With America’s sluggish economy and stagnant wages, federal policymakers are looking for ways to help the working poor. One idea that has gained some bipartisan support is expanding the earned income tax credit (EITC). President Barack Obama, members of Congress, and presidential candidates have all proposed plans to expand the tax credit.1

The EITC is a huge program. In 2015 it will provide an estimated $69 billion in benefits to 28 million recipients.2 The EITC is the largest federal cash transfer program for low-income households. Benefits are available to households with earnings from employment.

While the EITC is administered through the tax code, it is primarily a spending program. The EITC is "refundable," meaning that individuals who pay no income taxes are nonetheless eligible to receive a payment from the U.S. Treasury. Of the $69 billion in benefits this year, about 88 percent, or $60 billion, is spending.

Articles by liberal and conservative pundits regarding the EITC often make it seem as if there are few downsides to the program. The EITC is aimed at reducing poverty and encouraging work. Who could be against that?

Alas, there is no free lunch with subsidy programs. The EITC has a high error and fraud rate, and for most recipients it creates a disincentive to increase earnings.3 Also, the refundable part of the EITC imposes a $60 billion cost on other taxpayers, reducing their incentives to work, invest, and pursue other productive activities.

We conclude that the costs of the EITC are likely higher than the benefits. As such, the program should be cut, not expanded. Policymakers could better aid low-income workers by removing government barriers to investment, job creation, and entrepreneurship.

Low-Income Households

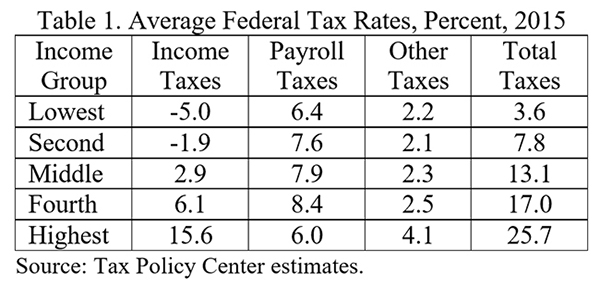

The federal tax system is highly graduated. Lower-income households pay much smaller shares of their incomes toward taxes than do higher-income households. Table 1 shows estimates of average federal tax rates for U.S. households in five income groups.4 These tax rates are simply taxes paid divided by income. The average household in the highest group paid 25.7 percent of its income toward taxes in 2015, while the average household in the lowest group paid 3.6 percent.

Looking at income taxes, households in the bottom two groups have an overall negative tax rate. That is because many low-income households pay no income tax but receive payments from the refundable EITC and other refundable credits. This year, an estimated 45 percent of households will pay no federal income tax.5

The expansion of the EITC and other low-income benefits in recent decades has reduced the share of U.S. households that pay income tax. The Congressional Budget Office found that the average total federal tax rate for the bottom one-fifth of households fell from 8.4 percent in 1990 to just 1.9 percent by 2011.6

Growth of the EITC

In the early 1970s, policymakers considered ways to combat the anti-work effects of the growing welfare state. But rather than reining in the welfare state, they decided to expand it in 1975 by enacting the EITC. The credit was aimed at reviving work incentives and offsetting rising federal payroll taxes. It began as a temporary program, but Congress made it permanent in 1978. Initially, it was a 10-percent wage credit with a maximum value of $400, and only people with children were eligible.

Congress expanded the size and scope of the EITC in numerous laws over the decades. The EITC is a much larger program today than in 1975. It has credit rates up to 45 percent and a maximum credit of $6,242 in 2015.7 It also provides benefits to childless workers.

