|

GRADE

|

TOOK OFFICE:

LEGISLATURE:

|

State government budgets have grown substantially in recent years with the influx of federal aid during the COVID-19 pandemic. That aid has now started to wane, but rising tax revenues have fueled continued budget growth. At the same time, large surpluses in many states have prompted the passage of major tax cuts and reforms.

That is the backdrop to this year’s 17th biennial fiscal report card on the governors, which examines state budget actions since 2022. It uses statistical data to grade the governors on their tax and spending records: Governors who restrained taxes and spending receive higher grades, while governors who substantially increased taxes and spending receive lower grades.

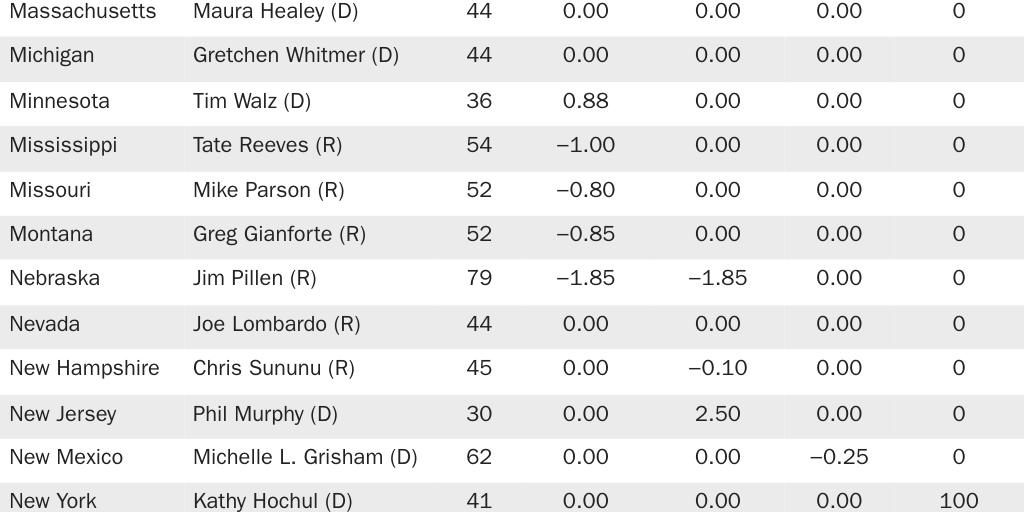

Six governors receive a grade of A: Kim Reynolds of Iowa, Jim Pillen of Nebraska, Jim Justice of West Virginia, Sarah Huckabee Sanders of Arkansas, Kristi Noem of South Dakota, and Greg Gianforte of Montana. Six governors receive an F: Tony Evers of Wisconsin, John Carney of Delaware, Jay Inslee of Washington, Janet Mills of Maine, Kathy Hochul of New York, and Tim Walz of Minnesota.

This report examines the tax and spending choices made by the nation’s governors and discusses recent policy trends. To spur growth, half the states have cut their individual or corporate income tax rates in recent years, and some states have converted their multirate individual income taxes into single-rate flat taxes. Unfortunately, many states have also been larding their tax codes with special interest breaks for filmmaking, green energy, and other politically favored industries.

Another trend affecting state budgets is the expansion of school choice programs. More than 30 states now provide support for private schooling through various tax and spending mechanisms. A dozen states have made eligibility for their school choice programs universal or near universal for all students.

Most states are enjoying surpluses today, but they differ in their budget preparations for tomorrow. Debt levels, rainy day funds, and unfunded retirement obligations vary widely by state. These state variations and overall fiscal trends are discussed in the body of the report, and the fiscal actions of each governor are discussed in Appendix B.

Introduction

Governors play a key role in state fiscal policy. They propose budgets, recommend tax changes, and sign or veto tax and spending bills. When the economy is growing, governors can use rising revenues to expand programs or they can return extra revenues to the public through tax cuts. When the economy slows and budgets go into deficit, governors can respond by raising taxes or trimming spending.

This report grades governors on their fiscal policies from a limited-government perspective. Governors receiving an A are those who have cut taxes and spending the most, whereas governors receiving an F have increased taxes and spending the most. The grading mechanism is based on seven variables: two spending variables, one revenue variable, and four tax-rate variables. Cato’s state fiscal report has used the same methodology since 2008.

The results are data driven. They account for tax and spending actions that affect short-term budgets in the states. However, they do not account for longer-term or structural changes that governors may make, such as reforms to state pension plans. Thus, the results provide one measure of how fiscally conservative each governor is, but they do not reflect all the fiscal actions that governors take.

Tax and spending data for the report come from the National Association of State Budget Officers (NASBO), the National Conference of State Legislatures, the Tax Foundation, the budget agencies of each state, and news articles. The data cover the period from January 2022 to August 2024.1 The report rates 48 governors. It excludes the governor of Louisiana because he has been in office only a brief time, and the governor of Alaska because of peculiarities in that state’s budget.

The next section discusses the highest-scoring governors. Subsequent sections examine trends in revenues and tax policy, business subsidies, school choice reforms, and state debt levels. Appendix A discusses the methodology used to grade the governors. Appendix B provides summaries of the fiscal records of the 48 governors included in the report.

Main Results

Highest-Scoring Governors

Table 1 presents the overall grades for the governors. Scores ranging from 0 to 100 were calculated for each governor based on seven tax and spending variables. Scores closer to 100 indicate governors who favor smaller government policies. The numerical scores were converted to the letter grades A to F.

The following six governors received grades of A:

- Kim Reynolds of Iowa has been a lean budgeter and dedicated tax reformer since entering office in 2017. She received the highest score on this report. Iowa general fund spending has risen at just 2.3 percent annually since Reynolds took office. She has greatly simplified and reduced Iowa’s income taxes. The individual income tax was converted from a nine-bracket system with a top rate of 8.98 percent to a 3.8 percent flat tax; the corporate tax rate was slashed from 9.8 percent to 5.5 percent. The governor also approved school choice reforms allowing all students to opt for education savings accounts (ESAs) to cover private schooling costs.

- Jim Pillen of Nebraska is a veterinarian and entrepreneur elected governor in 2022. He cut the corporate tax rate and top individual income tax rate from a planned 5.84 percent to 3.99 percent, to be phased in by 2027. He also ended taxes on Social Security benefits, allowed businesses to expense their equipment purchases, and achieved major property tax reductions.

- Jim Justice of West Virginia is a wealthy entrepreneur elected governor in 2016. For years, he pushed to cut the income tax to increase growth and attract residents to his state. The legislature acceded in 2023 and passed, as he put it, the “largest tax cut in West Virginia history.”2 Individual income tax rates were cut across the board, with the top rate cut from 6.5 percent to 4.9 percent. It is the largest tax cut relative to state tax revenues in this year’s report. Justice also approved school choice reforms allowing all students to opt for ESAs to cover private schooling costs.

- Sarah Huckabee Sanders of Arkansas has pursued major tax reforms since her election in 2022. In a series of bills, she cut the top individual income tax rate from 4.9 percent to 3.9 percent and the corporate rate from 5.3 percent to 4.3 percent. Sanders says she is “committed to responsibly phasing out our state income tax rate and letting everyone keep more of their hard-earned money.”3 She has kept the lid on spending increases and Arkansas has one of the largest rainy day funds in the nation. Sanders also approved major school choice reforms in 2023 based on ESAs and universal eligibility.

- Kristi Noem of South Dakota has defended her state’s low-tax policies since her election in 2018. As one of the freest states in the nation, South Dakota enjoys net domestic in-migration, while most of its neighbors suffer out-migration. Noem cut the general sales tax rate from 4.5 percent to 4.2 percent—a significant reduction, as the state has no income tax and relies heavily on sales taxes. Noem consistently proposes flat budgets.

- Greg Gianforte was elected Montana governor in 2020. He was determined to cut income tax rates and succeeded in a series of bills. In 2021, he cut the top individual income tax rate from 6.9 percent to 6.5 percent and collapsed seven income tax brackets to two. He expanded the standard deduction and repealed tax credits. Further reforms in 2023 cut the top individual income tax rate to 5.9 percent. He has also cut the capital gains tax rate and increased the exemption level for taxing business equipment.

All the governors receiving an A on this year’s report are Republicans, and all the governors receiving an F are Democrats. Republican governors tend to focus more on tax cuts and spending restraint than do Democrats. In Table 1, the Republicans had an average score of 56 and the Democrats an average score of 42. On reports going back to 2008, Republican and Democratic governors had average scores of 56 and 43, respectively.

