President Biden’s “war on junk fees” is only picking up steam. On May 9, the Senate Committee on Banking, Housing, and Urban Affairs held a hearing to focus on fees charged for financial services, and it unfortunately showcased many of the core problems with this “war.”

Senator Sherrod Brown (D‑OH) opened the hearing by claiming corporate greed was the reason for inflation and that financial services are plagued by junk fees that are “surprise, often last-minute charges that drive up the cost of products [with] no justification.”

There is a case to be made if financial institutions are handing customers receipts that say one price, but then charge those same customers something much higher behind their backs without any notice. In most cases, that would be fraud. Yet that doesn’t seem to be what he had in mind. Instead, Senator Brown pointed to credit card late fees saying, “Credit card late fees are the most costly and frequently applied junk fee.”

Yet late fees do not seem to track with Senator Brown’s definition of junk fees. For instance, how can a late fee be considered a surprise or without justification? As a penalty, late fees are common. As Representative Brad Sherman (D‑CA) pointed out earlier this year, if “you don’t pay the IRS on time, you expect a fee.” So late fees are hardly a surprise—especially considering the possibility of being charged fees must be disclosed up front. The justification is clear: a late fee is meant to recoup costs incurred due to a payment coming in late and discourage customers from being late in the future.

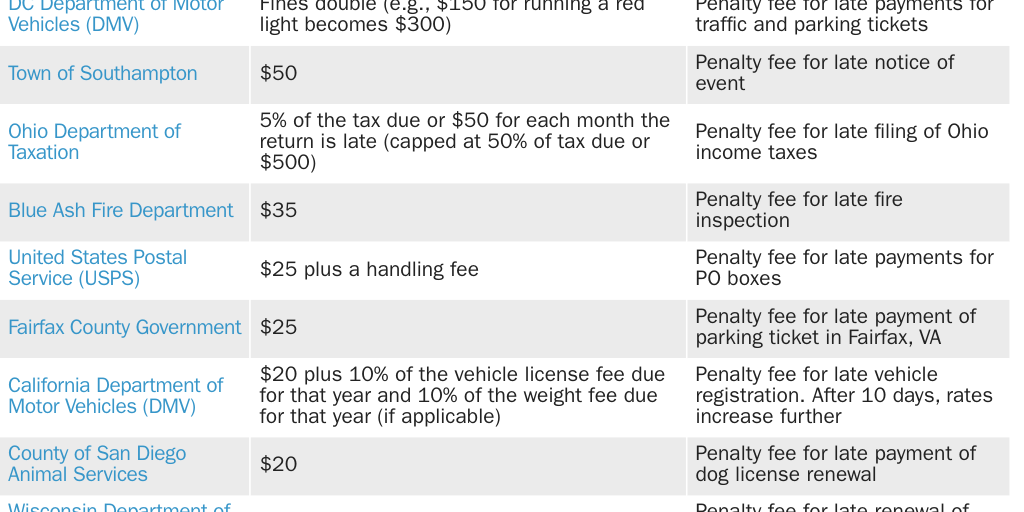

So, it’s a mystery how “late fees” can be termed “junk fees,” according to the senator’s definition. And it’s an even greater mystery how this definition can be used to restrict late fees in the private market and yet officials remain silent on late fees charged by the government (Table 1).

At a broader level, this example captures a wider issue with the Biden administration’s war on junk fees—something my colleagues Ryan Bourne and Sophia Bagley have described at length. The administration might wish the term “junk fee” was an established term to describe fees that are objectively wrong, but the administration has instead used it in practice to essentially describe anything it doesn’t like.

Senator Tim Scott (R‑SC) addressed this issue well at the hearing when he warned against taking the “politically expedient” route in calling for price controls:

Sure, it might be easy, or even politically expedient, to slap a label of “junk” or “excessive” on additional costs for legitimate products and services in an effort to villainize business in America…. But it is long past time that Democrats stopped playing political games with price controls and trying to micromanage the business operations.

Senator Scott is right. It’s too easy to fall back on the idea that the government simply needs to set the right price and everything will be okay. That’s not how things work in practice. The world is far too complicated and information changes far too much for any singular entity to plan the entire economy. Furthermore, as Ryan Bourne’s new book, The War on Prices, demonstrates, it doesn’t matter if we are talking about financial services or health care, price controls are bad policy.

Are you interested in learning more about how price controls distort the market? Ryan Bourne’s latest book, The War on Prices, is available here and features 24 chapters that will walk you through price controls large and small.