Washington, D.C.– Only 16% of Americans support the U.S. government adopting a Central Bank Digital Currency or “CBDC,” according to the new Cato Institute 2023 CBDC National Survey Report. The national survey of 2,000 Americans conducted by YouGov found that twice as many Americans—34%—oppose adopting a CBDC, while 49% don’t yet have an opinion. Nevertheless, the survey finds that Americans are more concerned about a CBDC’s risks than they are enthusiastic about its benefits.

The poll was conducted as officials at the Federal Reserve, the United States’ central bank, are considering whether the U.S. should adopt a central bank digital currency. While Americans regularly use digital dollars via credit cards, debit cards, etc, those dollars are a liability of the private commercial bank that issues them, like Bank of America or Wells Fargo. Conversely, a CBDC would be a liability of the government’s Federal Reserve, rather than a private bank. Thus, a CBDC would create a direct link between citizens and the government’s central bank.

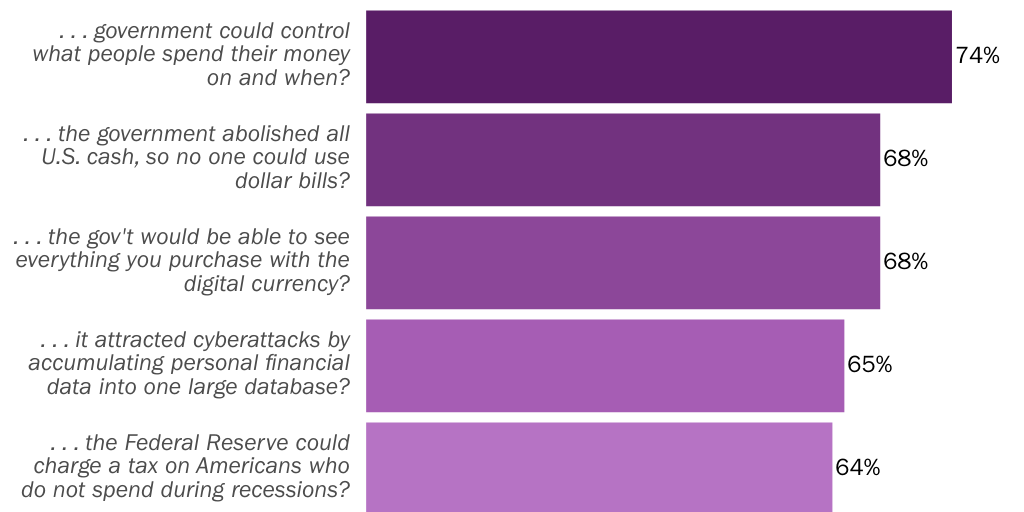

When Americans learn of the potential benefits and risks of a CBDC they express stronger opinions about whether the U.S. should adopt one. Strong majorities of Americans would oppose adopting a CBDC if it meant that the government could control what people spend their money on (74%), that the government could monitor their spending (68%), that a CBDC would lead to the abolishment of all U.S. cash (68%), that a CBDC would attract cyberattacks (65%), that the government could charge a tax on those who don’t spend money during recessions (64%), or that the government could freeze the digital bank accounts of political protesters (59%). Americans were marginally opposed (52%) if a CBDC would cause some people to stop using private banks, resulting in some banks going out of business.