When the economy is growing and revenues are rising, Democrats tend to increase spending, whereas Republicans tend to both increase spending and cut taxes. Recently, state budget surpluses have been so large that both Republicans and Democrats have cut taxes, although the Democratic cuts have often been one-time rebates, which are scored lower on this report than the permanent cuts favored by Republicans.

Trends in Revenues and Tax Policy

During the COVID-19 pandemic in 2020, news stories portrayed state governments as facing disaster from falling tax revenues and slashed public services. That narrative provided support for federal policymakers to pass $1 trillion in aid for the states in a series of bills in 2020 and 2021.4

However, that doom‐and‐gloom outlook was unwarranted. Large aid packages were not needed because state and local tax revenues grew during that time. Tax revenues were flat in 2020 but then soared in 2021 and 2022 before leveling off again. Estimated state and local tax revenues of $2.47 trillion in 2024 are up 28 percent from the 2019 level of $1.93 trillion. Meanwhile, federal aid to the states jumped by 52 percent, from $684 billion in 2019 to an estimated $1.04 trillion in 2024.5

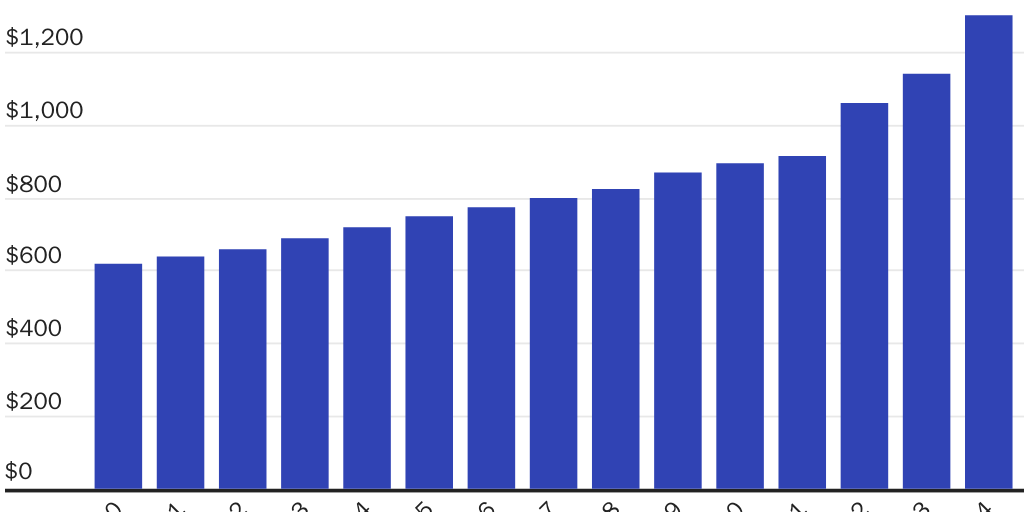

The jumps in aid and tax revenues have generated large state budget surpluses, which have been used to expand spending, cut taxes, and fill rainy day funds. Across the 50 states, general fund spending soared by 46 percent between 2020 and 2024, as shown in Figure 1.

State rainy day fund balances increased from 8.6 percent of state expenditures in 2020 to 11.9 percent of state expenditures in 2024.6 However, rainy day funds vary widely. In 2024, Alaska, Arkansas, Kentucky, New Mexico, North Dakota, and Wyoming had rainy day funds of 25 percent or more, but Delaware, Illinois, and New Jersey had rainy day funds of 5 percent or less. The former states are prepared in case of a recession; the latter states are not.

Overall, the states enacted net tax hikes every year from 2016 to 2021, but then enacted net tax cuts in 2022, 2023, and 2024.7 The quality of the tax cuts has varied widely. Many states have reduced tax rates and simplified tax structures to boost growth. However, many states have expanded special interest tax breaks, which has made tax codes more complex and distorted the economy.

The big news is that a wave of income tax rate cuts has swept the states. Of the 41 states that have individual income taxes, 21 cut the top rate between 2021 and 2024. Some of the largest cuts were signed by Sarah Huckabee Sanders of Arkansas, Brian Kemp of Georgia, Brad Little of Idaho, Kim Reynolds of Iowa, Tate Reeves of Mississippi, Greg Gianforte of Montana, Jim Pillen of Nebraska, Henry McMaster of South Carolina, and Jim Justice of West Virginia.

Among the states with individual income taxes, 13 have single-rate flat taxes and 28 have multirate systems.8 Some states have always had single rates, but Colorado was the first state to switch—in 1987—from a multirate system to a flat tax.9 Three more states switched to flat taxes between 2007 and 2019: Kentucky, North Carolina, and Utah. And since 2021, five more states switched to flat taxes: Arizona, Georgia, Idaho, Iowa, and Mississippi.

Some governors, including Reynolds of Iowa and Justice of West Virginia, are proposing repealing their income taxes entirely. That may sound radical, but a diverse group of nine states—Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming—have prospered for decades without individual income taxes.10

From 2021 to 2024, 14 states cut their corporate income tax rates. Among current governors, the largest cuts were signed by Sanders of Arkansas, Kemp of Georgia, Little of Idaho, Reynolds of Iowa, Pillen of Nebraska, and Roy Cooper of North Carolina. Corporate income taxes are highly complex and discourage investment, and since the corporate tax burden ultimately lands on individuals, it is simpler to eliminate corporate taxes and collect needed revenues directly from individuals.

Growth in Business Subsidies

Many states are cutting taxes in ways that distort the economy and increase tax-code complexity. States have added narrow breaks for businesses in film production, green energy, housing, manufacturing, agriculture, data centers, and many other industries. States are handing out these breaks under their income tax, property tax, and sales tax systems.

New York has a tax credit for digital games businesses, and Virginia has a tax credit for vineyards. California has a tax credit for cannabis businesses, and Georgia allocates more than $1 billion a year to film tax credits.11 New Jersey recently enacted a special tax credit for artificial intelligence businesses.12 Such tax breaks, along with government grants and loans to businesses, are often called subsidies or incentives.

There are different estimates of the magnitude of state incentives, but there is agreement that incentives have mushroomed. A 2012 New York Times investigation found 1,874 state incentive programs costing about $80 billion a year.13 A more recent estimate by the Mercatus Center puts the figure at around $95 billion.14

Good Jobs First estimates that states have created 1,408 business incentive programs.15 The Council for Community and Economic Research estimates that there are 2,420 such programs, of which about half are tax breaks and about half are spending subsidies.16 The group found that the number of incentive programs has more than doubled since 2000.17 Economist Tim Bartik estimates that state incentive programs have roughly tripled in cost since 1990.18

Virginia has 92 business incentive programs including tax credits, tax exemptions, and grants. A November 2023 state report noted, “Almost half of the currently active incentives were adopted since 2010.”19 Scholars at the Lincoln Institute of Land Policy found that few states used tax abatements, tax increment financing, or enterprise zones in the 1960s, but that a great majority of states use them today.20

Moreover, rising federal tax complexity is generating rising state tax complexity. Recent federal legislation has created an array of new tax breaks and subsidies for semiconductors, renewable energy, batteries, and other industries. These complicated and distortionary federal breaks have prompted the states to create similar breaks in their own tax codes.

The spread of state business incentives is a troubling move toward crony capitalism and away from free markets. Here are seven ways in which economic development incentives are harmful.

Central Planning. Special interest incentives presume that politicians know how to allocate resources across industries to produce more value than if markets had allocated those resources. But there is no reason to believe that—markets use prices, profits, and other feedback mechanisms for allocating resources to generate net value, while governments rely on guesswork and lobbyist pleading to make their allocation decisions.

Unfairness. When the government provides subsidies to some businesses, other businesses are put at a disadvantage. Unsubsidized businesses producing similar products and businesses sourcing inputs in the same markets as subsidized businesses are especially harmed. When a large company uses subsidies to boost hiring, for example, it puts upward wage pressure on nearby businesses. Rather than creating winners and losers with subsidies, governments should aim for equal treatment of all businesses.

Big Companies over Small. Politicians often claim to support small businesses, but most subsidies go to big corporations. In Virginia over the past decade, the largest 7 percent of state incentive awards accounted for more than 80 percent of all state awards.21 Good Jobs First counted 23 state corporate subsidy megadeals across the states in 2023 worth more than $50 million each.22 Delaware recently enacted an incentive program to grow greenhouse fruits and vegetables—but only for businesses that invest more than $40 million in facilities of more than 400,000 square feet.23 Why advantage large greenhouses over small ones?

