If you’re a regular Alt‑M reader (and may the frost never afflict your spuds if you are), I needn’t tell you that I’m the last person to exalt the pre-2008 Federal Reserve System. Among other things, I blame that system for fueling the 2003–2006 boom, and for creating a credit famine afterwards. I also blame it for contributing to the dot.com boom of the 90s, for the rise of Too Big to Fail in the 80s, for the inflation of the 70s, and for the disintermediation crisis of 1966, to look no further back than that.

Yet for all its flaws that old-time Fed set-up was a veritable monetary Shangri-La compared to the one now in place. For while the newfangled Federal Reserve System is no less capable of mischief than the old one was, it also has the Fed playing a far larger role than before in commandeering and allocating scarce credit.

Monetary Control, Then and Now

You see, back in those (relatively) halcyon days, the Fed got by with what now seems like a modest-sized balance sheet, the liabilities of which consisted mainly of circulating Federal Reserve notes, supplemented by Treasury and GSE deposit balances and by bank reserve balances only slightly greater than the small amounts needed to meet banks’ legal reserve requirements. Because banks held few excess reserves, it took only modest adjustments to the size of the Fed’s balance sheet, achieved by means of open-market purchases or sales of short-term Treasury securities, to make credit more or less scarce, and thereby achieve the Fed’s immediate policy objectives. Specifically, by altering the supply of bank reserves, the Fed could influence the federal funds rate — the rate banks paid other banks to borrow reserves overnight — and so keep that rate on target.

Today, in contrast, the Fed presides over a vast portfolio, with assets consisting mainly of long-term Treasury securities and mortgage-backed securities, instead of the short-term Treasuries it once held; and that portfolio is funded more by banks’ holdings of substantial excess reserves than by circulating Federal Reserve notes. Yet instead of enhancing the Fed’s conventional powers of monetary control, the ballooning of the Fed’s balance sheet has sapped those powers by making it unnecessary for banks to routinely borrow from one another in the federal funds market to meet their legal reserve requirements. Consequently, the Fed can no longer target the effective federal funds rate, and influence other short-term interest rates, just by making modest changes to the stock of bank reserves.

So how does the Fed control credit now? Instead of increasing or reducing the availability of credit by adding to or subtracting from the supply of Fed deposit balances, the Fed now loosens or tightens credit by controlling financial institutions’ demand for such balances using a pair of new monetary control devices. By paying interest on excess reserves (IOER), the Fed rewards banks for keeping balances beyond what they need to meet their legal requirements; and by making overnight reverse repurchase agreements (ON-RRP) with various GSEs and money-market funds, it gets those institutions to lend funds to it.

Between them the IOER rate and the implicit ON-RRP rate define the upper and lower limits, respectively, of an effective federal funds rate target “range,” because most of the limited trading that now goes on in the federal funds market consists of overnight lending by GSEs (and the Federal Home Loan Banks especially), which are not eligible for IOER, to ordinary banks, which are. By raising its administered rates, the Fed encourages other financial institutions to maintain larger balances with it, instead of trading those balances for other interest-earning assets. Monetary tightening thus takes the form of a reduced money multiplier, rather than a reduced monetary base. The counterpart of that reduced multiplier is an increase in the Fed’s overall command of the public’s savings, for it’s the public that ultimately supplies the funds that financial institutions in turn hand over to the Fed, by holding those institutions’ IOUs.

Confiscatory Credit Control

As no one has yet come up with a catchy or at least convenient name for this new arrangement for credit control, allow me to propose one: “confiscatory credit control.” Why “confiscatory”? Because instead of limiting the overall availability of credit like it did in the past, the Fed now limits the credit available to other prospective borrowers by grabbing more for itself, which it then passes on to the U.S. Treasury and to housing agencies whose securities it purchases. When the central banks of other, and especially poorer, nations do this sort of thing, economists (including some who work for the Fed) refer to their policies, not as examples of enlightened monetary management, but as instances of financial repression. So it seems only fair to characterize our own central bank’s similar policies in a like manner. Although it’s true that financial repression has traditionally been practiced using the stick of high mandatory reserve requirements, whereas the Fed has instead been employing carrots in the shape of ON-RRP and IOER interest incentives, the ultimate result — more credit for the government, and less for everyone else — is the same. And though banks and bank depositors are better compensated for the governments’ takings, that compensation comes at taxpayers’ expense, because it translates either into an immediate reduction in Fed remittances to the Treasury or (as has been the case in fact) in an enhanced risk of reduced remittances in the future.

