At the end of my first post in this series, I observed that assessing the claim that fractional reserve banking causes business cycles meant asking two questions: first, “To what extent have historical money-fueled booms been associated, not with growth in the supply of either commodity money or central-bank supplied bank reserves, but with declining banking system reserve ratios?” and, second, “When a banking system does manage to operate on a lower reserve ratio, does its doing so necessarily contribute to an unsustainable boom?” I answer the first question here, leaving the second to a third and final installment.

The Myth of Bank Lending “Manias”: the 19th Century

That first question is empirical, so answering it means consulting the historical record. It happens that I did just that some years ago, in response to claims to the effect that bankers, far from being immune to bouts of what Alan Greenspan famously called “irrational exuberance,” often play a lead part in fueling unsustainable booms, leading the more common herd of speculators, not to mention many perfectly innocent parties, to their ultimate undoing.

I eventually published my findings in an article on “Bank Lending ‘Manias’ In Theory and History. Although I didn’t attempt anything approaching a comprehensive review of historical booms and busts in that brief survey, I did look at several of the most notorious cases of booms and busts commonly blamed on excessive commercial bank lending.

I also made a point of selecting those cases in which commercial banks were free to issue their own notes, so that they did not have to rely on notes supplied by a central bank to meet their customers’ demands for currency. The episodes that fit that description best are the Ayr Bank Crisis of 1772, the English Panic of 1825, the U.S. Panic of 1837, the Australian Crash of 1893. After carefully reviewing each episode, I concluded that

Available evidence from less restricted banking systems does not support the banking mania tradition. Banks not subject to legal limits on their issues have not taken advantage of this to allow their reserve ratios to fall during booms. Banks have tended to hold higher than usual reserve ratios in the aftermath of crises, perhaps in anticipation of extraordinary “leakages” of high-powered money. In short, if banks have behaved in any procyclical fashion, they have leaned in the direction of exceptional conservativism during slumps. When monetary expansion has “fanned the flames” of euphoria and planted the seeds of an eventual crisis, the expansion has generally been caused not by falling reserve ratios for competitive banks (as the mania thesis claims), but by exogenous injections of high-powered [i.e. “basic”] money. These injections have sometimes consisted of specie inflows; at other times they have consisted of the expanded liabilities of a central bank of issue.

The 20th Century

But what about other famous booms? Because fans of the Austrian cycle theory often refer to the 1920s boom as fitting the theory, let’s first consider it. Doing so is made difficult by the lack of any consistent figures for bank demand deposits and reserves: while data for total bank demand deposits go back to 1914, data for bank reserves are available only for Federal Reserve System member banks. Yet there are no data for demand deposits of member banks alone! Consequently, and most frustratingly, it’s impossible to know precisely what was happening to the overall reserve ratios of either commercial banks taken as a whole or of Fed member banks only.