Business Diversity Undermined. If a state has a budget surplus, it could use the funds to subsidize a handful of big corporate projects, or it could trim the general corporate tax rate and boost investment incentives for thousands of firms in a variety of industries. The former strategy puts the economic development eggs in a few baskets, which is risky because the future is unknown. The latter strategy is more likely to succeed because it encourages many diverse investment experiments. Why has Silicon Valley been successful? Not because of a few big companies, but because it has been a vast incubator for tens of thousands of start-ups.

Corruption Fostered. Allowing governments to provide narrow business incentives opens the door to corruption because the incentives can get swapped for campaign cash and bribes. State film tax credits, low-income housing tax credits, and other special interest breaks have been hit by corruption scandals in numerous states.24 Incentive programs are complex and rely on political discretion, which creates a breeding ground for corruption. And to compound the problem, the more businesses that receive subsidies, the more that other businesses will lobby for handouts for themselves.

Productivity Undermined. Just as low-income welfare undermines individual productivity, corporate welfare undermines business productivity. Companies receiving subsidies allow their costs to bloat, and shift their focus to short-term political gains and away from long-term marketplace gains. Governor Jared Polis handed out $4.9 million to a Swiss company to make solar panels in Colorado, but the credits are contingent on the company “meeting net new job creation and salary requirements.”25 But that requirement will undermine the company’s incentive to improve labor productivity over the eight-year life of the deal. More generally, subsidies induce companies to make bad business decisions. Ford Motor’s massive investment in electric vehicles, which was largely induced by federal subsidies, has cost the company billions of dollars in losses.26

Complexity. The rules for special interest tax breaks are usually complex. For example, the rules for the federal low-income housing tax credit paid to developers span 2,060 pages.27 This federal credit has spawned similar state-level credits in half the states, thus creating further complexity. States create bureaucracies to administer such incentives and ensure that businesses follow the rules and create promised benefits. A simpler way to generate growth is to cut tax rates for all businesses.

Many states—illogically—create incentives to draw investment to selected industries but then impose high general tax rates, discouraging overall investment. Interestingly, there is a statistical correlation across the states between the number of special interest incentive programs and scores on the Tax Foundation’s business tax climate index, which assigns higher scores to states with low-rate, neutral tax systems.28 States with high index scores provide relatively fewer incentives, and vice versa.

In sum, trying to spur economic development with business subsidies and narrow tax breaks is wasteful. To achieve broad-based economic growth, states should restrain spending and cut overall tax rates to encourage a diverse range of entrepreneurial and investment activities.

School Choice Reforms

School choice reforms are spreading across the nation. Governments in more than 30 states now provide financial support for private K–12 schooling through at least four types of programs.29

First, some states offer vouchers to parents to help cover tuition at private schools.

Second, some states fund education savings accounts (ESAs), which parents use to cover tuition costs at private schools and other schooling expenses. Some ESA programs are funded by private tax-advantaged contributions.

Third, some states allow for tax-credit scholarships, which provide tax credits for donations to nonprofit groups that fund private school scholarships.

Fourth, some states provide individual income tax credits or deductions to parents to help them recoup the costs of private schools.

The momentum in recent years has been to enact ESA-based school choice programs. School choice reforms began gaining ground a dozen years ago, but programs were originally limited to students from lower-income families or in failing schools. Many states have recently broadened eligibility for their school choice programs. About 1 million students are currently benefiting from these reforms, and 12 states have now made eligibility for their school choice programs universal or near universal for all families.30

What are the fiscal effects of school choice programs? Spending on the programs still represents a small share of overall school spending. Arizona’s ESA program enrolled 77,571 students in 2024 at a cost of $759 million, which is about 5 percent of public school spending in the state.31 Iowa’s ESA program enrolled 16,757 students in 2024 at a cost of $124 million, which is less than 2 percent of public school spending in the state.32

As choice programs grow, states should reduce funding for public schools that have declining pupil counts. Taxpayers should enjoy savings because the average per pupil costs of choice programs are much less than the costs of public schools. In Iowa, the average per pupil ESA funding is $7,413, which compares to $15,283 for the average per pupil public school cost.33 In Arizona, the average per pupil ESA funding is $9,785.34 That compares to the $13,541 average per pupil public school cost in that state.

Over time, ESAs should reduce the overall costs of K–12 education. Some public school costs are fixed in the near term but can be cut in the longer term as public school enrollment falls. Also, while some ESA pupils had previously been enrolled in private schools that are paid for privately, most have switched over from public schools.35 An analysis for Iowa taking these factors into account found that the 2023–2024 cohort of ESA students will save taxpayers a net $55 million a year.36

The main goal of school choice programs is to improve education quality with competition and innovation.37 However, the fiscal benefits to government budgets may also be substantial, given that the nation’s public school spending is about $900 billion a year.38

Debt Varies Widely by State

State and local governments are major investors in infrastructure such as highways, bridges, and schools. A portion of the investment is financed by debt in the form of state and local bonds. The interest and principal on the bonds are paid back over time from either taxes or user fees.

However, debt is not the only way to finance infrastructure. Much state-local infrastructure is funded on a pay-as-you-go basis. That approach entails governments looking ahead and planning to construct facilities over time with an allocated portion of annual tax revenues. Pay-as-you-go financing is preferable to debt because it creates less financial risk for governments and future taxpayers.

States impose other financial risks on future taxpayers in addition to bond debt. They incur unfunded retirement obligations, which include pension benefits and other post-employment benefits (OPEB), for their workers. OPEB consist mainly of promised future retirement health benefits for government workers.

Bond debt and unfunded retirement obligations vary widely by state. Table 2 shows state government debt and unfunded obligations in 2022 measured as a percentage of state gross domestic product (GDP). The data come from Truth in Accounting.39

The differences in total liabilities between the lowest and highest states are huge. The lowest-liability states owe less than 3 percent of GDP, whereas the highest-liability states owe 20 percent or more of GDP.

The states with the lowest total liabilities are Arizona, Idaho, Nebraska, Tennessee, Utah, Wisconsin, and Wyoming; the states with the highest liabilities are Connecticut, Hawaii, Illinois, New Jersey, and Vermont. There are similar patterns across the states for debt, pension liabilities, and OPEB liabilities. For example, New Jersey is far above average for all three types of liability, while Nebraska is far below average for all three types. Note that these are only state-level liability data points and do not include local government liabilities.

Most state liabilities were accumulated before current governors took office. But governors of highly indebted states such as New Jersey should be taking action to pay down debt and unfunded obligations. To reduce bond debt, governors should restrain spending and shift infrastructure investment to pay-as-you-go funding. In addition, some infrastructure, such as airports, could be privatized and the funding removed from government accounts entirely.40

Governors should also pursue reforms to retirement plans. Reforms should trim benefits in defined benefit (DB) pension and OPEB plans, and workers should be required to contribute a greater share of wages toward their own future benefits.

Also, government workers should be transitioned from DB plans to defined contribution (DC) plans, like the 401(k) plans offered in the private sector. States that have transitioned new employees from DB to DC pension plans include Alaska in 2006, Michigan in 1997, Oklahoma in 2015, and North Dakota in 2023.

Some states, including Colorado, Florida, Indiana, Montana, North Dakota, Ohio, and South Carolina, provide workers the option of using a DC plan as their primary retirement benefit. However, most states continue to rely on DB plans, which create unnecessary risks for taxpayers because large funding gaps may be closed down the road with tax increases.

Appendix A: Report Card Methodology

This study computes a grade for each governor based on his or her success at restraining taxes and spending since 2022, or since 2023 for governors who entered office that year. The spending data mainly come from the National Association of State Budget Officers but in some cases they come from the budget documents of individual states. The data on proposed, enacted, and vetoed tax changes come from NASBO, the National Conference of State Legislatures, state budgets, and news articles.41 Tax rate data come from the Tax Foundation and other sources.

This year’s report uses the same methodology as all reports dating back to 2008. It focuses on short-term taxing and spending actions to judge whether governors take a small-government or big-government approach. Each governor’s performance is measured using seven variables: two for spending, one for revenue, and four for tax rates. Their overall score is calculated as the average of their scores in those three categories. Tables A.1 and A.2 summarize the governors’ scores.

Spending Variables

- Average annual percentage change in per capita general fund spending proposed by the governor.

- Average annual percentage change in per capita general fund spending enacted.