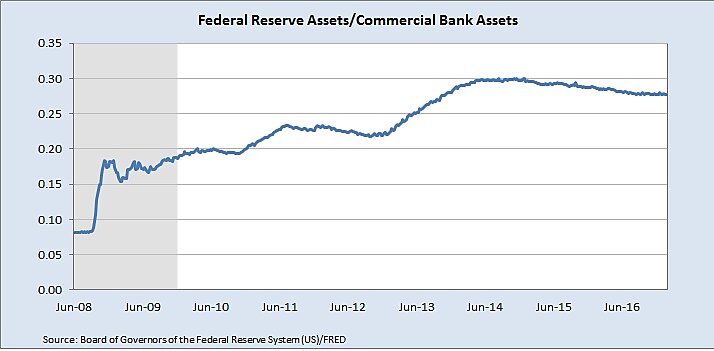

Whatever you call it, the Fed’s new monetary control framework involves a dramatic increase in the Fed’s credit footprint. To grasp the extent of the increase, have a gander at the chart below, showing the value of the Fed’s assets expressed as a percentage of total commercial bank assets. Whereas in the months prior to June 2008, Fed assets amounted to less than 8 percent of those held by U.S. commercial banks, its relative size has since increased five-fold. Of this overall increase, $2.5 trillion has gone into Treasury notes and bonds, while $1.75 trillion has been invested in MBS and housing-agency debt securities.

Thanks to the combined effects of LSAP’s, IOER, and ON-RRP, among other Fed programs and policies, the Fed now lords over a far greater share of the public’s savings than it has at any time since World War II, when it resolved “to use its powers to assure at all times an ample supply of funds for financing the war effort.” Even allowing, as many authorities do, that the Great Recession was a national crisis warranting a similar expansion of the Fed’s role, that fact alone can hardly continue to justify the Fed’s vast expansion now that the recovery is well-nigh complete.

Why should we mind a permanently enlarged Fed footprint? We should mind it because the Fed’s mandate doesn’t include commandeering a huge chunk of the public’s savings; and we should mind it because the Fed isn’t designed to employ our savings efficiently. Its business, like that of all modern central banks (but unlike that of, say, the Gosbank), is that of keeping the overall scale of credit creation within bounds consistent with macroeconomic stability, while leaving private financial institutions as free as is consistent with preserving that stability to decide how best to employ scarce credit.

The bigger the Fed’s credit footprint, the more it interferes with the efficient employment and pricing of credit. By directing a large share of savings to purchases of longer-term MBS and Treasury securities, for example, the Fed has artificially raised both the prices of those securities, and the importance of the housing market and the federal government relative to the rest of the U.S. economy. It has also dramatically increased its portfolio’s duration gap and, by so doing, the risk that it will suffer losses should it sell assets before they mature. In other words, the Fed has undermined its own flexibility, by increasing the likely cost, directly to the U.S. Treasury and indirectly to itself, of using open-market sales to tighten credit. Finally, by flattening the yield curve, the Fed’s purchases have harmed commercial banks, the profits of which come mainly from borrowing short, lending long, and pocketing the difference.

Promises, Promises

The presumption that the Fed’s credit footprint should be as small as possible was once shared by most experts, including Fed officials. For that reason, when QE was just getting started, and for some time afterwards, those officials were anxious to assure everyone that the Fed ‘s growth was only temporary.

In speaking at the LSE back in January 2009, for example, Ben Bernanke promised that

As lending programs are scaled back, the size of the Federal Reserve’s balance sheet will decline, implying a reduction in excess reserves and the monetary base. … As the size of the balance sheet and the quantity of excess reserves in the system decline, the Federal Reserve will be able to return to its traditional means of making monetary policy — namely, by setting a target for the federal funds rate.