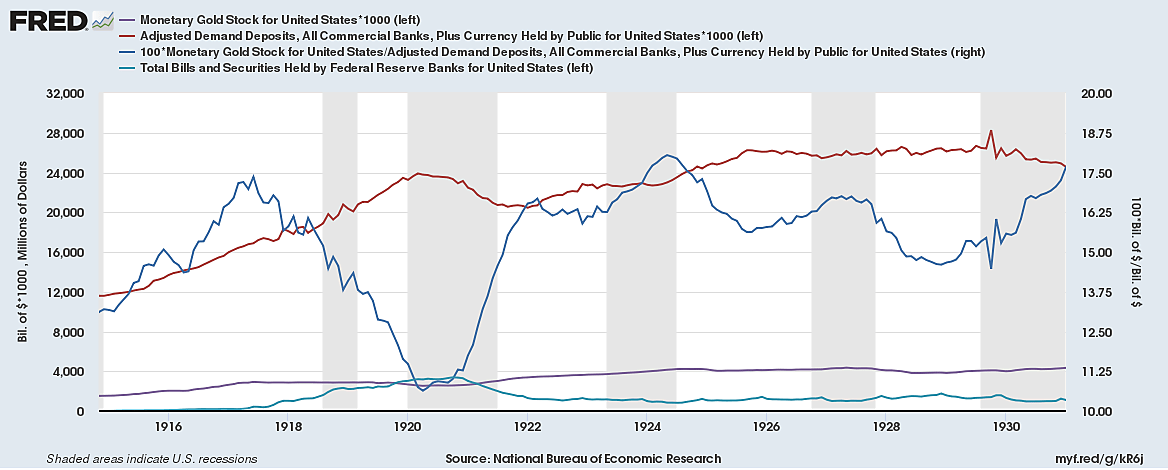

As an alternative way to gauge the role of fiduciary media in the lead-up to the Great Depression, the chart below shows, for 1914 (the first year for which consistent data are available) until 1930, the behavior of the following: (1) the U.S. money stock (demand deposits plus currency) (red line); (2) the stock of monetary gold (purple line); (3) total Federal Reserve “fiduciary” money creation, as measured by its holdings of commercial bills and Treasury securities (turquoise line); and (4) the relationship, expressed as a percentage, of the monetary gold stock to the broader money supply (blue line).

Although the chart does indeed appear to show a clear example of a “fiduciary media”-based boom, that boom occurs, not in the years leading to the Great Depression, but in those leading to the previous sharp but short-lived recession of 1920–21. Between the end of the war and the start of that recession the percentage of gold cover for the total money stock declined from almost 17.5 percent to less than 11.5 percent. The chart also shows how that decline was largely driven by Federal Reserve lending, which increased tenfold during the same period, from under $300 million to over $3 billion.

There’s no similarly clear evidence, on the other hand, of a fiduciary-media boom during the mid-to- late 1920s. After the ’20-’21 crisis, the gold cover percentage quickly recovered from its post-war decline. By May 1924 it had risen above 18 percent, a level exceeding its wartime peak. From there it declined, rose slightly, and declined again, to a not remarkably low nadir, in December 1928, of 14.6 percent, from which it proceeded to rise again until Black Tuesday. Finally, were one bold enough to venture that the modest decline of the gold cover percentage between May 1924 and December 1928 contributed importantly to an unsustainable boom, one would once again have to blame much of that decline on a substantial increase in Federal Reserve credit, the quantity of which doubled during the period in question, rather than on any fall in commercial bank reserve ratios.

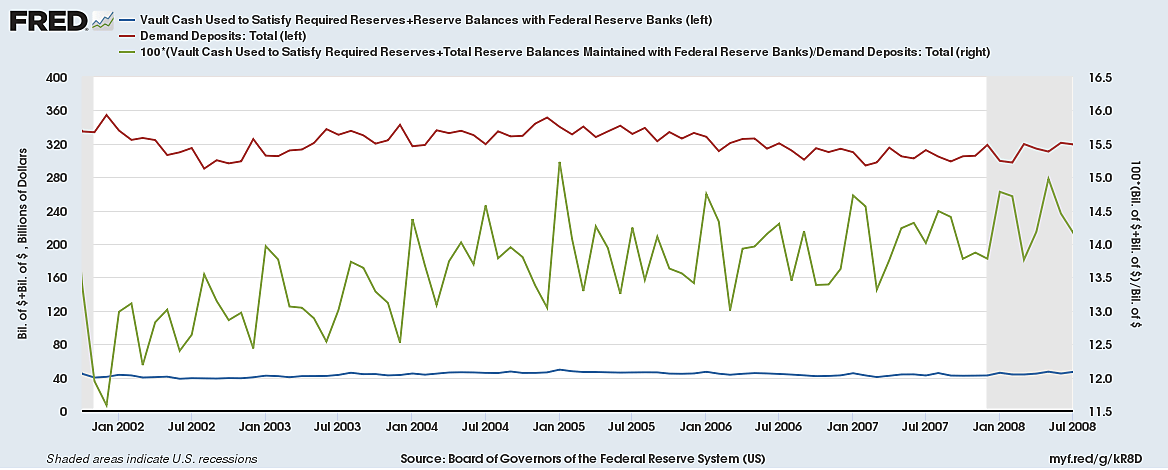

And what about the post-2001 subprime mortgage boom? Here the evidence is perfectly clear: the boom had nothing to do with growth in the supply of fiduciary media, as that term is conventionally defined. Another FRED chart should settle any doubts:

