Earlier this week an unusual event took place: a U.S. shipyard delivered an oceangoing merchant ship. Named the Janet Marie, the vessel will transport goods between Hawaii and the U.S. mainland. Anyone tempted to toast the new ship as a symbol of U.S. shipbuilding prowess, however, should keep the champagne bottle corked. More an embarrassment than cause for celebration, the containership serves as a rich symbol of the heavily protected U.S. shipbuilding industry’s myriad shortcomings.

The most glaring problem with the Janet Marie is its price. Although the exact figure has not been published, its George III sister ship—a vessel delivered last year with the exact same specifications—was revealed to cost “$225 million-plus.” It’s a safe bet Janet Marie did not cost less. In comparison, two similarly-sized containerships were ordered from a South Korean shipyard in 2021 for $41 million each. The vast difference ($184 million) is no anomaly, comporting with previous assessments from maritime industry observers that U.S.-built cargo ships are five times the price of those constructed abroad.

The length of time required to build the Janet Marie provides another unfavorable contrast. From the time steel was cut until the ship’s delivery was approximately 50 months. In contrast, the Ever Alot—one of the largest containerships in the world with a cargo capacity nearly 10 times that of the Janet Marie (and a price tag $80 million lower)—required just 19 months to build. Originally slated for delivery in the third quarter of 2020, the Janet Marie is a full three years late.

Unfortunately, construction times significantly longer than those of foreign shipyards have been a feature of the U.S. shipbuilding industry for decades.

Faced with such high prices and lengthy construction times, the market for U.S.-built merchant ships is limited to those who must buy them to comply with the 1920 Jones Act, which requires vessels transporting goods within the United States to be constructed in U.S. shipyards. Understandably, these vessel operators delay purchasing new ships for as long as possible. Instead of buying new ships when existing ones approach the 20 year mark as is commonly done abroad, Jones Act-compliant ships are often not scrapped until age 40 or older.

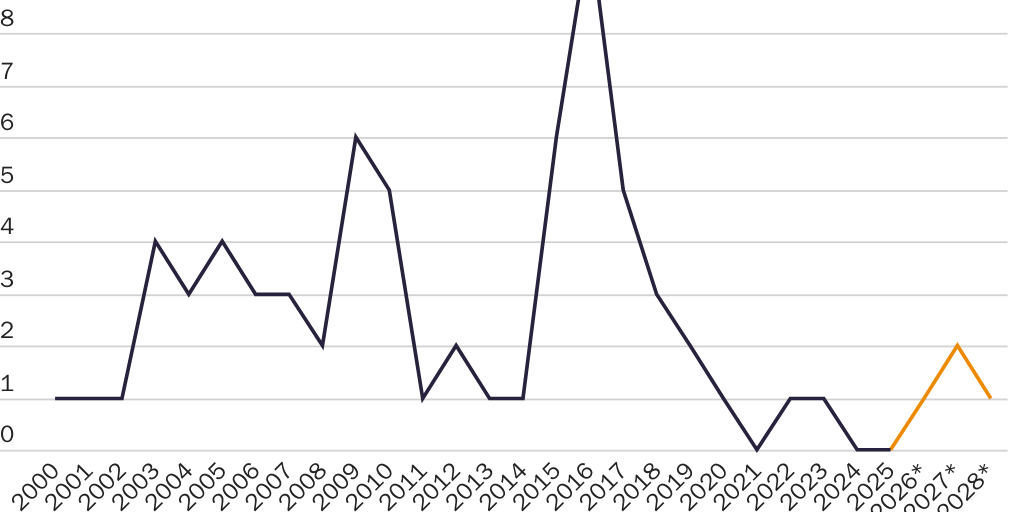

As a result, few ships are built. In fact, with the Janet Marie now delivered there are currently no merchant ships under construction in the United States (there are, however, three containerships on the order book slated for delivery in 2026 and 2027 at the astounding price of $333 million each).

Since 2000 deliveries of oceangoing merchant ships by U.S. shipyards combined have averaged fewer than three per year.

In comparison, a single shipyard in South Korea is slated to deliver 47 ships this year alone.

But it’s not just the large shipbuilders in Asia that have left protected American shipyards in the dust. Even European shipyards are churning out more vessels than those in the United States. Dutch shipyards, for example, delivered nearly 118,000 gross tons of merchant vessels in 2021 (latest available numbers) compared to less than 33,000 gross tons for U.S. shipyards. At 147,000 gross tons, Norway delivered almost five times the U.S. figure.

That U.S. shipyards produce so relatively little while charging so much should come to the surprise of no one. Having a captive Jones Act market means reduced incentive for U.S. shipyards to achieve the specialization and scale required for competition in the international market. It also means less competitive pressure—why be world-class when a lesser standard will suffice?

Another prominent factor is the large government contracts reserved for U.S. shipyards that many shipbuilders have prioritized at the expense of commercial shipbuilding. Indeed, the CEO of Overseas Shipholding Group, which operates Jones Act-compliant tankers, recently described the construction of commercial vessels to comply with the Jones Act as “a minor sideline interest” for most U.S. shipyards. His assessment appears borne out by the numbers, with a U.S. Maritime Administration study finding that government contracts accounted for nearly 80 percent of U.S. shipyard revenue in 2019.

Despite the U.S. shipbuilding industry’s extraordinary costs and trivial levels of output, some may believe that protectionism is nonetheless warranted to avoid U.S. reliance on foreigners for its shipbuilding needs. But the Jones Act doesn’t even do that. The Janet Marie’s sister ship delivered last year, for example, is chock full of foreign components. A sampling of the ship’s suppliers includes the China State Shipbuilding Corporation (supplier of the ship’s provision cranes), Alfa Laval (Qingdao) Ltd. (fired exhaust gas boiler), Zhenjiang Tongzhou Propeller Co. (fixed pitch propeller), and Jiangsu Xiangsheng Heavy Industries Co. (anchors and anchor chains).

That’s par for the course. Tankers built by the Philly Shipyard from 2004-06 required approximately 500 containers per vessel of material from South Korea as well as roughly 25 bulk shipments for larger items such as the main engine. While there is nothing wrong with relying on imported parts (imagine how costly these ships would be if all the components had to be U.S.-made as well!), notions that U.S. shipyards can produce ships without the need of foreigners is wishful thinking.

The Jones Act’s requirement that vessels used in domestic trade be constructed in U.S. shipyards fails to pass even the faintest whiff of a cost-benefit analysis. Among its harms include higher costs for those that must rely on these ships, added stress on infrastructure and congestion as transport is shifted to less expensive modes, irritated relations with U.S. trading partners and allies, and a smaller and older U.S. fleet than would otherwise be the case.

The other side of the ledger, meanwhile, consists of a commercial shipbuilding industry that punches well below its weight. Indeed, when the United States first required ships flying the U.S. flag to be domestically built U.S. merchant shipbuilders were among the world’s best and most competitive. Now they are a global afterthought, and there is good reason to think the industry would be better off without such heavy-handed protectionism.

Rather than a triumph, the Janet Marie offers a cautionary tale of protectionism’s heavy toll. The Jones Act’s U.S.-built requirement—if not the law entirely—should be discarded immediately.