President Bush has proposed overhauling the federal tax code, and he has appointed a panel to provide him with reform options by the end of July. One priority of reform is to reduce the distortionary effects that tax laws have on the nation’s health care system. A good solution would be to liberalize health savings accounts. Expanded HSAs could reduce health care costs and increase individual choice and control over medical decisions.

How the Tax Code Distorts Health Care

Employer-sponsored health insurance is exempt from federal income and payroll taxes, which induces employers to substitute health coverage for wages. This exemption is the largest special break in the tax code, valued at $126 billion annually.1 It is the reason that nearly 70 percent of nonelderly adults have employer-based coverage.

The tax exemption distorts the efficient functioning of health care markets in three main ways:

- It encourages people to have more health insurance coverage than they otherwise would;

- It favors employer-provided insurance over other types of health insurance; and

- It favors spending on health care rather than non-health expenditures or saving.

These distortions encourage first-dollar health coverage, rather than more efficient high-deductible coverage. They reduce incentives for patients and providers to pursue lowcost, high-quality care. They shift control over medical decisions from individuals to employers and insurance companies. And because most tax benefits for health care are contingent on whether employers provide coverage, the system treats workers unequally.

On the whole, these distortions have the effect of reducing consumer choice and competition, and of fostering overutilization and high costs. The current tax preference for employer-sponsored health insurance is thought to create “deadweight losses,” or inefficiency costs, of more than $100 billion per year.2

Expanding Health Savings Accounts

In a perfect world, tax policy would be neutral toward health expenditures. Consumers would make medical and health insurance decisions based on the value of different alternatives, free from tax distortions. Some analysts are proposing limiting tax distortions by capping the tax benefits for employer-sponsored insurance. Others advocate giving deductions or credits to individuals to purchase insurance and medical care directly. These ideas have merit, but a better route to health care reform would be to expand health savings accounts.

HSAs were created by Congress in the Medicare Modernization Act of 2003. They combine high-deductible health insurance with a personal savings account for medical expenses. Money deposited into HSAs by employers or employees is untaxed. HSA funds may be withdrawn tax-free for medical purchases, and any unused balances grow tax-free indefinitely.

As they exist today, HSAs make consumers more costconscious users of routine care, but they still encourage excessive coverage and do not give consumers full control over their health care dollars. HSAs do reduce the tax bias toward excess coverage, but Congress requires HSA holders to purchase insurance, and it imposes coinsurance limits that require some to buy more coverage than they want. Also, HSAs only marginally offset the bias in favor of employer-provided coverage. Those who obtain HSAs on their own can make pre-tax deposits, but they must purchase the mandated insurance with after-tax dollars. Thus, current HSAs only modestly reduce the tax code’s distortion of health care markets.

Expanding HSAs into larger, more flexible accounts, however, can bring more equity to the tax code, and more choice and competition to the health care sector. Three changes are necessary to create large HSAs:

- Increase HSA contribution limits to $8,000 for singles and $16,000 for families;

- Eliminate the requirement that HSA holders obtain health insurance; and

- Allow tax-free HSA withdrawals for health insurance premiums as well as health care.

These changes would give workers full ownership and control over all their health care dollars, and would vastly expand choice and competition in health care markets.

More Equity, More Choice, More Competition

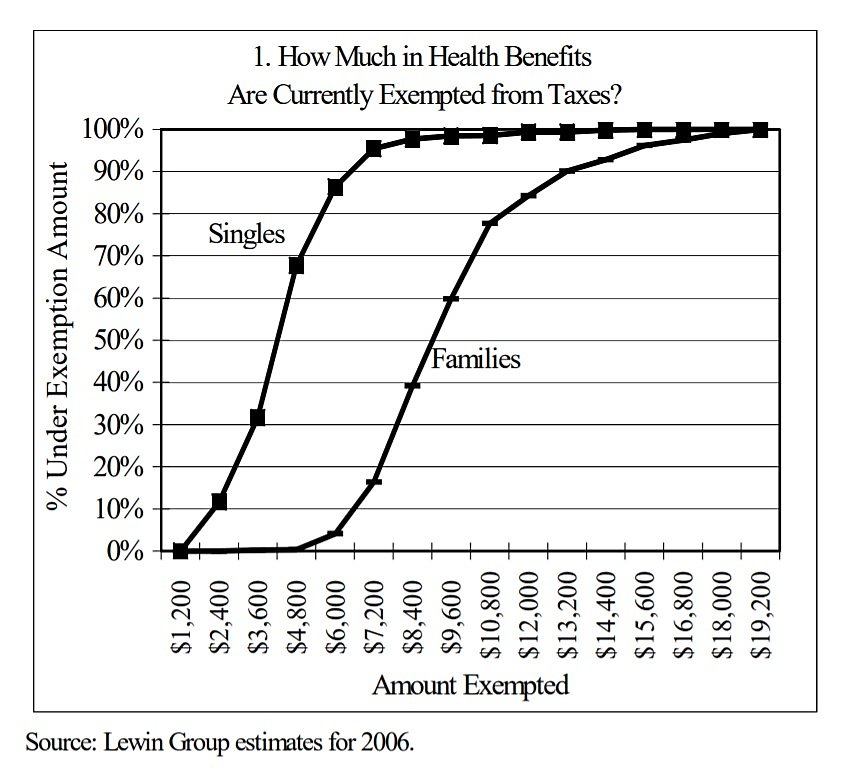

With contribution limits of $8,000 for singles and $16,000 for families, 97 percent of workers would be able to receive the full value of their current health benefits as a cash deposit into their HSAs (see Figure 1). As with 401(k)s, workers could decide how much to deposit and could vary their contributions from year to year. With the bias toward employer-based coverage eliminated, only a bias toward employer contributions would remain (as only employer contributions would avoid payroll taxes).

Large HSAs would make health care much more equitable. Today, high-income earners receive the largest tax benefits, while many low-income workers receive zero benefits because their employers offer no coverage. Large HSAs would extend tax benefits to low-income workers who today receive none because employers who do not provide coverage could still make HSA contributions.

Large HSAs would give workers far greater freedom of choice. Workers could use their HSA funds (and non-HSA funds) to purchase insurance from their employer or any other source. Alternatively, they could forgo insurance to build larger HSA balances.

Large HSAs would create more competitive health care markets. Because HSA holders would be spending their own money on their own behalf, they would demand greater value. Consumers would pressure providers to reduce costs, provide better information, and give high-quality service. Competition would force all providers and insurers to focus on consumers’ needs.

Possible Concerns about Large HSAs

Some analysts may object that expanding HSAs would create revenue losses for the government. But every dollar lost to the Treasury would represent even more dollars being put aside for future health care needs. Large and growing HSAs would help fill the enormous gap that future retirees will face between what Medicare promises and what it can deliver.

Others may object that large HSAs would allow some workers to leave employer plans, which may increase premiums for those who remain. Similar objections were raised about current HSAs, yet there is little evidence of such adverse selection. Even if there were, it does not follow that workers who can find a better deal elsewhere should be forced to stay with their employer’s plan.

Conclusion

Other proposed reforms share common elements with the changes proposed here. President Bush wants to make individually purchased health insurance premiums taxdeductible, just as they would be under large HSAs. Another idea, included in House-passed legislation in 2003, is to allow HSAs with lower deductibles or even without any health insurance. Other proposals seek more flexibility with regard to contributions. Congress can pursue such reforms piecemeal. Even better, it can rapidly infuse more equity, choice, and competition into health care with large HSAs.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.