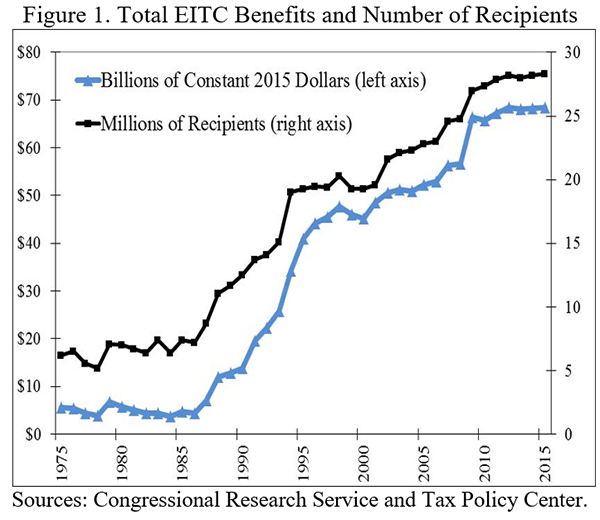

Figure 1 shows the growth of the EITC. The number of recipients and cost was relatively stable for the first decade, but expansions in 1986, 1990, 1993, and 2009 greatly increased the costs. The number of recipients soared from 12.5 million in 1990 to 28 million by 2015. Total EITC benefits in constant 2015 dollars increased from $14 billion in 1990, to $45 billion in 2000, and to an estimated $69 billion by 2015.8

As noted, most of the benefits stem from the EITC's refundable feature, meaning that families who owe no income taxes nonetheless receive a cash payment. The EITC has increasingly become a spending program over time. The refundable portion of benefits has risen from 70 percent in 1990 to about 88 percent today.9

Structure of the EITC

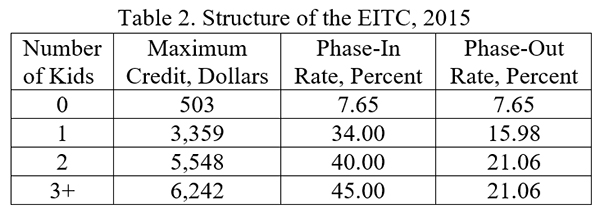

EITC benefits vary based on the number of children, income level, and filing status (single or married). Table 2 shows the maximum credit for households with different numbers of children.

The table also shows the phase-in and phase-out rates, which determine the amount of the credit as income varies. Initially, the credit rises with income (the phase-in range). Then the credit reaches the maximum amount and is constant for a certain range (the flat range). Finally, the credit falls as income rises further (the phase-out range).

For example, during the phase-out range for a single parent with two children, the phase-out rate is 21.06 percent. Thus, for every additional $1,000 the parent earns, she loses $210 in EITC benefits.

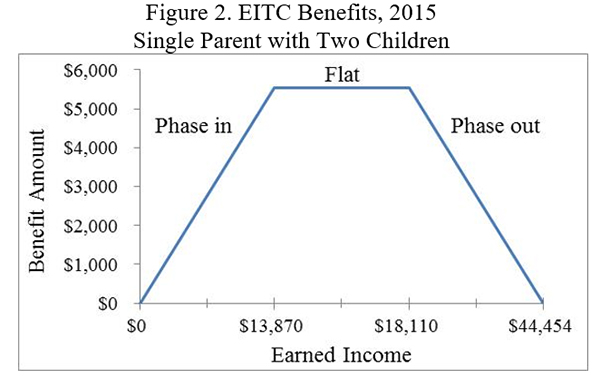

Figure 2 shows the EITC benefit structure for such a household. The maximum credit of $5,548 would be available for those earning between $13,870 and $18,110, and the credit would be fully eliminated if earnings topped $44,454. The pattern of benefits—rising, flat, then falling—is similar for other types of families.

EITC Reduces Market Wages

A key goal of the EITC is to strengthen work incentives for lower-income individuals. If the EITC is successful, it will increase the labor supply of low earners. On a simple supply-and-demand diagram, the labor supply curve would shift to the right, and that would tend to reduce market wages.10

As labor supply increases and market wages fall, it induces employers to hire additional workers. Workers who receive the EITC are better off than before with the combination of a lower market wage and the EITC. But it is interesting that proponents of the EITC implicitly favor cutting market wages for low earners.

One side effect of the EITC is that, to the extent it works by pushing down market wages, it ends up hurting low earners who receive no EITC or a small EITC—mainly childless workers. The labor-supply effect of the EITC also means that the program acts partly as a subsidy to businesses that hire lower-skilled workers because they are able to pay reduced market wages.11

Work Incentives and Disincentives

The EITC affects work incentives in two ways. First, it affects labor force participation, or the incentive for non-workers to gain employment. Second, it affects the number of hours worked by people who are working. The EITC affects these factors in different ways for different people, creating both positive and negative effects.12