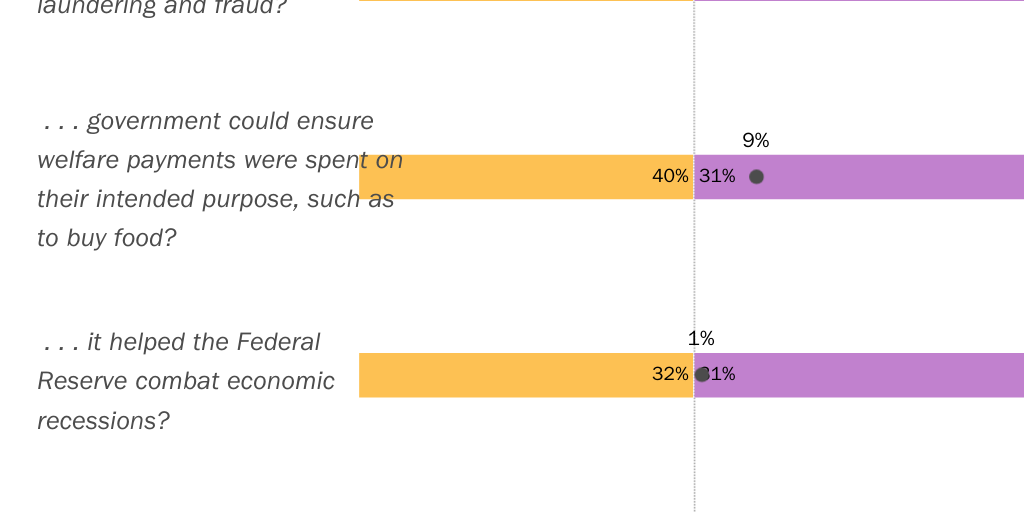

Americans express tepid support for a CBDC’s potential advantages. A plurality would support one if it reduced the risk of money laundering and fraud (42%) or if it meant that the government could ensure welfare payments were spent on their intended purpose (40%). Americans are about evenly supportive or opposed if a CBDC made instantaneous financial transactions possible (27% favor), made it easier for people without bank accounts to gain equitable access to the banking system (33% favor), or helped the Federal Reserve combat economic recessions (32% favor). In nearly each of these scenarios, about a quarter to a third of Americans still don’t have an opinion about a CBDC.

Both Republicans and Democrats are wary of CBDCs, but opposition is greater among Republicans. Before any benefits or costs are mentioned, a majority (53%) of Republicans oppose the government issuing a CBDC. On the other hand, a majority of Democrats (56%) are undecided and 22% oppose. Few Republicans (11%) and Democrats (22%) support adopting a CBDC. Additionally, strong majorities of both Democrats (71%) and Republicans (82%) would oppose a CBDC if the government could control what people spend their money on and when. Majorities of Democrats (61%) and Republicans (82%) would also oppose if the government could see what people buy with the digital currency.

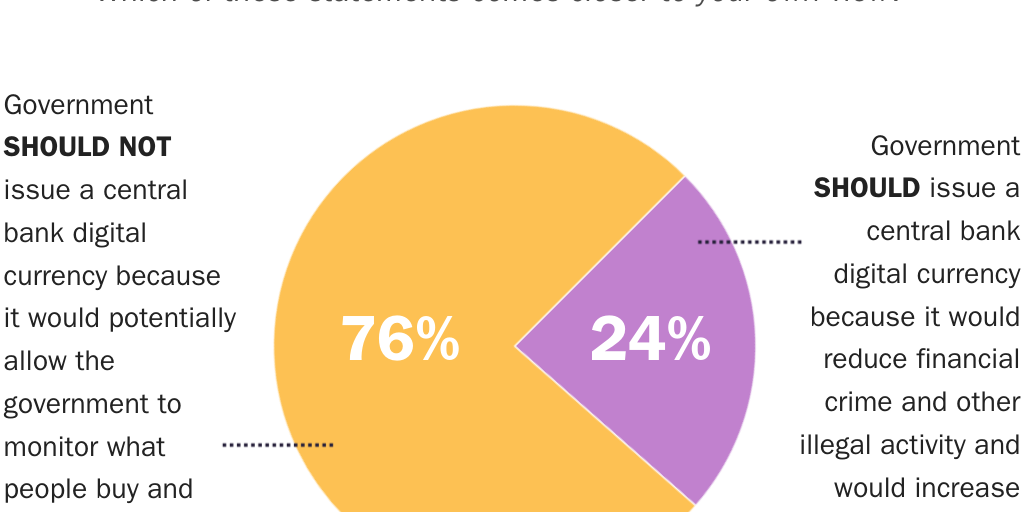

Most Americans are more concerned about CBDC’s potential risks than enthusiastic about the benefits when considered together: 76% of Americans say the “government should not issue a central bank digital currency because it would potentially allow the government to monitor what people buy and potentially control how they spend their money.” About a quarter (24%) say that the “government should issue a central bank digital currency because it would reduce financial crime and other illegal activity and would increase access to the financial system.”

