America’s annual trade deficit continues to be among the most misunderstood features of the nation’s economy. Trade skeptics tend to blame the deficit for a range of problems, real or imagined, when in fact the current deficit in important ways reflects America’s underlying strength and influence in the world.

The latest example of misplaced worry about the deficit is a recent essay from The Claremont Institute on “Restoring American Manufacturing: A Practical Guide.” The essay attempts to pin at least part of the blame for the relative decline of U.S. manufacturing on persistent U.S. trade deficits. Author David P. Goldman argues that trade deficits also mean the accumulation of unsustainable “foreign debt”:

During the past thirty years, from 1992 through May of 2022, America’s trade balance on goods was a cumulative negative $18 trillion. That is exactly equal to America’s net foreign investment position, also $18 trillion. We have exchanged $18 trillion worth of Treasury bonds, corporate stocks, real estate, and other assets, for $18 trillion worth of goods.

A better term for “foreign debt” is “foreign investment.” In a new Cato Policy Analysis released today, “Balance of Trade, Balance of Power: How the Trade Deficit Reflects U.S. Influence in the World,” co-author Andreas Freytag and I explain that what ultimately drives the U.S. trade deficit is the annual net inflow of foreign investment to the United States. Through a persistent surplus in the financial account, foreigners help to finance a share of the federal government’s annual borrowing needs, while also investing in the productive private sector. As we explain in the paper:

The financial account surplus demonstrates confidence in the United States as a haven for global savings. Foreign investment keeps interest rates lower in the United States than they would be otherwise and provides capital to launch new businesses, to fuel research and development, and to expand output for existing firms.

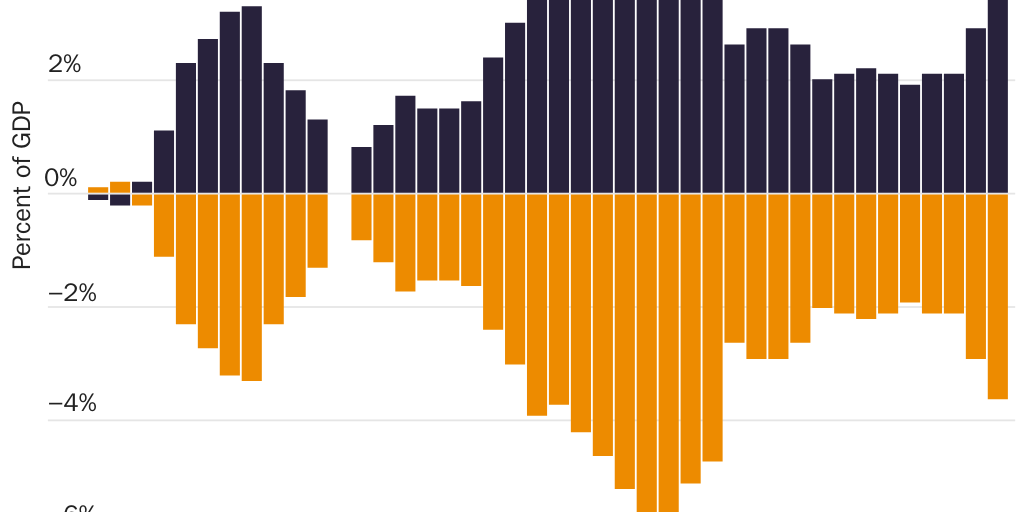

America’s net international investment position is easily sustainable. As we note in the paper, Americans run an annual surplus of more than $200 billion a year in primary income—U.S. earnings on foreign assets compared to what is paid out on foreign-owned assets in the United States. As we conclude, “The abiding confidence of global investors remains one of America’s greatest national assets—and the trade balance is a symptom of that strength.”

We go on in the paper to debunk myths about the deficit and “deindustrialization,” the alleged “de-dollarization” of global commerce, and the supposed decline of U.S. competitiveness. (The trade-skeptical American Compass raised similar fears about the trade deficit, which I critiqued in a previous blog post.)