Among last week’s news items that had colleagues asking me, “What’s your answer to this?,” was a piece by Quartz’s John Detrixhe, telling its readers that, according to “300 years of financial history,” rolling back bank regulations is a good way to trigger a financial meltdown.

Though you may be surprised to hear me say it, there’s some truth to Mr. Detrixhe’s thesis. While government intervention in banking typically does more harm than good, it’s also true that, unless it’s done carefully, deregulation can itself lead to trouble. As I put it some years ago in a Cato Journal article (reprinted recently in Money: Free and Unfree), “Dismantling bad bank regulations is like cutting wires in a time bomb: the job is risky and has to be done in carefully ordered steps, but it beats letting the thing go on ticking.”

Back in the 1980s, for example, when U.S. bank regulators phased-out depression-era regulation‑Q type restrictions on the interest rates depository institutions could pay to their depositors, they unwittingly freed a moral hazard genie that those regulations had kept bottled-up for several decades.

Did that make deregulating interest rates a bad idea? It didn’t, first of all because had those rates not been deregulated banks and S&Ls would have taken a licking from new Money Market funds, and also because regulators might have avoided the moral hazard problem by allowing banks to offer competitive interest rates on uninsured deposits only. The phasing-out of reg Q and its S&L counterparts would then have proceeded only to the extent that it went hand-in-hand with deregulation of another sort, namely, more limited deposit insurance, which would have gone a long way toward avoiding the S&L crisis later that decade. (And if you think banking stability depends on deposit insurance you really do need to review some non‑U.S. banking history.)

However, as the last example suggests, the fact that careless deregulation sometimes sets the stage for financial crises doesn’t mean that deregulation isn’t desirable, or that a deregulated banking system can’t be safe. On this point the three centuries of experience to which Mr. Detrixhe’s article refers speak eloquently, provided one bothers to consult the relevant case studies. Compare, for example, Canada’s banking system, especially between 1867 and 1935, to the system or systems of the U.S. Will anyone deny that Canada’s system was both far less heavily (and less heedlessly) regulated, and far more stable? The same conclusion holds for a comparison of the Scottish and English banking systems between 1772 (the year of the Ayr Bank’s failure, in which unwise regulation also played a part) and 1845 (when Scottish banks were compelled, for no good reason, to abide by Peel’s Bank Charter Act). Showing that misguided bank regulations were also an important cause of crises elsewhere than in the U.S. and England is also child’s play, provided one bothers to try. (Have a look for starters, at Charles Calomiris and Stephen Haber’s Fragile by Design.)

Not trying, especially by not even considering the performance of the world’s least-regulated banking systems, is the main reason why so many economists learn the wrong lessons from history. I made that point several years ago in reviewing Gary Gorton’s book, Misunderstanding Financial Crises; and I fear that what goes for Gary Gorton may go for Mr. Detrixhe as well.

Consider Detrixhe’s discussion of the Financial Crisis of 1825. In the years leading up to it, he notes, the prices of securities trading on the London Stock Exchange “were soaring, and members of parliament sat on the boards of some of the firms quoted on the exchange.” Quite true. But lax regulation of British banks had nothing to do with it. To the extent that England’s “country” banks (meaning all those apart from the privileged Bank of England) contributed to the boom, they did so, as I explained in my 1992 article “Bank Lending ‘Manias’ in Theory and History,” only by following the Bank of England’s lead:

The ratio of country note circulation to Bank of England issues remained within the narrow range of .64 to .663 for most of the years 1818 to 1825. The sole exceptions were 1823 and 1824 — the two years preceding the crisis — when the ratios were .572 and .588, respectively. These figures suggest that, insofar as country banks behaved unusually in the years just prior to the crisis, they did so by becoming more conservative than usual, resisting any impulse to extend their liabilities beyond levels consistent with available, liquid reserves of Bank of England notes.

The Bank of England, on the other hand, had been engaged since 1822 in what Elmer Wood (English Theories of Central Banking Control, p. 82) refers to as “a general plan for cheap money and credit expansion,” involving a reduction in its discount rate to 4 percent from its traditional value of 5 percent and an increase in the maximum maturity of bills eligible for discounting from 65 to 95 days. The country banks, and London discount houses, I observed in the above-mentioned article, having long been accustomed to treating Bank of England deposits and notes as so much cash, “could hardly be expected to do other than respond positively to the increased abundance of their own reserves, by reducing their own discount and deposit rates” (ibid.).

As for the Bank of England’s own capacity to fuel a bubble, that stemmed entirely from the Bank’s monopoly privileges, including its unique enjoyment of joint-stock status, and its monopoly of note issue within London and its surroundings.

As the Bank’s liabilities grew, its stock of bullion, which was just shy of £14 million in May 1824, declined continuously and rapidly. By the the end of 1825, it had fallen to just £1.26 million. When at last the Bank of England took steps to conserve its dwindling reserves, in part by once again raising its discount rate to 5%, the country banks, having been “kept in the dark about the status of the Bank’s bullion reserves” (ibid.), were among the firms and persons that bore the brunt of its policy reversal. “By the end of 1825,” Mr. Detrixhe observes, “markets were in a ‘full blown panic’…leading to bank runs and failures.” “A year later,” he continues, “nearly 10% of England’s banks had collapsed, sparking the first major global banking crisis.”