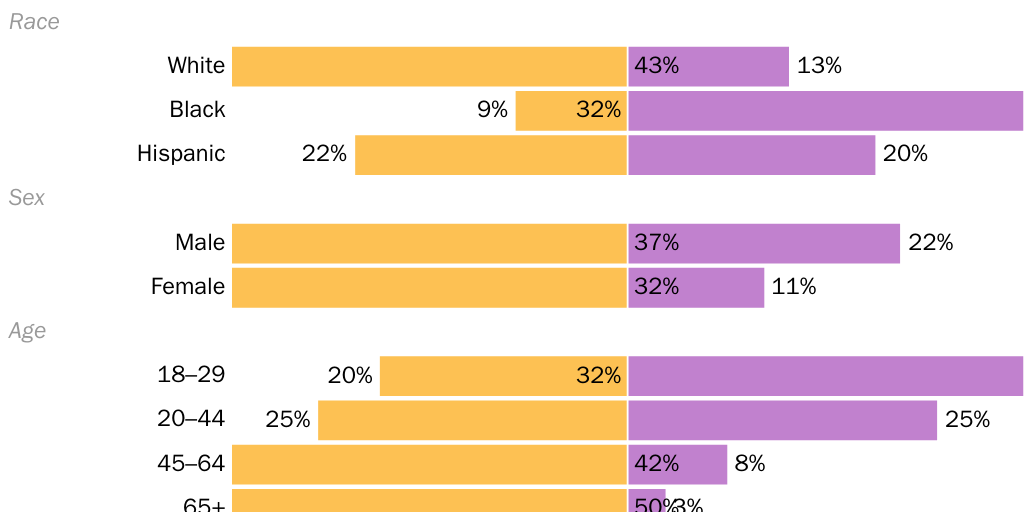

Nearly 8 in 10 Americans (78%) say they would not use a CBDC if one were offered, while 22% say they would. Some are more inclined to use a CBDC than others. Democrats (29%), Black Americans (39%), men (28%), and Americans under 35 (40%) were more likely than Republicans (16%), Hispanic (26%) or White Americans (18%), women (17%), and Americans over 55 (8%) to say they would use a CBDC.

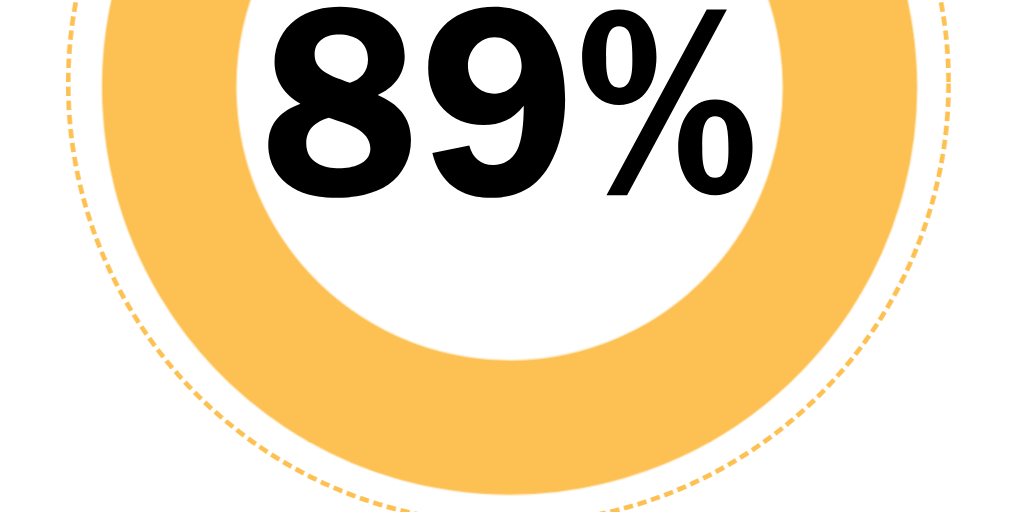

Americans are satisfied with their own bank (89%) and trust private banks more than the government to “handle [their] money appropriately” (79%). Further, 85% of Americans would prefer to keep their money with a private bank rather than in an account operated by the Federal Reserve (15%).

The survey also found that a CBDC is about as popular as 1984-style in-home government surveillance cameras. Only 14% of Americans support the government installing surveillance cameras in every household “to reduce domestic violence, abuse, and other illegal activity.” But strikingly–a majority (53%) of Americans who support a CBDC also support the government installing in-home surveillance cameras to reduce abuse and other illegal activity. This suggests that some of the psychology behind support for a CBDC springs from an above average comfort level with trading some personal autonomy and privacy for societal order and security.

The topline questionnaire, full methodology, and report of the survey findings can be found here. If you would like to speak to Dr. Ekins on the poll’s results, please contact pr@cato.org or 202–789-5200.