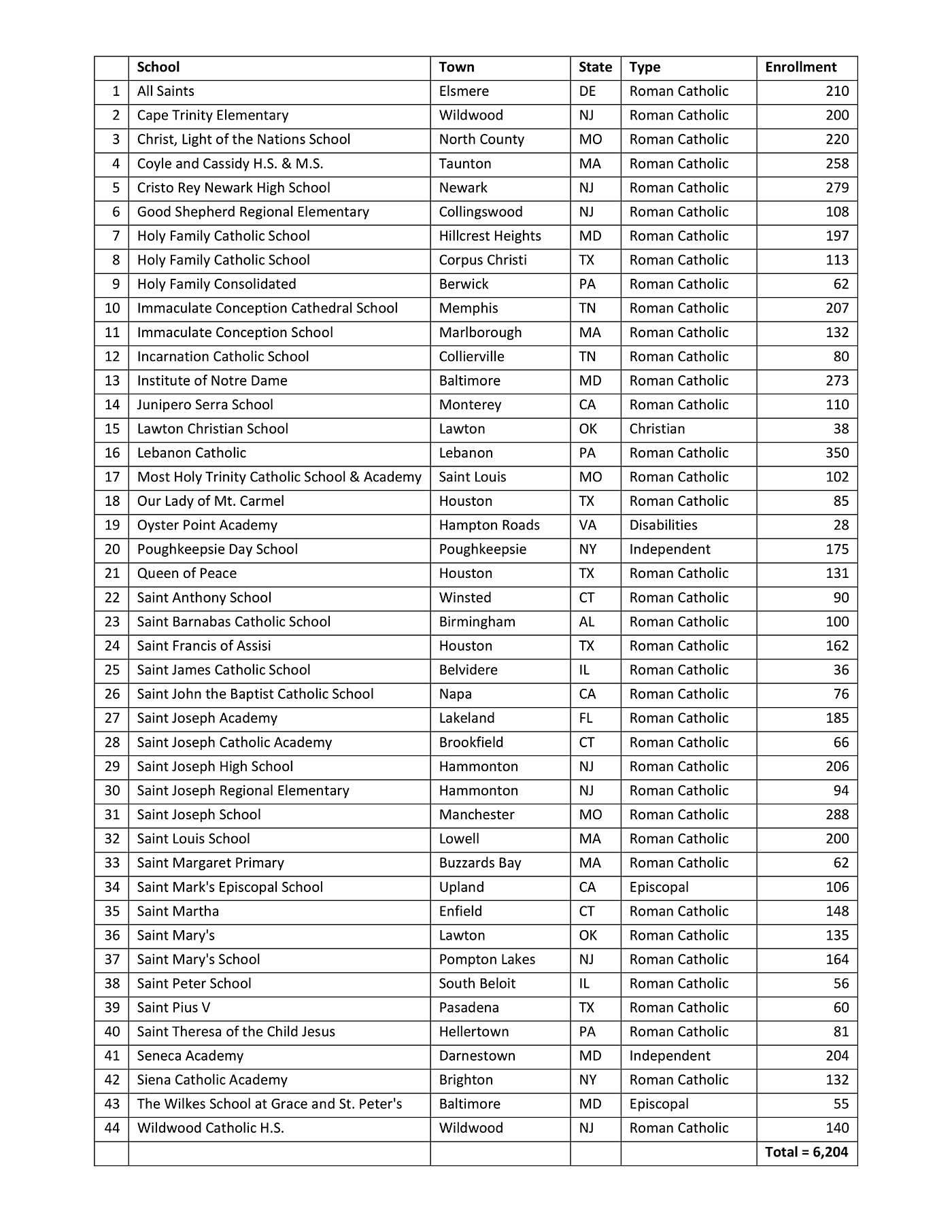

44 private schools have announced that they are closing permanently, at least in part due to the COVID-19 economic downturn, up from 33 in last week’s update. Enrollment in the closing schools, which in a few cases is estimated, is 6,204, up from 5,690 last week. Were all of these students to go to public schools, and had none been part of publicly connected school choice such as voucher programs or scholarship tax-credits, the new cost to the public purse would be roughly $96,000,000 ($15,424 per student multiplied by 6,204).

As always, the list is expected to grow as schools learn more about the impact of the economic downturn on enrollment and income for the coming school year. We will ordinarily post an update on Cato’s blog every Friday, but if the list reaches 100 schools we may transition to an online, searchable format. You can contact CEF director Neal McCluskey if you need more current numbers, if you know of permanent closures not on the list, or if you believe schools have been listed by mistake. We also welcome suggestions for improving the list.