Many commentators have decried the recent drop in oil prices as “bad for the U.S. economy,” to use a standard expression expressed on Bloomberg TV. But people also complain that high or rising oil prices are bad for the economy. It cannot be true that both higher and lower oil prices are bad.

A drop in oil prices benefits consumers of derived goods and services (gasoline, heating oil, etc.) and harms oil producers. A prima facie reason to believe that an oil price cut is good is that the welfare of consumers, not producers, is the paramount criterion; the goal of economic life is consumption, not production. Conversely, an increase in oil prices will benefit producers and harm consumers, which suggests that it is bad.

That answer, however, is not totally satisfactory. A change in the price of oil (or any good) generates a long chain of consequences: on consumption and production, including the effects on substitutes and complements of oil; on measured inflation; and so forth. Pundits also worry about the effect of rapidly declining oil prices on investment in the oil industry.

IMPORTANT DISTINCTIONS

A clearer picture of the economic effects of falling oil prices is necessary. In order to gauge the net result in terms of “good” or “bad,” economic theory suggests that we first need to make several important distinctions.

First, we must distinguish between supply and quantity supplied (just as we make the same distinction on the demand side). A change in supply is a shift in the whole supply curve: more quantity is supplied at any price. A change in quantity supplied is a move along a given supply curve in response to different prices. Neglecting this distinction, some commentators have claimed that lower oil prices will bring forth less supply, which will push prices back up. Such circular and muddled reasoning would lead to the absurd conclusion that prices never change: more supply would cause lower prices, which would bring less supply and higher prices.

What happens in reality—and in theory—is the following: When oil prices are pushed down by increased supply, it is because producers have become capable of profitably supplying more oil at any given price. The whole supply curve has shifted outward and the new price is justified by the new supply conditions. It is true that marginal producers, who were barely profitable at the higher prices, will be pushed out of the industry by the lower prices or be forced to cut their production to an economically sustainable level, but this effect is already incorporated in the new supply curve.

Second, we must distinguish between long-term trends and short-term reactions. In the short run, supply and price can temporarily overshoot their equilibrium. Producers can make mistakes. Speculators may misjudge the future. Moreover, the presence of a cartel, the Organization of the Petroleum Exporting Countries, blurs the supply picture: both market power and political factors can disturb the simple supply and demand model I have presented. But OPEC’s market power is easily exaggerated; not only is it unstable like any cartel, but now (at the end of 2014) it accounts for only one-third of the world’s crude oil production.

There is no way to know where oil prices will go, especially in the short run. Political factors or supply disruptions by war or terrorism in the Middle East could provoke temporary price spikes, as we have seen since the 1970s. But as Julian Simon argued in his book The Ultimate Resource (Princeton University Press, 1981, 1996), when the price of oil increases, human ingenuity and entrepreneurship work to find alternative sources or techniques of production, ultimately shifting supply outward.

A third essential distinction is between a mere change in the relative price of oil (its price in terms of other goods and services) and a change in its production possibilities. Making this distinction helps us to see what is happening in the oil market.

Suppose that, for whatever reason, consumers decide to consume more oil at the expense of other goods. For example, they may want to save on beer in order to travel more. The price of the forgone goods will go down and the price of oil up; more oil will be produced and fewer other goods. What has changed in this case is the relative price of oil in terms of other goods. A gallon of oil costs more in terms of beer, and a bottle of beer less in terms of oil. This should not be a dramatic revelation because all prices are relative prices. They are only thinkable in terms of something else—dollars for example, and thus the other goods that dollars can buy.

PRODUCTION POSSIBILITY FRONTIER

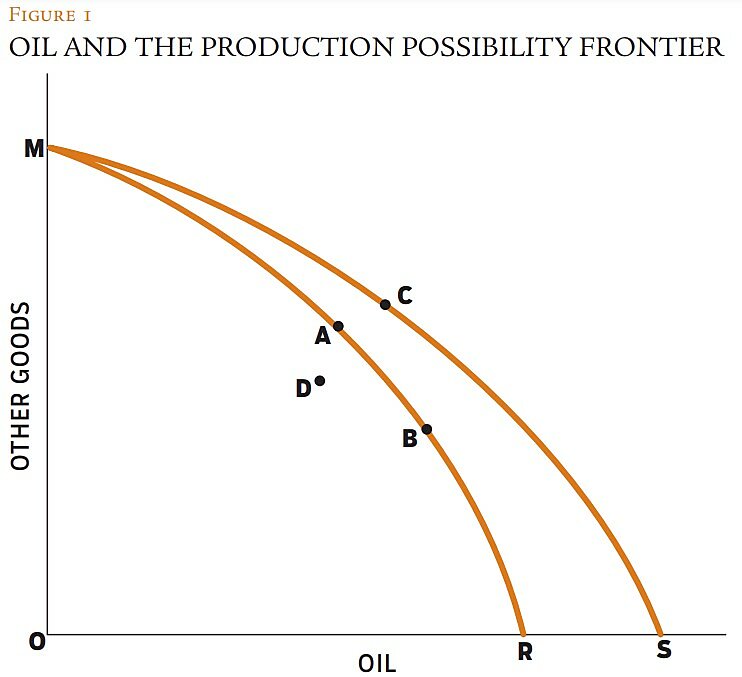

Consider Figure 1, where the quantity of oil produced is measured on the horizontal axis and the quantity of other goods produced is measured on the vertical axis. The curve MR represents what economists call society’s production possibility frontier: for a given production of other goods, it shows the maximum quantity of oil that can be produced, and vice-versa.