Let's examine labor force participation first. People within the EITC's income range have an added incentive to find a job because the credit increases the reward for working. Most economists think that the EITC particularly encourages low-income single mothers to join the labor force, and there is solid empirical support for that positive effect.13

However, there is doubt about the strength of this effect.14 Supporters of the EITC often point to the strong gains in participation of single mothers in the late 1990s as evidence of the EITC's benefits. But while the number of EITC recipients soared between 1987 and 1994, the number was flat in the late 1990s, as shown in Figure 1. Yet the years from 1994 forward were precisely the years that labor force participation by single mothers was growing strongly.15 That suggests other factors caused much of the participation increase in the late 1990s—perhaps the strong economy at the time and welfare reforms that increased work requirements. Note that with the weaker economy after 2000, the participation of single mothers fell substantially, suggesting that it is the economy—not the EITC—that mainly drives participation changes.

Another concern about the generally positive labor force participation effects of the EITC regards second earners in married households. For these individuals, the EITC produces a negative work effect because the level of benefits is based on household income. So if a spouse decides to start working, the family will receive less EITC in most cases.16

Now let's look at the other way that the EITC affects work incentives—hours worked. For existing workers, the EITC creates a complex mix of incentives to either increase or decrease hours worked. Workers face an "income effect," which may cause some individuals to reduce work because the EITC allows them to meet their income needs with less work. Workers also face a "substitution effect," meaning that the EITC makes working more valuable compared to not working.

The substitution effect varies depending on whether individuals are in the phase-in, flat, or phase-out income ranges of the EITC. Thus, at different income levels people may respond to the credit by seeking to work either more or less. Here is how one study described the effects:17

- "In the phase-in region, the EITC leads to an ambiguous impact on hours worked due to the negative income effect and positive substitution effect."

- "In the flat region, however, the EITC produces a negative income effect leading to an unambiguous reduction in hours worked."

- "In the phase-out region, the EITC produces a negative income and negative substitution effect leading again to an unambiguous reduction in hours worked."

To summarize, people have an incentive to reduce hours worked in both the flat and phase-out ranges of the credit. As it turns out, about three-quarters of people taking the EITC are in those two ranges where the work incentives are negative.18 So economic theory indicates that a large majority of people taking the EITC have an incentive to work less, not more. Based on this factor, a Tax Foundation simulation found that the EITC reduces overall U.S. output and employment.19

Consider a single parent with two children, as in Figure 2. She would have a disincentive to increase her work effort in the large income range from $13,870 all the way to $44,454. Above $18,110 she faces an EITC phase-out rate of 21 percent, so for each extra $1,000 she earns, her EITC payment is cut by $210. That cut is similar in effect to a 21 percent marginal tax rate on her work effort.

As the EITC has grown and benefits have become larger, a faster phase-out rate has become necessary. Put another way, the higher EITC benefits are, the more of a negative work effect is created from the phase-out, or marginal tax rate, effect.

However, while there is strong theoretical support that the EITC will reduce hours worked, there is not strong empirical evidence. The negative work effects are hard to see in the data. Some studies have found modest negative effects for some types of workers, particularly married mothers.20

There are additional concerns regarding the EITC's possible negative hours-worked effects. For one thing, half of the states now have their own state-level EITCs. These generally allow taxpayers to claim a percentage of the federal credit on their state returns, ranging from 3.5 percent to 40 percent.21 By boosting the credit, state EITCs increase marginal tax rates during the phase-out range, and thus add to work disincentives.

Furthermore, EITCs are only one part of federal and state fiscal systems that create disincentives to increase market earnings. A study by Tax Policy Center (TPC) scholars examined marginal tax rates on a hypothetical low-income single parent with two children in each of the states.22 As her earnings rise, she pays more payroll taxes and possibly more income taxes, and the benefits from the EITC, food stamps, and Temporary Assistance for Needy Families are reduced. On average, across the states, the TPC study found that the parent would face a marginal tax rate of about 50 percent in moving from a poverty level of income to twice the poverty level. For a married couple with two kids, the marginal tax rate averaged about 60 percent.

When the TPC scholars added the effect of reduced Medicaid benefits as incomes rise, the calculated marginal tax rates were even higher. The rates exceeded 100 percent in some states, meaning that a worker would actually be better off with reduced market earnings.