Revenue Variable

- Average annual dollar value of proposed, enacted, and vetoed tax changes. This variable is measured by summing estimates of the annual dollar effects of tax changes as a percentage of a state’s total tax revenues. For example, vetoing a $50 million tax increase would boost a governor’s score the same amount as approving a $50 million tax cut. This is an important variable, and it is compiled from many news articles, budget documents, and reports.42 Temporary tax changes were valued at one-quarter the value as permanent tax changes.

Tax Rate Variables

- Change in the top personal income tax rate approved by the governor.

- Change in the top corporate income tax rate approved by the governor.

- Change in the general sales tax rate approved by the governor.

- Change in the cigarette tax rate approved by the governor.

The two spending variables are measured on a per capita basis. Also, the spending variables measure only changes in the general fund portions of budgets, which governors have the most control over. Variable 1 is measured through FY 2025, and variable 2 is measured through FY 2024. Variables 3 through 7 cover changes from January 2022 to August 2024, or from January 2023 to August 2024 for governors who entered office in 2023.

For each variable, the results are standardized so that the worst scores are near 0 and the best scores are near 100. The scores for each of the three categories—spending, revenue, and tax rates—are calculated as the average score of the variables within the category, with one exception: The cigarette tax rate variable is quarter-weighted because that tax is a smaller source of state revenue than the other taxes measured in its category. The average of the scores for the three categories produces the overall grade for each governor.

Measurement Caveats

This report uses statistical data to measure the fiscal performance of the nation’s governors from a small-government perspective, but the results include imprecisions. One issue is that the results cannot fully isolate the policy effects of governors from state legislatures. To help separate the effects, variables 1 and 3 measure each governor’s proposed—although not necessarily enacted—policies.

Another issue is that states grant governors differing amounts of authority over budgets. Most governors can use a line-item veto to trim spending, but some governors do not have that power. Also, supermajority voting requirements to override vetoes vary among the states. Such factors give governors differing levels of budget control.

Nonetheless, the results presented here should roughly reflect each governor’s fiscal approach. Governors who received the highest grades focused on reducing tax burdens and restraining spending, whereas governors who received the lowest grades pursued government expansion.

Appendix B: Fiscal Notes on the Governors

This section discusses the fiscal records of the 48 governors covered in the report. The profiles are based on the tax and spending data used to grade the governors and other information that sheds light on each governor’s fiscal approach. Spending data are for fiscal years and are generally from NASBO.43 The grades are calculated based on each governor’s record since 2022, or since 2023 if that was the governor’s first year in office. Finally, note that states typically refer to legislation as HB for House Bill and SB for Senate Bill, along with the bill number, such as SB 549 signed by Arkansas Governor Sarah Huckabee Sanders in 2023.

Alabama — Illinois

Alabama

Kay Ivey, Republican

Legislature: Republican

Grade: C

Took office: April 2017

Kay Ivey has years of service in Alabama government. She was a reading clerk in the legislature, an assistant director of the Alabama Development Office, the state treasurer, and the lieutenant governor. She was sworn in as governor in 2017 after the resignation of the prior governor in a scandal.

Ivey has delivered a series of modest tax cuts but has not taken on major tax reforms aimed at simplifying the code and reducing overall rates. In 2022, she approved an increase to the income tax standard deduction, a partial exemption of retirement income, and a trimming of small business taxes.

In 2023, Ivey signed a cut in the sales tax on food from 4 percent to 3 percent, which saved consumers about $150 million a year. She also signed a temporary exemption from tax for worker hours over 40 hours a week, and she approved one-time rebates totaling about $390 million.

In 2024, Ivey signed legislation creating education savings accounts for families to pay for private school tuition and other qualified education expenses. The state will fund the ESAs at up to $7,000 a year, and all Alabama families will be eligible by 2027.

Arizona

Katie Hobbs, Democrat

Legislature: Republican

Grade: D

Took office: January 2023

Katie Hobbs had a career as a social worker and rose to the position of chief compliance officer at the Sojourner Center, a domestic violence shelter. Hobbs also served in the state legislature for four terms and was elected Arizona’s secretary of state in 2018.

Hobbs was elected governor in 2022 after major tax reforms under prior governor Doug Ducey. Arizona’s multirate individual income tax structure was simplified and cut to a 2.5 percent flat tax effective in 2023. Also, voters approved a constitutional amendment in November 2022 that requires a 60 percent supermajority vote to pass ballot measures for higher taxes.

Hobbs has not made major tax changes. In 2023, she vetoed a bill that would have ended local taxes on groceries. She did, however, agree with the legislature on a one-time rebate for families of $250 per child.

Arkansas

Sarah Huckabee Sanders, Republican

Legislature: Republican

Grade: A

Took office: January 2023

Sarah Huckabee Sanders served as President Donald Trump’s press secretary before being elected governor in 2022. Before working in the White House, Sanders worked for US senators, governors, and presidential campaigns. She is the daughter of former Arkansas governor Mike Huckabee.

Like her predecessor in the governor’s mansion, Asa Hutchinson, Sanders is a tax reformer. Hutchinson reduced the top individual income tax rate from 6.9 percent to 4.9 percent in a series of laws. In early 2023, Sanders signed SB 549, which cut the top individual tax rate further to 4.7 percent, and later that year she signed SB 8, which cut the rate to 4.4 percent for 2024.

Hutchinson reduced the corporate tax rate from 6.5 percent to 5.3 percent. In early 2023, Sanders cut the rate to 5.1 percent, and later in the year reduced the rate to 4.8 percent for 2024. Sanders also cut unemployment taxes on businesses and approved one-time tax rebates.

In her 2024 state of the state address, Sanders said, “I’m committed to responsibly phasing out our state income tax rate and letting everyone keep more of their hard-earned money.”44 Neighboring Texas and Tennessee do not have individual income taxes, so Sanders is right that Arkansas does not need one either. In June 2024, she signed HB 1001, which cut the individual income tax rate to 3.9 percent and the corporate tax rate to 4.3 percent.

Despite all the tax cuts, Arkansas has a large rainy day fund measuring 41 percent of general fund expenditures in 2024, compared to the 50-state average of 12 percent.45 The key to responsible budgeting is spending restraint. In her state of the state address, Sanders said, “I made a promise to the people of Arkansas that we would work to slow the out-of-control growth of government. With the help of my Cabinet, we kept it.”46

Within modest state budget increases, Sanders signed into law major school-choice reform in 2023. The program sets up education savings accounts funded at 90 percent of the state’s per pupil funding of public schools. The accounts can be used for private school tuition and other qualified education expenses and will be available to all families when it is fully phased in.

California

Gavin Newsom, Democrat

Legislature: Democratic

Grade: D

Took office: January 2019

Gavin Newsom is a former lieutenant governor of California and mayor of San Francisco. He oversaw a large expansion in the general fund budget during his first few years in office that was fueled by rising income and capital gains taxes. During his first five years, the general fund budget expanded by 65 percent, from $140 billion in 2019 to $231 billion in 2024.

However, California now faces large deficits because spending keeps rising and income and capital gains tax revenues are lower than expected. In early 2024, the deficit was projected at $58 billion, but it was later closed as the governor and legislature slowed spending, pulled money from the rainy day fund, and raised corporate taxes.47

High taxes, high regulations, and high living costs are inducing people to leave California. IRS data show that the state lost a net 142,000 households to other states in 2022.48 The state loses two households with annual earnings above $200,000 for each one it gains. The Los Angeles Times reported, “With the top 20% of earners—those families making at least $120,000 a year—supplying 91% of the state income tax, a continued exodus is sure to lighten the Sacramento pocketbook. The state currently is facing a budget deficit of tens of billions of dollars.”49

Newsom’s high-tax policies are contributing to the exodus. In 2019, he approved business tax hikes of more than $1 billion. In 2020, he approved more business tax increases, including limiting the use of tax credits and loss deductions for three years. He also endorsed a massive $12 billion-a-year property tax hike on the November 2020 ballot, but the hike was defeated by voters.

Newsom took the taxpayers’ side on Proposition 30 on the November 2022 ballot. The proposition would have imposed a 1.75 percent surtax on high earners to fund various green programs, but it was voted down by the public. The ongoing threat of tax hikes on businesses and high earners generates an anti-investment climate for the state.