Later that same year Fed Vice President Donald Kohn, speaking at a Shadow Open Market Committee meeting held here at the Cato Institute, complained that “the large volume of reserves is contributing to the loose relationship of our deposit rate and market rates,” while assuring those present that the Fed would eventually “drain the banking system of excess reserves for that reason.” [1] In their April 2010 meeting, most FOMC members hoped that the Fed would dispose of all its QE1 assets within 5 years of its first post-crisis rate hike, while a few wanted it to start selling assets before its first rate increase. A year later the FOMC was still committed to having the Fed dispose of its agency securities rapidly, so as “to minimize the extent to which the Federal Reserve portfolio might affect the allocation of credit across sectors of the economy.”

Finally, when, in 2014, the Fed began to increase the magnitude of its ON-RRP operations, some FOMC members worried about that facility’s influence on credit allocation. Nor were their concerns unwarranted. According to a study prepared by a group of Fed economists some months later, an enlarged ON-RRP program “would expand the Federal Reserve’s footprint in short-term funding markets and could alter the structure and functioning of those markets in ways that may be difficult to anticipate.” Among other things, Fed experts feared that, by substantially increasing the Federal Reserve’s role in financial intermediation, the new facility “might magnify strains in short-term funding markets during periods of financial stress.”

Alas, despite such concerns, and the progress of the recovery, the Fed has yet to take steps to shrink its balance sheet. Instead, it continues to reinvest both the proceeds from maturing Treasuries and principal payments from its agency debt and MBS. More disturbingly still, arguments to the effect that the Fed should make its gigantic footprint permanent, or even increase it, seem to be gaining ground both within and beyond the Fed. (An early convert to the new view was Ben Bernanke himself, who, at a May 2014 conference in which yours truly also took part, declared that “There is absolutely no need or requirement for the balance sheet to go back to normal as monetary policy normalizes. The balance sheet could be kept where it is for a very long time if necessary.”)

On the other hand, some other Fed officials, including St. Louis Fed President James Bullard, still hope to get the Fed to go on a diet. So, apparently, does Kentucky representative Andy Barr, who favors legislation that would give the Fed no choice but to shrink. Writing recently in Investor’s Business Daily, Barr observed that the Fed’s “enormous balance sheet puts taxpayers at risk, especially if interest rates rise, and distorts the free flow of capital that has sorely gone missing from our low-productivity recovery.”

The Demand Side of Fed Shrinkage

Barr hopes that pending legislation “will include an effective strategy to shrink the Federal Reserve’s balance sheet and limit its holdings to U.S. Treasuries.” If that’s what it’s going to take to cut the Fed back down to size, I’m for it as well. But Barr’s proposal begs the question, just what is an “effective strategy” for shrinking the Fed?

Most discussions treat such a strategy as being entirely a matter of setting a schedule, like those the FOMC has toyed with since 2010, for ending or limiting Fed re-investments of maturing securities and dividends, and (in more aggressive plans) for outright MBS sales. But there’s more to it than that, because the size of the Fed’s footprint is ultimately determined, not by the dollar-value of the Fed’s assets, but by the real demand for its liabilities. The greater the latter demand, the larger the Fed is bound to be in real (that is, inflation-adjusted) terms.

Just before the crisis, the demand for Fed liabilities consisted mainly of the public’s demand for paper dollars, about $800 billion of which were outstanding. The demand for Fed deposit balances, including banks’ demand for reserves, was, in contrast, quite limited. The Treasury and the GSEs kept modest balances amounting in all to about $100 billion, while banks held even less, in reserves barely exceeding minimum legal requirements. Today, thanks to IOER, ON-RRP, and other Federal Reserve programs and powers put into effect during the crisis, the demand for Fed balances has dramatically increased. Unless these special sources of demand are themselves dealt with, shrinking the Fed’s balance sheet alone won’t suffice to reduce the Fed’s size, either in real terms or relative to the credit system as a whole. Instead, Fed asset sales will, other things equal, cause private financial institutions to reduce their holdings of assets other than balances at the Fed, so as to retain the same ratio of Fed balances to other assets.