The TPC study did not include the effects of health care subsidies under the Affordable Care Act (ACA). But generous ACA benefits also phase out as income rises above the poverty level, and thus further push up marginal tax rates for affected individuals.23

In sum, the overall work incentive effect of the EITC is mixed—some individuals may be encouraged to enter the labor force, but others may be discouraged from earning additional market income. On top of the EITC effects are the anti-work effects of numerous other welfare programs. Unfortunately, many federal and state programs undermine incentives for millions of moderate-income Americans to advance in the market economy with rising earnings from work.

Errors and Fraud

A major weakness of the EITC is the program's high rate of overpayments, which are caused by math errors, misunderstanding of the rules, and fraud. The EITC error rate has been more than 20 percent since at least the 1980s.24 The Internal Revenue Service reports that the EITC error and fraud rate in 2014 was 27 percent, which amounted to $18 billion in overpayments.25

People are receiving excess EITC payments based on false information about such items as their income level, filing status, and qualifying children. The EITC is an easy target for dishonest filers because it is refundable, meaning that people can simply file false tax returns and see if the Treasury sends them a check. Errors and fraud also plague the other large refundable credit, the child tax credit (CTC). The improper payment rate for the CTC is more than 25 percent, thus wasting about $6 billion a year.26

Part of the problem with the EITC is that unscrupulous tax preparation firms prey on unsuspecting workers, including many immigrants who have poor English skills. For a fee, firms help workers file claims, and they also provide loans in anticipation of EITC refunds. Typically, half of the EITC tax returns completed by paid preparers overclaim the credit.27

It is remarkable that the EITC error and fraud problems have persisted for so long, despite the many efforts to fix them. This is one good reason to cut or end the EITC. It is unfair to the taxpayers who fund the program for the government to misspend so much of their money year after year.

EITC Complexity

As a general rule, tax credits are a complex and unnecessary part of the income tax code. Congress can and should create a simple and neutral tax code with no credits for low earners, high earners, or businesses.

The EITC is a particularly complex credit. Benefits change as income rises, with four phase-in rates and three phase-out rates. It is adjusted by filing status and number of children. The rules regarding child eligibility are complex due to issues such as separation and divorce. There are rules and calculations regarding earned income, investment income, and adjusted gross income.

The EITC generates a large bureaucratic cost. Because of the high levels of error and fraud, the IRS must put major resources into training agents, advising and monitoring tax preparers, and auditing. The credit is so problematic that 39 percent of all IRS audits under the individual income tax are done on EITC filers.28 Without the EITC, the IRS would have little reason to audit low-income filers. And EITC audits are particularly time-consuming because of often unclear correspondence with tax filers and the need for multiple phone calls.29

For individuals, the IRS guidebook for the EITC (Publication 596) is 37 pages long. But the rules are so complicated that more than two-thirds of all tax returns claiming the EITC are done by paid preparers.30 That costs money, and so do the fees that are charged to many EITC claimants who receive refund anticipation loans. All in all, the EITC has led to the creation of tax-preparation industry of more than $3 billion annually in fee revenue.31

High Cost on Taxpayers

The EITC is primarily a spending program. As noted, 88 percent of the benefits—$60 billion a year— are payments to people who owe no income tax. While the recipients gain from this largesse, every dollar of that gain is a dollar of direct loss for other people who pay the taxes to support the program.

There is an indirect loss as well. The process of extracting taxes damages the economy because it causes people to reduce their productive activities, such as working and investing. The harm from the behavioral responses to higher taxes is called "deadweight losses."

For the federal income tax, studies have found, on average, that the deadweight loss of raising taxes by a dollar is roughly 30 to 50 cents.32 Based on his pioneering work, Harvard University's Martin Feldstein thinks that the loss may be higher, perhaps exceeding "one dollar per dollar of revenue raised, making the cost of incremental governmental spending more than two dollars for each dollar of government spending."33 But other estimates are lower than Feldstein's.

Suppose that Congress expands EITC spending by $10 billion a year. Does this expansion make any economic sense? The benefits would have to be higher than the total cost of about $15 billion, which includes the $10 billion direct cost to taxpayers plus another $5 billion or so in deadweight losses.