With a large budget surplus in 2022, Newsom approved legislation providing one-time rebates for moderate-income families. However, he also approved a large tax hike on wages with SB 951, which increased payroll taxes to fund the state disability insurance program. The hike will raise at least $3 billion annually and increase the state’s top individual income tax rate from 13.3 percent to 14.4 percent.50

In 2024, with a large budget gap opening, Newsom pushed for tax increases. He proposed temporarily limiting the use of net operating loss deductions and business tax credits. The budget agreement reached in June raised corporate tax revenues by $15 billion over the next three years.51 Newsom and the legislature have also raised taxes on managed care health organizations.

Another threat to Californian families is high energy prices caused by taxes and regulations. The state’s cap-and-trade system raises billions of dollars a year for the government from auctions of carbon permits, and the regulatory agency in charge has been considering raising billions of dollars more in coming years.52 Meanwhile, Newsom complains about gasoline “price gouging” and has pushed to raise taxes on California refineries.53

California has many natural advantages but they are being outweighed by anti-growth policies and people and businesses are leaving. California has the third-worst business tax climate among the 50 states, according to the Tax Foundation.54 It is also the third-least free state, according to Cato Institute rankings.55 California needs spending cuts, tax-rate cuts, and regulatory reforms, but residents will have to wait for a new governor.

Colorado

Jared Polis, Democrat

Legislature: Democratic

Grade: B

Took office: January 2019

Jared Polis is a former member of the US House of Representatives. He is a political moderate and scores quite well on spending in this report, although he has supported numerous tax hikes over the years.

Tax policy in Colorado revolves around the ballot box and the Taxpayer Bill of Rights (TABOR), which includes a mechanism to distribute surplus revenues back to taxpayers. In 2019, Polis supported retaining surplus revenues to boost spending, but voters rejected that idea at the ballot box in Proposition CC that year.56 However, Polis has supported TABOR refunds in other years.

Polis supported Proposition 116 in November 2020, which reduced the individual and corporate income tax rates from 4.63 percent to 4.55 percent. Voters approved the measure, which cut taxes by $150 million a year, by a 58 to 42 percent margin. Polis says that he supports reforming the income tax code by eliminating loopholes and reducing tax rates. In fact, he has said the income tax rate “should be zero.”57

On the other hand, Polis has supported some tax hikes. In 2020, he approved HB 1420, which temporarily increased business taxes. He also supported Proposition EE on the November 2020 ballot to increase taxes on tobacco, which was approved by voters. The increase raised more than $170 million a year.

In 2021, Polis signed legislation expanding the sales tax base to cover digital goods. And he signed legislation curtailing tax deductions, including itemized deductions for high earners and the pass-through deduction for business owners. He also signed SB 260 that year, which hiked transportation charges to raise more than $200 million a year. The bill provoked opposition for skirting voter-approval requirements under TABOR.

Also in 2021, Polis approved HB 1312, which raised the state’s exemption level for business personal property taxes in the state, which is a pro-investment reform for small businesses. He also exempted Social Security benefits from taxation.

In 2022, Polis supported TABOR-funded rebates of $750 for individuals and $1,500 for married couples. On the November ballot that year, Coloradans voted for Proposition 121 to cut the individual and corporate tax rates from 4.55 percent to 4.40 percent. Polis endorsed the measure, which passed by a 65 to 35 percent margin.58

In 2023, Polis supported Proposition HH, which would have cut property taxes, but also would have reduced taxpayer rebates under TABOR.59 Voters rejected the plan. Polis signed into law expansions in low-income credits and various special-interest credits, such as for film production.

In his 2024 state of the state speech, Polis said, “A healthy TABOR surplus is the sign of a strong economy, but also a signal that the tax rate is too high. Tax relief is the best mechanism to relieve cost of living pressures and spur economic growth for everyone in our state … Cutting the income tax rate is the most effective way to further our economic growth.” He continued, “Taxes are simply too high: income taxes, property taxes, and the state sales tax,” and he promised to work “on a bold, balanced, progressive package, including cutting the income tax rate.”60

In 2024, Polis signed SB 228, which changed the TABOR mechanism to reduce income tax rates but not how much revenues are refunded overall.61 The bill cut the individual and corporate income tax rate from 4.4 percent to 4.25 percent for one year, and in future years TABOR refunds will be applied to income tax and sales tax cuts depending on the level of excess revenues.

Polis also signed HB 1311 in 2024, which created a refundable Family Affordability Tax Credit benefiting low-income families by more than $300 million a year. However, the new credit will reduce the amount of revenues available for refunding under TABOR, and so taxpayers as a whole will be no further ahead.62

Polis also signed SB 233, which limits annual property tax revenue increases, creates an exemption amount for residential properties, and limits assessment rates for residential and nonresidential properties.

Finally, in 2024, Polis signed SB 230, which imposed a new fee on the oil and gas industry to raise $138 million a year mainly to fund public transit.63

Connecticut

Ned Lamont, Democrat

Legislature: Democratic

Grade: C

Took office: January 2019

Ned Lamont is a former cable television executive. He has scored poorly on previous Cato report cards and scores middling on this one.

In 2019, Lamont signed into law a paid leave program that imposed a wage tax on employers to raise more than $400 million a year. He approved other tax increases that year, including extending a corporate income tax surcharge and broadening the sales tax base. In 2021, Lamont approved an extension of the corporate tax surcharge and a delay of a phaseout of a corporate capital tax.

However, budget surpluses in 2022 prompted Lamont to change course. He approved one-time tax rebates for some families, a temporary suspension of the gas tax, an expansion of the earned income tax credit, and a reduction of taxes on retirement income.

In 2023, Lamont approved an individual income tax cut, which reduced the rates for lower- and middle-income households to save about $370 million annually. The bill cut the 3 percent rate to 2 percent and the 5 percent rate to 4.5 percent, but it did not reduce the top rate of 6.99 percent.

The savings from the individual tax cut were partly offset by extending the 10 percent corporate tax surcharge for another three years.64 In March 2023, Lamont said, “The temporary surcharge has been temporary for about 20 years … I think probably [it’s time to] let that go back to 7.5 percent,” but then in June he approved another extension.65

That was a bad policy decision, as Connecticut’s business tax climate is ranked the fourth-worst in the nation by the Tax Foundation.66 The state has a high corporate tax rate and a punitive property tax burden on businesses.

Delaware

John Carney, Democrat

Legislature: Democratic

Grade: F

Took office: January 2017

John Carney has had a long political career. Before becoming Delaware governor, he was a member of Congress, Delaware’s lieutenant governor, and Delaware’s secretary of finance. He also served on the staff of Joe Biden in the US Senate.

On the 2018 Cato fiscal report, Carney earned a D because he supported tax increases, including increases on corporations, alcohol, and cigarettes. Carney improved to a C on the 2020 Cato report but then dropped back down to a D on the 2022 report.

Large spending increases pulled down Carney’s score in this report. Delaware’s general fund spending has exploded by 42 percent under Carney—from $4.27 billion in 2019 to his proposed $6.08 billion in 2025.67 Spending rose 9.9 percent in 2024 and a proposed 8.4 percent in 2025.

On tax policy, he has supported both hikes and cuts. In 2022, he approved one-time rebate checks of $300 to eligible residents. But he also signed into law SB 1, an expensive family leave program that imposes an 0.8 percent payroll tax on employers and employees to fund paid parental and medical leave benefits.

In 2023, Delaware legalized recreational marijuana and imposed a 15 percent excise tax on it. Carney objected to the legislation but allowed it to become law without his signature.68 Carney proposed increasing standard deductions under the income tax and increasing the earned income tax credit.

Carney has called for an amendment to the state constitution to smooth out state spending from year to year. The state would establish a benchmark level of spending, and in boom years extra revenues would be deposited in a budget stabilization fund, which would be a larger version of the current rainy day fund.

Florida

Ron DeSantis, Republican

Legislature: Republican

Grade: C

Took office: January 2019

Ron DeSantis served in the US House of Representatives from 2013 to 2018 before being elected governor. Florida is the second-freest state according to Cato’s ranking.69 It is a low-tax state with no individual income tax, and DeSantis has supported this important policy advantage.

DeSantis approved a temporary reduction in the corporate tax rate and a bill to avoid business tax increases related to the federal Tax Cuts and Jobs Act. DeSantis has frequently signed legislation providing temporary tax breaks, including annual sales tax holidays, rebates, a suspension of the gas tax, and similar sorts of breaks. Using budget surpluses for temporary tax breaks has reduced funds available for spending, but it would have been better to enact permanent tax reforms.