Remarkably, far from having been fueled by an increased in bank demand deposits unmatched by a corresponding increase in bank reserves, the great boom of the noughts did not even involve any substantial growth in the absolutely quantity of demand deposits, which for the most part fluctuated within the narrow range of $300 billion to $350 billion. (The series for “checkable” deposits behaves almost identically.) As for the percentage of demand deposits covered by bank reserves, including both vault cash and reserve balances at the Fed, instead of declining, it shows a distinct upward trend.

None of this is meant to deny that banks played some part in fueling the subprime boom. Bank lending and deposit expansion were certainly part of the story: by mid-2008 total bank deposits were half again their value at the start of 2002. But the deposits that grew during the boom weren’t demand deposits. Instead they consisted of various sorts of time deposits, which are not supposed, according to the standard Austrian account, to be particularly capable of causing unsustainable booms. It’s partly for that reason that most (though not quite all) Austrian-school calls for 100-percent reserve banking are calls for having banks keep 100-percent reserves against their demand deposits only, and not against time deposits

Maturity Mismatching: Healthy and Unhealthy

To his credit Philip Bagus — one of the Austrian-school critics of fractional-reserve banking — has argued quite correctly against the standard Austrian view that a 100-percent reserve system would not suffice to rule-out bank maturity mismatching and business cycles that result from it. That so-called “shadow” banks, none of which actually took part in the issuance of fiduciary media as Austrian economists define it, formed the epicenter of that crisis, supports’ Bagus’s claim.

However, Bagus himself errs in supposing that maturity mismatching itself is an inevitable cause of malinvestment. Here it helps to distinguish between what I’ll call, for want of accepted terms, “item-by-item” maturity mismatching from “aggregate” maturity mismatching. The difference is crucial in the case of financial intermediaries, the functions of which include gathering savings from large numbers of independent sources, and using those savings to fund various investments. How come? Well, suppose that I borrow $1000 from a friend, while agreeing to pay that friend back any time he or she wishes, and that I in turn lend the $1000 to someone who will not pay me back for a year. In that case, assuming I did not have any other assets or liabilities, I’d be engaging in a very risky act of one-on-one maturity mismatching.

But suppose I am a bank, with thousands of customers each of whom deposit (that is, lend the bank) $1000, also for undetermined periods, and that I have been receiving such deposits for a long time. In that case, over time I learn that, thanks to having so many depositors, the withdrawals of some tend to be made up for by the fresh deposits of others: in other words, the different depositors are like so many runners in a relay race, with those drawing on their balances passing the savings baton on, as it were, to others who are making new deposits.

The banks challenge, in that case, is not that of mismatching the maturity of any individual deposit with that of some corresponding bank loan, but one of matching the maturity of the banks assets with the expected availability of the totality of its deposits. In principal a well-managed bank only has to have loans enough being repaid on any given day to meet its net deposit withdrawals for that same day, where by adequately limiting the overall quantity of its lending it might in principal keep that expected net withdrawal right at zero.

In practice, though, bankers are bound often to lose more funds than they gain, if only on a day to day basis, with the opposite happening just as often. It’s precisely for that reason that banks have reason to maintain fractional cash reserves, while also limiting the maturity of the loans they do make — as they have every reason to do unless they or their creditors expect to be bailed out. The existence of fractional reserves in a competitive banking system subject to market discipline is, therefore, properly understood, not as a symptom of bankers’ tendency to engage in dangerous or excessive mismatching of the maturities of their assets and liabilities, but as a precaution taken against the risk of excessive mismatching.