EITC proponents do not seem to consider the high costs. American Enterprise Institute scholar Michael Strain cheerleads for the EITC, saying it "channels social resources to meet a social goal."34 The problem is that there is no such thing as "social resources" in the sense of a free pool of community money. All $60 billion of annual refundable EITC payments must be extracted from taxpayers at a loss of about $90 billion, including the deadweight losses from higher taxes. Jobs are destroyed by that extraction and many investments are not made.

Analysts and reporters often point to the anti-poverty benefits of the EITC, claiming things such as the credit "pulled 6.5 million people out of poverty."35 But that is a meaningless statistic. If the government gives low-income individuals $60 billion, of course they will have more money in their pockets, and fewer of them will be below a measured poverty line.

But why not double or triple EITC benefits and try to pull even more people out of poverty? The answer is that we need to worry about the costs of federal programs, which are the harms done to other citizens and the broader economy. Expanding the EITC would create more fraud, higher administration costs, and added disincentives to increase hours worked in the phase-out range.

Furthermore, expanding the EITC—or any other federal spending program—would ultimately mean higher taxes, and thus more tax distortions and higher deadweight losses. Indeed, the deadweight losses from higher taxes rise more than proportionally as tax rates rise, which means that additional federal spending is more economically damaging than existing spending.36

Conservative supporters of the EITC often talk as if the credit is one welfare program that actually works. But they seem to be looking only at the benefits, and not the costs. One conservative writer, for example, says that expanding the EITC would be much better than raising the minimum wage because "it poses no threat of destroying jobs."37 But this ignores that extracting taxes from the economy to pay for the EITC certainly does destroy jobs.

Reform Options

The EITC was designed to counter the anti-work effects of welfare programs and the federal payroll tax. But as we have seen, the EITC creates a range of problems of its own, including errors and fraud, disincentives to increase earnings in the phase-out range, and deadweight losses caused by extracting taxes to pay for it.

The EITC should not be expanded. Indeed, the best long-term solution would be to end the EITC, while also cutting other welfare programs and the payroll tax. At the same time, policymakers should pursue policies to boost wages and increase job growth. For example, cutting the corporate income tax rate would boost business capital investment. That would generate higher demand for labor, and thus raise wages and create more opportunities for American workers over time.

In sum, we do not think that the argument for the EITC is very convincing. The credit creates a modest increase in workforce participation by single mothers, but that benefit is outweighed by the work disincentives during the phase-out range, billions of dollars of errors and fraud, substantial paperwork costs, and the damage caused by the higher taxes needed to fund the program.

Notes:

1 GOP presidential candidate Jeb Bush has proposed expanding the EITC, as has Ways and Means Committee chairman Paul Ryan. The Ryan and Obama plans are discussed in Richard V. Reeves and Joanna Venator, "Are Obama and Ryan Proposals for an EITC Expansion Pro- or Anti-Mobility?" Brookings Institution, August 1, 2014.

2 Tax Policy Center, Table T15-0118, www.taxpolicycenter.org, July 28, 2015.

3 About three-quarters of people taking the EITC are in income ranges where the incentive to increase hours worked is negative. See Nada Eissa and Hilary Hoynes, "Redistribution and Tax Expenditures: The Earned Income Tax Credit," National Bureau of Economic Research Working Paper no. 14307, September 2008, p. 5.

4 Tax Policy Center, Table T15-0049, www.taxpolicycenter.org, June 23, 2015. We use "households" to mean "tax units."

5 Tax Policy Center, Table T15-0082, www.taxpolicycenter.org, June 25, 2015.

6 Congressional Budget Office, "The Distribution of Household Income and Federal Taxes, 2011," November 12, 2014. See the supplemental data.

7 Tax Policy Center, "Earned Income Tax Credit Parameters 1975-2015," November 3, 2014.

8 Estimate for 2015 from Tax Policy Center, Table T15-0118, www.taxpolicycenter.org, July 28, 2015.

9 Gene Falk, "The Earned Income Tax Credit (EITC): An Overview," Congressional Research Service, October 22, 2014.

10 Andrew Leigh, for example, finds that increases in the EITC reduce wages for people without college degrees. See Andrew Leigh, "Who Benefits from the Earned Income Tax Credit?" B.E. Journal of Economic Analysis and Policy 10, no. 1 (May 2010).