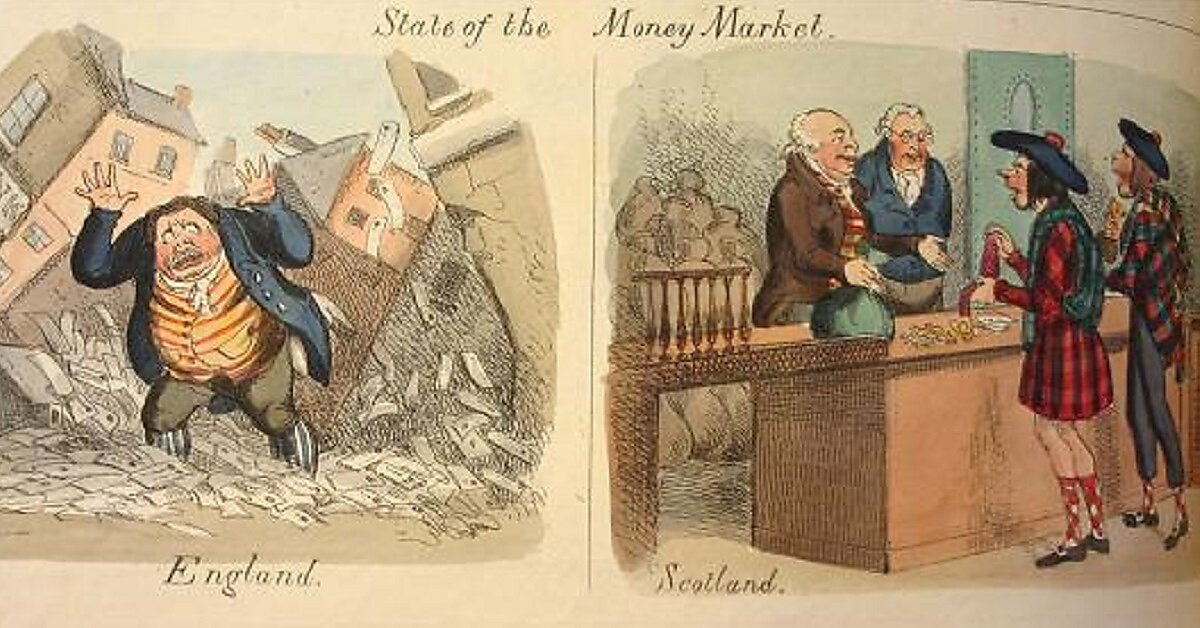

But did the 1825 Panic really trigger a global banking crisis? Not unless Scotland had somehow taken leave from planet earth, for as far as the British Isles were concerned, the banking crisis was an English and Welsh episode only; it left nary a trace in Scotland, whose bankers emerged from it unscathed. To a contemporary English cartoonist, the difference looked like this:

The different experiences of England and Wales on one hand and Scotland on the other reflected, not more heavy-handed regulation of the Scottish banks, but just the opposite. Most importantly, Scottish banks were, unlike their English and Welsh brethren, not subject to hampering restrictions on bank ownership, including the notorious six-partner rule. As Kevin Dowd explains (Laissez-Faire Banking, p. 35), Parliament had imposed that rule, limiting all English and Welsh banks apart from the Bank of England to six partners or less, back in 1709, as a means for reinforcing the Bank’s privileges in return for its having granted Parliament a subsidized loan. The measure

effectively prohibited reliable (that is, large) aggregations of capital in banking, as those partnerships that were allowed to enter the industry were too small to withstand any substantial shock. People knew how vulnerable the banks were and, whenever there was any disturbance, rushed to withdraw their gold (ibid.).

As Robert Jenkinson, the 2nd Lord Liverpool, told Parliament the year after the crisis, under the six-partner rule,

a cobbler or a cheesemonger, without any proof of his ability to meet them, might issue his notes, unrestricted by any check whatever; while, on the other hand, more than six persons, however respectable, were not permitted to become partners in a bank, with whose notes the whole business of a country might be transacted. Altogether, this system was one so absurd, both in theory and practice, that it would not appear to deserve the slightest support, if it was attentively considered, even for a single moment (ibid., pp. 47–8).

Thanks in part to Liverpool’s efforts, the absurd rule, enacted in the first place to gratify the Bank of England’s shareholders, was finally scrapped. In the ensuing decades, 138 English joint-stock banks were established, of which only 19 either failed or went into voluntary liquidation prior to the passage of Peel’s Act in 1844 (Newton n.d., p. 4). I hope I’m right in thinking that Mr. Detrixhe, had he also been an MP in 1826, would not have been tempted to plead for sticking to the six-partner rule on the grounds that getting rid of it would increase the risk of another financial meltdown.

Certainly Mr. Detrixhe can’t be accused of favoring any sort of government regulation. He recognizes, for example, that U.S. government housing policies contributed to the recent panic. On the other hand he seems to believe that the Dodd-Frank Act’s many provisions are capable of preventing another crisis, if only Republicans will let them stand, whereas in truth those provisions hardly address any of that crisis’s root causes.

And although Mr. Detrixhe never actually claims that the subprime meltdown itself illustrates the supposedly general tendency for panics to follow deregulation, one suspects that he, like many others, believes this to be the case. But while many have blamed the crisis on deregulation, and especially on the partial 1999 rollback of Glass-Steagall, such claims seem to be based on little more than their authors’ preconceived notions. A close look at the evidence suggests, on the contrary, that although the crisis had many causes, deregulation wasn’t one of them.

So let’s by all means learn as much as we can from 300 years of financial history. But let’s also remember that to do so one must delve deep into that history, and not just skim the surface.