DeSantis has signed some permanent reforms. In 2023, he cut the sales tax on commercial leases from 5.5 percent to 4.5 percent, and then cut it to 2 percent in 2024. The reform will save Florida businesses more than $1 billion a year.70 DeSantis has proposed doubling the maximum sales tax collection allowance to save retailers $165 million a year.71

DeSantis scores above average on spending. He has proposed lean budgets, although the legislature has usually passed higher spending. He does not shy away from vetoing spending. DeSantis vetoed $1 billion from the 2025 budget, saying “Governments should strive to do more with less.… It can be done, and my action today cements that lesson for the nation.”72

In his 2024 state of the state address, DeSantis discussed his fiscal approach: “Florida has the lowest number of state employees per capita at 96 per 10,000 (82 full time), and the lowest cost per state resident at $40. This year, my budget proposal reduces the budget by $4 billion from the previous year, placing $16.3 billion in reserves and paying down another $455 million in state debt ahead of schedule.”73

Georgia

Brian Kemp, Republican

Legislature: Republican

Grade: B

Took office: January 2019

Brian Kemp is an entrepreneur who has invested in agriculture, banking, manufacturing, and real estate. He was a state senator from 2003 to 2007 and Georgia’s secretary of state from 2010 to 2018. Kemp performs well on this report and on previous Cato fiscal reports.

Kemp has approved major tax reforms. He signed HB 1437 in 2022, which transitioned Georgia from a multirate individual income tax to a single-rate flat tax. The bill collapsed six tax brackets with a top rate of 5.75 percent to a flat tax of 5.49 percent in 2024. If revenue targets are met, the tax rate will drop to 4.99 percent by 2029. The bill also increased personal exemptions. The reforms saved taxpayers $450 million in the first year and increasing amounts after that.

In 2024, Kemp and the legislature accelerated the planned income tax cuts. HB 1015 cut the individual income tax rate to 5.39 percent for 2024 and scheduled a reduction to 4.99 percent by 2028. Meanwhile, HB 1023 cut the corporate rate from 5.75 percent to 5.39 percent, and then matched the individual rate reductions for future years.

In 2022, Kemp temporarily suspended the gas tax, reduced taxes on military retirement income, and provided one-time tax rebates. In 2023, he provided additional rebates, and in 2024, he increased the dependent exemption under the income tax.

Georgia has enjoyed large budget surpluses, which have allowed both tax cuts and budget increases in recent years.74 To soak up the surplus cash, Kemp proposed expanding the state’s rainy day fund, but the reform did not pass the legislature.

In his 2024 state of the state address, Kemp noted, “One of the brilliant principles of America’s founding is the role of the states, for them to be the laboratories of democracy, to protect the liberties and freedoms of their citizens, and to carry out the will of the people.… In Georgia, we balance our budget and spend less than we take in. We cut taxes instead of raising them. We return money back to the taxpayers rather than justifying new government programs.”75

Hawaii

Josh Green, Democrat

Legislature: Democratic

Grade: B

Took office: December 2022

Josh Green grew up in Pittsburgh, became a doctor, and moved to Hawaii to practice medicine. Green served in the state legislature for more than a decade and served as lieutenant governor.

In 2023, Green approved tax increases on cigarette dealers, e‑cigarettes, and e‑liquids. He also signed legislation increasing low-income tax credits. In February 2024, Green proposed increasing cigarette taxes from $3.20 to $3.60 per pack, raising the conveyance tax on sales of luxury homes, and imposing a new tax on hotels and vacation rentals.76

However, Green also proposed cutting income taxes by raising tax bracket thresholds and indexing brackets for inflation. In his 2024 state of the state address he said, “We will also index the state’s tax code to provide all taxpayers relief from inflation—a long overdue change which will help people in every tax bracket.”77

The legislature followed through with HB 2404, which included even larger income tax cuts than Green had proposed. The governor signed the bill, which doubled standard deductions and will cut taxes in future years by adjusting income tax brackets. If the reductions proceed as planned, the average effective tax rates on middle-income earners will be cut roughly in half by 2031, with larger cuts at the bottom and smaller cuts at the top.78

This was a large tax cut, particularly in a state that rarely cuts taxes. However, the law did not reduce Hawaii’s high top tax rate of 11 percent. Nonetheless, taxpayers will save more than $3 billion over the first five years, which is one of the largest state tax cuts relative to total tax revenues among the states in recent years.79

Green has held the general fund budget quite flat and has been willing to trim excess spending passed by the legislature.80 For these reasons, Green is the highest-scoring Democrat in this study.

Idaho

Brad Little, Republican

Legislature: Republican

Grade: B

Took office: January 2019

Brad Little had a career in ranching, and he served as a state senator and as Idaho’s lieutenant governor. As governor, Little has been a leader in tax reform, which is helping Idaho become a magnet for inflows of investment and workers from other states.

In 2021, Little signed HB 380, which cut the top individual income tax rate from 6.93 percent to 6.5 percent and reduced the number of tax brackets from seven to five. The bill also cut the corporate tax rate from 6.93 percent to 6.5 percent. That was followed by HB 436 in early 2022, which cut the top individual tax rate to 6.0 percent and reduced the number of tax brackets to four. The bill also cut the corporate tax rate to 6.0 percent. The cuts are saving taxpayers more than $400 million a year.

Little called for further tax cuts, and later in 2022 the legislature passed HB 1, which converted the individual income tax into a 5.8 percent flat tax and also cut the corporate tax rate to 5.8 percent. The legislation also nullified a tax-increase initiative that was to have appeared on the November ballot.

In 2024, Little approved further reductions of individual and corporate income tax rates. HB 521 trimmed the rates from 5.8 percent to 5.695 percent. Little also signed HB 428, which cut unemployment insurance taxes by 20 percent, saving businesses more than $40 million a year.

Despite all the tax cuts, Idaho has one of the largest rainy day funds among the states. In 2024, Idaho’s fund was 23 percent of its annual expenditures, almost double the 50-state average of 12 percent.81

Idaho has improved its ranking on fiscal freedom on Cato’s Freedom in the 50 States report in recent decades.82 The report also ranks Idaho as one of the best states for regulatory freedom. Little claims that Idaho is the “least regulated state in the nation.”83 Americans are recognizing these advantages, and Idaho is the state with the highest ratio of in-migration to out-migration.84

Illinois

J. B. Pritzker, Democrat

Legislature: Democratic

Grade: C

Took office: January 2019

Billionaire J. B. Pritzker is a member of the family that owns the Hyatt hotel chain, and he has long been involved in Democratic politics. Governor Pritzker scored poorly on past Cato fiscal reports because of his huge tax increases but he was more restrained on tax and spending increases for the period of this report.

In 2019, Pritzker approved $2.7 billion in net annual tax increases. He increased the gas tax from 19 cents to 38 cents per gallon, hiked vehicle registration fees, and increased the cigarette tax from $1.98 to $2.98 per pack.

In 2020, Pritzker pushed for passage of a ballot question to amend the state constitution and convert the state’s flat individual income tax to a multirate system. If the amendment had passed, legislation would have converted the 4.95 percent tax to one with a top rate of 7.99 percent. The plan also would have hiked the corporate income tax rate and raised taxes by $3.9 billion a year. The public rejected the hike at the ballot box. Despite that rebuke, Pritzker approved numerous tax increases in 2021, including broadening the corporate tax base and halting a corporate franchise tax phaseout.

Pritzker seems unconcerned that Illinois is losing workers, entrepreneurs, and retirees, who are fleeing to warmer and lower-tax states. IRS data show that Illinois has the worst ratio of in-migration to out-migration of any state except New York. Illinois loses more than two households earning more than $200,000 per year for each one moving in.85 To reverse the migration outflow, the state needs to reduce taxes and embrace leaner government.

In 2022 the pain of high inflation finally prompted the governor to give taxpayers a break. He approved a one-year suspension of the grocery sales tax, delayed an increase in the gas tax, provided one-time rebates to low-income residents, and expanded the earned income tax credit.

Unfortunately, tax increases were back on the agenda in 2023 and 2024. In 2023, the budget modified the inflation indexing of the personal exemption under the income tax, which cost taxpayers about $100 million.86 In 2024, the budget included about $1 billion in tax increases, including a sports wagering tax, limits on business net operating loss deductions, limits on retailer payments for collecting sales taxes, and various other charges.87 While the budget eliminated a 1 percent statewide sales tax on groceries, it allowed local governments to continue imposing their own sales taxes on groceries.88

While Pritzker favors higher taxes on businesses in general, he hands out narrow breaks to big corporations. In 2023, for example, he awarded $213 million of incentives to a Chinese battery maker that is building a facility in Illinois. Because “the company is making a minimum investment of at least $1.5 billion, it’s also eligible for exemptions from state and local sales tax on building materials, utility tax, and telecommunication excise tax.”89 This sort of favoritism for large corporations is both unfair and distorts the economy.