11 Jesse Rothstein finds that "employers capture about $0.36 of each dollar spent on the program through reduced wages." See Austin Nichols and Jesse Rothstein, "The Earned Income Tax Credit (EITC)," National Bureau of Economic Research Working Paper no. 21211, May 2015, p. 49.

12 Nichols and Rothstein provide a good summary of the research.

13 Evidence summarized by Nichols and Rothstein.

14 One skeptic is Lawrence M. Mead, "Overselling the Earned Income Tax Credit," American Enterprise Institute, September 22, 2014.

15 See Figure 8 in Nichols and Rothstein.

16 The EITC will be cut if the primary earner is in the flat or phase-out ranges of the credit, which is where most recipients are.

17 Nada Eissa and Hilary Hoynes, "Behavioral Responses to Taxes: Lessons from the EITC and Labor Supply," National Bureau of Economic Research Working Paper no. 11729, November 2005, p. 7.

18 Nada Eissa and Hilary Hoynes, "Redistribution and Tax Expenditures: The Earned Income Tax Credit," National Bureau of Economic Research Working Paper no. 14307, September 2008, p. 5.

19 Michael Schuyler and Stephen J. Entin, "Case Study #7: The Earned Income Tax Credit," Tax Foundation, August 6, 2013. However, the study did not take into account the positive labor force participation effect.

20 Nada Eissa and Hilary Hoynes, "Behavioral Responses to Taxes: Lessons from the EITC and Labor Supply," National Bureau of Economic Research Working Paper no. 11729, November 2005, p. 15.

21 Tax Policy Center, "State EITC Based on the Federal EITC," May 6, 2015.

22 Elaine Maag, et. al., "How Marginal Tax Rates Affect Families at Various Levels of Poverty," National Tax Journal 65, no. 4 (December 2012).

23 Casey B. Mulligan, "Average Marginal Labor Income Tax Rates under the Affordable Care Act," National Bureau of Economic Research Working Paper no. 19365, August 2013. See also Casey B. Mulligan, "The New Employment and Earnings Taxes Created by Social Programs," testimony to the House Ways and Means Committee, June 25, 2015.

24 U.S. Treasury, Inspector General, "The Internal Revenue Service Is Not in Compliance With Executive Order 13520 to Reduce Improper Payments," August 28, 2013, Figure 2. And see Joint Committee on Taxation, "Description of Present Law and Discussion of Issues Relating to the Earned Income Tax Credit," JCX-27-95, June 14, 1995, p. 14.

25 Cited in Government Accountability Office, "Government Efficiency and Effectiveness: Opportunities to Reduce Fragmentation, Overlap, Duplication, and Improper Payments and Achieve Other Financial Benefits," GAO-15-440T, March 4, 2015, p. 35.

26 U.S. Treasury, Inspector General, "Existing Compliance Processes Will Not Reduce the Billions of Dollars in Improper Earned Income Tax Credit and Additional Child Tax Credit Payments," September 29, 2014, p. 8.

27 Internal Revenue Service, "Compliance Estimates for the Earned Income Tax Credit Claimed on 2006–2008 Returns," August 2014, p. 26.

28 Internal Revenue Service, "Data Book 2014," 2015, Table 9a.

29 GAO, GAO-15-440T, p. 36.

30 GAO, GAO-15-440T, p. 37.

31 Nichols and Rothstein, p. 12.

32 Edgar K. Browning, Stealing from Each Other: How the Welfare State Robs Americans of Money and Spirit (Westport, CT: Praeger Publishers, 2008), pp. 156, 166, 178.

33 Martin Feldstein, "How Big Should Government Be?" National Tax Journal 50, no. 2 (June 1997).

34 Michael R. Strain, "Earned Income Tax Credit Does Better Job of Lifting Workers from Poverty," American Enterprise Institute, May 1, 2014.

35 Reeves and Venator.

36 Greg Mankiw notes, "It is a standard proposition in economics that the deadweight loss of a tax rises approximately with the square of the tax rate. ... If we double the size of a tax, the deadweight loss increases four-fold." See Greg Mankiw, "An Expositional Challenge," Greg Mankiw's Blog, November 22, 2006.

37 Ramesh Ponnuru, "Republicans Can Minimize the Minimum Wage," BloombergView, May 19, 2014.

About the Authors