The good news is that reducing the demand for Fed balances to pre-crisis levels is relatively easy. Today’s exceptional demand is mainly the result of heightened bank liquidity needs combined with the Fed’s practice of setting the IOER rate above the yield on Treasury securities, and on short-term securities especially. Banks’ heightened liquidity needs initially stemmed from the crisis itself, but have since been sustained by the Fed’s liquidity stress testing and, more recently, by the U.S. implementation of Basel’s Liquidity Coverage Ratio.[2] But these needs alone don’t account for banks’ extraordinary demand for excess reserves, because Treasury securities are themselves high-quality liquid assets, which banks would normally favor over excess reserves for their higher yields. It’s only because the Fed has been paying IOER at rates exceeding those on many Treasury securities, and on short-term Treasury securities especially, that banks (especially large domestic and foreign banks) have chosen to hoard reserves. Even today, despite rate increases, the IOER rate of 75 basis points exceeds yields on most Treasury bills. Were it not for this difference, banks would trade their excess reserves for Treasury securities, causing unwanted Fed balances to be passed around like so many hot-potatoes, and creating new bank deposits in the process. Because more deposits means more required reserves, banks would eventually have no excess reserves to dispose of.

Phasing out ON-RRP, on the other hand, would eliminate the artificial boost that program has been giving to non-bank financial institutions’ demand for Fed balances.

Because phasing out ON-RRP makes more reserves available to banks, while reducing IOER rates reduces banks’ own demand for such reserves, both policies are expansionary. They don’t alter the total supply of Fed balances. Instead they serve to raise the money multiplier by adding to banks’ capacity and willingness to expand their own balance sheets by acquiring non-reserve assets. But this expansionary result is a feature, not a bug: as former Fed Vice Chairman Alan Blinder observed in December 2013, the greater the money multiplier, the more the Fed can shrink its balance sheet without over-tightening. In principle, so long as it sells enough securities, the Fed can reduce its ON-RRP and IOER rates, relative to prevailing market rates, without missing its ultimate policy targets.

In practice, the Fed may prefer (if it isn’t forced) to shrink its portfolio according to a preset schedule, rather than at whatever rate it takes to compensate for a declining demand for Fed balances. In that case, it has another tool it can use to keep a lid on credit: its Term Deposit Facility. As the Federal Reserve Board’s own description of that facility explains, by inducing banks to keep term (rather than demand) deposits with it, the Fed drains as many reserve balances from the banking system. So, to the extent that the Fed’s gradual asset sales fail to adequately compensate for a multiplier revival brought about by its scaling-back of ON-RRP and IOER, the Fed can take up the slack by sufficiently raising the return on its Term Deposits.

And the Fed’s federal funds rate target? What happens to that? In the first place, as the Fed scales back on ON-RRP and IOER, by allowing the rates paid through these arrangements to decline relative to short-term Treasury rates, its administered rates will become increasingly irrelevant. The same changes, together with concurrent assets sales, will make the effective federal funds rate more relevant, by reducing banks’ excess reserves and increasing overnight borrowing. While the changes are ongoing, the Fed would continue to post administered rates; but it could also revive its pre-crisis practice of announcing a single-valued effective funds rate target. In time, the latter target could once again be more-or-less precisely met, making it unnecessary for the Fed to continue referring to any target range.

____________________________

[1] Kohn also observed, by the way, that “the high volume of reserves evidently has not increased bank lending or reduced spreads of rates on bank loans or other assets relative to, say, Treasury rates,” while acknowledging that “an increase in lending and narrowing of spreads on bank loans is a necessary and desirable aspect of the return to better-functioning markets and intermediation to promote economic growth.” That sounds to me rather like an admission that QE was, up to that point at least, a flop.

[2] The Liquidity Coverage Ratio (LCR) calls for banks to have enough unencumbered “high quality liquid assets” (HQLA) to meet a 30-day stressed liquidity outflow scenario. Banks that rely heavily on wholesale funding are subject to a higher required LCR than those funded chiefly by retail deposits. The different requirements accounts for the fact that larger U.S. banks hold a disproportionate share of total excess reserves. Although the U.S. first began enforcing Basel-based LCR requirements in January 2015, it appears that U.S. banks that were to be subject to those requirements started accumulating qualifying liquid assets in 2013.