In his 2024 state of the state address, Pritzker bragged that he and legislators had “created a $2 billion Rainy Day Fund.”90 That figure is correct, but compared to state spending it is the second smallest rainy day fund in the nation.91 Illinois also has the highest level of unfunded pension obligations of any state, as shown in Table 2.

Indiana — Montana

Indiana

Eric Holcomb, Republican

Legislature: Republican

Grade: C

Took office: January 2017

Eric Holcomb entered the Indiana governor’s office in 2017 after a career in the US Navy and other positions in public service. He has supported substantial tax cuts. In 2022, he signed legislation eliminating the state’s tax on utility services such as gas and water, which will save consumers about $220 million a year. Also, with large budget surpluses that year, Holcomb approved two rounds of taxpayer rebates, which disbursed excess cash from the state treasury back to taxpayers before it could be spent on expanded programs.

More importantly, Holcomb signed HB 1002 that year, which cut the individual income tax rate from 3.23 percent to 3.15 percent in 2023 and reduced it to 3.05 percent in 2024. The law scheduled further reductions over time to 2.9 percent if budget conditions are met. In 2023, Holcomb approved HB 1001, which accelerated the tax rate cuts and removed the need for cuts to meet budget conditions.

Iowa

Kim Reynolds, Republican

Legislature: Republican

Grade: A

Took office: May 2017

Kim Reynolds has had a long career in public service as a county treasurer, a state senator, and lieutenant governor of Iowa. She became governor after her predecessor stepped down in 2017, and then she won election in 2018. Reynolds has overseen lean budgets and been a champion tax reformer, earning her the highest score on Cato’s 2022 and 2024 reports.

In 2018, Reynolds cut the top individual income tax rate from 8.98 percent to 8.53 percent and the top corporate tax rate from 12 percent to 9.8 percent. In 2021, she resumed her tax-reform drive, signing bills to speed up the phase-in of income tax cuts and eliminating Iowa’s inheritance tax.

In 2022, Reynolds approved HF 2317, which phased in tax cuts to save Iowa taxpayers more than $1 billion a year by 2026. The law consolidated individual income tax rates into a single-rate structure and phased down the rate to just 3.9 percent by 2026. The top individual rate is 5.7 percent in 2024. Taxes on pensions and other retirement benefits were repealed.92

The 2022 legislation also phased down the corporate tax rate from 9.8 percent to 5.5 percent if revenue targets are met. In her budget that year, Reynolds noted, “Corporate tax levels directly affect economic activity in states, and those with more competitive structures and rates are in much better positions to grow existing businesses and attract new ones.”93 The corporate tax rate in 2024 is 7.1 percent. To further ease business burdens, Reynolds has supported cuts to unemployment insurance taxes.94

In 2024, Reynolds called for speeding up the income tax cuts, and the legislature delivered. She signed SF 2442, which replaces Iowa’s individual income tax brackets with a 3.8 percent flat tax effective in 2025. That will be a remarkable improvement from the nine-bracket system and the top rate of 8.98 percent that Reynolds faced when she entered office.

Reynolds has suggested that Iowa is on the path to zeroing out the individual income tax, and most Iowans support that goal. A March 2024 poll found that Iowans, by a 62 percent to 32 percent margin, favor getting rid of the income tax.95

Reynolds has been a lean budgeter. Iowa general fund spending has grown at just 2.3 percent annually since she entered office in 2017. Within those lean budgets, Reynolds has fit major education reforms. In 2023, she approved legislation creating education savings accounts, which parents can use to pay for private school tuition and other qualified education expenses. Universal eligibility for the accounts is being phased in. The reforms should save taxpayer money since Iowa’s per pupil ESA funding is just half the per pupil costs for students in public schools.96

Kansas

Laura Kelly, Democrat

Legislature: Republican

Grade: B

Took office: January 2019

Laura Kelly served as the executive director of the Kansas Recreation and Park Association and has worked in mental health services. She also served in the Kansas legislature and was the ranking member on the Ways and Means Committee.

The governor has supported substantial spending increases. The general fund budget has grown from $7.0 billion in 2019 to $9.9 billion in 2024, which is an annual average increase of 7.1 percent.

Kelly has agreed to substantial tax cuts but has blocked some larger tax reforms passed by the legislature. In 2022, she called for eliminating the sales tax on groceries, and the legislature followed through. She signed HB 2106, which phases down the 6.5 percent grocery tax to zero by 2025 to save Kansas households more than $400 million annually.

In 2022, Kelly signed legislation reducing the corporate tax rate from 7.0 to 6.5 percent, paired with a package of corporate subsidies and narrow incentives. The lower rate became effective in 2024.

In 2023 and 2024, Kelly proposed various tax reductions, including rebates, property tax relief, an increase in the standard deduction, accelerating the cuts on groceries, ending taxes on Social Security benefits, and reducing a bank privilege tax.97 However, Republicans in the legislature had other plans for tax reform, and there was a stand-off on priorities.

In January 2024, Kelly vetoed a bill to convert the state’s multirate individual income tax with a top rate of 5.7 percent to a 5.25 percent flat tax. In April and May, Kelly vetoed two more attempts at tax reform, which would have cut the top income tax rate, increased standard deductions, and exempted Social Security benefits from income taxes.98

Finally, in June 2024, Kelly signed SB 1, which cut individual income taxes by about $340 million a year.99 The state’s three-rate structure—3.1 percent, 5.25 percent, and 5.7 percent—was collapsed to two rates: 5.2 percent and 5.58 percent. Standard deductions and personal exemptions were increased. Taxes on Social Security benefits were repealed. The tax package also included a reduction in statewide property taxes.

Kentucky

Andy Beshear, Democrat

Legislature: Republican

Grade: D

Took office: December 2019

Andy Beshear served as Kentucky attorney general before being elected governor. He is the son of former Kentucky governor Steve Beshear. The current governor Beshear scores poorly on spending and taxes. He has allowed the budget to grow quickly, including a proposed 21 percent general fund spending increase for 2025.

Beshear proposed modest tax reductions in 2022, including freezing vehicle property tax rates and reducing the sales tax rate for a year. But he vetoed HB 8 and was overridden. It cut the individual income tax rate from 5 percent to 4.5 percent. To partly offset the revenue loss, the law expanded the sales tax base. Overall, the bill saved taxpayers about $460 million in the first year.

In vetoing the tax-rate cut, Beshear worried that it would jeopardize corporate welfare handouts: “House Bill 8 will leave the Commonwealth unable to comply with its promise to provide incentives to some employers under the Kentucky Business Incentives Program. In total, House Bill 8 will negatively impact over 207 economic development projects that have received more than $413,000,000 in incentives.”100 Essentially, Beshear prioritized handouts to selected corporations over simpler tax-rate cuts to encourage all businesses to invest.

Beshear changed direction in 2023 and reluctantly approved tax reforms. He signed HB 1, which affirmed the income tax reductions set in motion by the 2022 law and cut the individual income tax rate to 4.0 percent in 2024. That decision made political sense because if Beshear had vetoed, the legislature would have likely overridden his veto, and he “is running for reelection this year in what is expected to be a competitive race.”101 Whatever his motivation for approving the bill, Kentucky taxpayers and the economy are better off for it.

Maine

Janet Mills, Democrat

Legislature: Democratic

Grade: F

Took office: January 2019

Janet Mills served as a criminal prosecutor, district attorney, member of the state legislature, and state attorney general before running for governor in 2018. Her predecessor in office, Paul LePage, earned an A every time he was graded on the Cato fiscal report.

Mills scored poorly on spending, as she usually proposes large budget increases. The general fund budget jumped from $4.1 billion in 2022 to $5.1 billion in 2024. On her first day in office she approved the expansion of Medicaid, which LePage had resisted.

On tax policy, Mills approved one-time rebates for moderate-income households. She also approved expansions of a property tax credit, the earned income tax credit, a dependent credit, retirement income deductions, and a refundable tax credit for college debt. Unfortunately, the governor has focused on such narrow breaks rather than pursuing broad-based tax reforms.

In 2023 Mills signed LD 1964, which imposed a paid family leave program funded by a new 1 percent tax on wages. Mills claimed, “I have repeatedly said I am opposed to increasing taxes,” but she decided to sign the large tax hike nonetheless.102 The payroll tax will raise about $370 million a year.103

Mills is mistakenly trying to improve her state’s competitiveness with corporate subsidies. In pushing subsidies in 2023, Mill said, “If we want to keep Maine competitive with other states that are working aggressively to attract businesses, then we simply cannot be without a business incentive program.”104 But Maine has a high 8.9 percent corporate tax rate, high property taxes on businesses, and ranks 34th on the Tax Foundation’s business tax climate index.105 Policymakers should fix the basic tax climate, and then economic growth will take care of itself without any need for business subsidies.

In 2024, Mills switched gears and vetoed LD 1231, which would have added higher-income tax rate brackets at the top end while reducing rates at the bottom end. Mills noted that the state has already “substantially reduced, if not outright eliminated, the tax burden for low-income Mainers,” and that raising tax rates on the top 1 percent would increase revenue volatility.106 The overall bill was roughly revenue neutral.

Maryland

Wes Moore, Democrat

Legislature: Democratic

Grade: C

Took office: January 2023

Wes Moore was elected governor in 2022. Before entering politics, he was a second lieutenant in the US Army, a captain with the 82nd Airborne Division, a banker, and an adviser to political leaders. He has published books exploring issues of race and opportunity.

Moore approved a smattering of tax cuts in 2023, including a tax cut for military retirement income and expansions of the child tax credit and earned income tax credit. However, he also increased various fees and approved a 9 percent sales tax on marijuana.

In 2024, numerous bills were proposed in the legislature to raise taxes. Moore leaned against major tax increases but signed a budget that included about $340 million a year in higher vehicle registration fees, fees for ride sharing, fees on electric vehicles, taxes on vapes, and an increase in the cigarette tax of $1.25 per pack.107

Moore scored well on spending. After a huge spending increase under the last year of former governor Larry Hogan, the general fund budget has been flat for the first two years under Wes Moore.

Massachusetts

Maura Healey, Democrat

Legislature: Democratic

Grade: B

Took office: January 2023

Before being elected governor, Maura Healey was Massachusetts attorney general for two terms and also worked in private law practice. Healy’s tenure as governor follows Republican Charlie Baker, who scored poorly on earlier Cato fiscal reports for his tax and spending increases.

Healey entered office after voters approved a constitutional amendment in November 2022 allowing a huge tax increase on high earners. On Question 1, voters approved a 4 percent surtax on incomes above $1 million, which raised the top individual income tax rate from 5 percent to 9 percent. In the near term, the hike is expected to raise about $1.3 billion annually for new spending, but over time it will exacerbate the exodus of high earners from the state and undermine the state budget and economy.

Healy and the legislature are using the new revenues to increase spending and provide targeted tax breaks. In her 2024 state of the state address, Healey said, “We passed a billion-dollar tax cut that will save money for everyone in our state. That’s right, we cut taxes in Massachusetts for the first time in 20 years.”108

However, many of Healey’s tax cuts are special-interest giveaways, such as housing developer breaks, and some of her tax cuts are actually spending, such as an expansion of the refundable earned income tax credit.109 Nonetheless, Healey has approved a few pro-growth reforms, such as an increase in the estate tax threshold and a cut to the capital gains tax rate.

Healey undercut her tax-cutting message by supporting legislation to allow local governments to impose higher transfer taxes on property sales above a specified value. The tax increase would have raised about $400 million a year but was rejected by the legislature.

Healey’s modest tax breaks will not make up for the anti-growth effects of high individual and business taxes in Massachusetts. IRS data show that for every four taxpayers earning more than $200,000 leaving the state, only three are moving in.110 The tax rate increase that was passed in 2022 will exacerbate the exodus of high earners. At the same time, Massachusetts is unwelcoming to businesses—the Tax Foundation ranks the state 46th on its business tax climate because of its high corporate tax rate, high property taxes, and high unemployment insurance taxes.111

Michigan

Gretchen Whitmer, Democrat

Legislature: Democratic

Grade: D

Took office: January 2019

Gretchen Whitmer served in both the Michigan House and Senate before being elected governor in 2018. She scored fairly poorly on this report because of her support for tax increases and her vetoing of tax reforms passed by the legislature.

In a debate in 2018, Whitmer “scoffed at the idea” that she supported a gas tax increase, calling the accusation “ridiculous.”112 But then Whitmer pushed for a gas tax increase during her first year in office. Her plan would have increased gas taxes by $2 billion annually, but it did not pass. Whitmer approved an increase in online sales taxes, and she has proposed increasing taxes on passthrough businesses.

However, Whitmer has supported some tax cuts. In her 2022 state of the state address she called for tax reductions on retirement income.113 She also called for one-time rebates and an expansion in the earned income tax credit. However, Whitmer vetoed SB 768, which contained those and other tax cuts, which would have saved individuals and businesses $2 billion annually. The bill would have cut the corporate tax rate from 6 percent to 3.9 percent and the individual income tax rate from 4.25 percent to 3.9 percent.

In response to the veto, the legislature passed a compromise bill, HB 4568, but Whitmer vetoed that as well. It would have cut the individual income tax rate from 4.25 percent to 4.0 percent, expanded the earned income tax credit and personal exemption, and created a child tax credit. Whitmer also vetoed a temporary suspension of the gas tax. However, Whitmer agreed with a new legislature in 2023 to approve a reduction in taxes on retirement income and an expansion of the earned income tax credit.

In 2023, taxpayers enjoyed a one-year automatic cut in the individual income tax rate from 4.25 to 4.05 percent because of an existing law related to budget surpluses. Republicans in the legislature wanted to keep the lower rate permanently, but Whitmer did not. The Wall Street Journal editors noted that the governor found budget room for billions of dollars in corporate subsidies but no room for rate cuts that would benefit all taxpayers.114

In 2024, Whitmer proposed creating a research and development tax credit, a caregiver tax credit, and a one-time rebate for new vehicle purchases. The rebate would be $1,000 for gas-powered cars, $2,000 for electric vehicles, and an extra $500 for union-made cars. However, such a subsidy would do nothing to support long-term economic growth.

Minnesota

Tim Walz, Democratic-Farmer-Labor

Legislature: Democratic-Farmer-Labor

Grade: F

Took office: January 2019

Tim Walz is a former member of the US House of Representatives and served in the Army National Guard. He has overseen substantial spending increases and pushed many tax hikes. Minnesota’s general fund budget increased from $51.9 billion in the 2022–2023 biennium to $70.5 billion in the 2024–2025 biennium, a 36 percent increase.115

In 2019, Walz’s budget would have added “$2 billion more in new spending and taxes would increase by $1.3 billion to pay for it, with the rest of the money coming from an existing surplus.”116 But he compromised with the legislature, and the final tax increase was about $330 million annually. Walz also pushed for higher gas taxes and higher vehicle fees to raise about $1 billion annually for transportation, but those increases were rejected.

Walz pushed for more tax hikes in 2021. He proposed adding a new individual income tax rate of 10.85 percent above the current top rate of 9.85 percent, a surtax on capital gains and dividends, and a hike to the corporate tax rate from 9.8 percent to 11.25 percent. The proposals—which would have raised about $1.6 billion annually—were rejected by the legislature.

In 2022, Walz said, “Cutting taxes for the wealthiest amongst us will not guarantee opportunities in Minnesota for the wider variety of folks, and it certainly won’t grow our economy from the middle out.”117 But Minnesota’s high tax rates are undermining the economy and driving away wealthy people, who include highly skilled job-creating entrepreneurs. IRS data show that the state loses about 10 households earning more than $200,000 for every 6 that it gains.118

In 2023, Democrats took control of the legislature and Walz pushed ahead with permanent tax hikes on businesses and high earners, while handing out low-income credits and one-time rebates totaling about $1 billion.119 In signing HF 1938, Walz raised taxes on businesses with foreign income, reduced the standard deduction for high earners, and imposed a new tax on the investment income.

Walz hit the middle class with HF 2887, which raised taxes and fees on vehicles and transportation. The increases included indexing the gas tax for inflation, increasing vehicle registration taxes, raising fees on deliveries, and raising sales taxes in the Twin Cities area.120

The governor hit the middle class again in 2023 with a massive tax hike to pay for a new mandatory paid family leave program. The legislation imposed a 0.7 percent tax on wages beginning in 2026 to fund the program benefits, but then new legislation in 2024 increased the tax rate to 0.88 percent of wages. An accounting analysis of the plan found that the tax will raise $1.2 billion in the first year of operation and rising amounts after that.121