A situation represented by a point like D under the production frontier is inefficient because, given the available resources, more of all goods could be produced—at A for example—without reducing the production of any good. Economic efficiency consists largely in moving toward society’s production frontier.

Once society stands on its production frontier, the situation is different. Because resources are limited and none are unemployed at any point on the frontier, the more oil is produced, the fewer other goods can be produced, and vice-versa. In the sort of relative price change I have considered thus far, the economy moves from A to B.

As more oil is produced, its price in terms of the other goods increases, which is indicated by a steeper slope (in absolute terms) of the production frontier at B compared to A. Conversely, of course, the price of other goods in terms of oil declines. The reason why costs and prices change along the production frontier is that as more oil is produced, resources (labor, steel, etc.) that were more efficient in the production of other goods are reallocated to oil. Using less efficient resources means that more will be needed and that, therefore, the (marginal) cost of oil production will increase.

The concept of the production frontier allows us to reduce to one criterion all the factors that matter in determining whether something is good or bad “for the economy.” This criterion is the quantity of goods produced and consumed: the more of them the better. Some individuals may not want to consume certain goods and their preferences will influence where the economy moves along the production frontier, but that will not change the argument made here.

So our question has been reduced to whether B is better or worse than A for the economy. We can see why there is really no way to tell. In situation B, some individuals are better off but others are worse off. For example, those who did not want more oil still have to pay more for it. A change in relative prices is neither good nor bad economically because “the economy” is made of many different individuals with different preferences.

At a more abstract level, we know that prices are useful to transmit the right signals regarding people’s preferences and resource scarcities. If this coordination role fails, society will not reach the production frontier. What is relevant is not whether a price has gone up or down, but whether it incorporates correct information. In general, a sufficient condition for this is that prices be determined by free exchange on free markets. Although the oil market is certainly not as free as it could be because of multiple political interventions, it is still better to let the price change according to the (imperfect) interplay of supply and demand. From this vantage point, there are no good or bad prices, but only free-market prices and arbitrarily controlled prices.

THE FRACKING REVOLUTION

New technologies—fracking and horizontal drilling—have made more “tight oil” accessible and shifted America’s (and the world’s) production frontier toward MS. The U.S. Energy Information Administration estimates that 26 percent of the technically recoverable crude oil resources in the United States and 10 percent at the world level now lie in shale. For a given production of other goods, more oil can now be produced, and much of it comes from formations that were not previously exploitable. The easiest way to understand the shift in the production frontier is to ask how much oil could be obtained if no other goods were produced at all. In Figure 1, the answer to this was OR, but now it is OS. The production frontier has shifted from MR to MS.

The economy has moved from A on the old production frontier to a point like C on the new one (the scale is exaggerated for better visualization). This move corresponds to the effect of lower oil prices on gross domestic product. If we consider a $50 drop in the price of crude, as happened between June and December 2014, and use the estimate of UBS (a Swiss bank), GDP would show a permanent increase of 0.5 percent in the United States and 1 percent at the world level. (Note that the graph can be used to analyze either the American or, mutatis mutandis, the world production frontier.)

How do we know that the drop in oil prices is more the result of a supply increase than a drop in demand? One indication is that, as of early January 2015, total oil consumption has been increasing—not decreasing—in America and the whole world, despite the recent economic slowdown in Europe. We also know that, since 2008, crude oil production in the United States has increased some 70 percent thanks in large part to fracking and horizontal drilling in tight oil formations.

POTENTIALLY GOOD

Our original question has been further reduced to a more precise and manageable one: is an outward shift of the production frontier good or bad? Because this shift will normally be accompanied by a change in relative prices (depending on where the economy lands on MS), we could think we have the same problem as before. But the situation is different. An outward shift in the production frontier generates a potential gain for everybody. More of all goods can be produced—compare C to A—so that every individual can potentially have more of what he likes. At worst, depending on where C is on the new production frontier, some individuals might lose and others gain—in which case the economist cannot make an evaluation. But at the very least we can say that the result cannot be bad.

From an economic viewpoint, then, we cannot say that the drop in oil prices is bad for the economy. We could unambiguously say that it is good if we knew that all individuals are participating in the gains—or, at least, that no individual experiences a loss. An alternative way to say that the price drop cannot be bad is to say that it is potentially good. If there is more of all goods, everyone can potentially benefit.

On the contrary, an inward shift of the production frontier—because of, say, the destruction of productive capacity by war—cannot be good. In the most general case, the economist will not be able to make an evaluation because some individuals will gain and others will lose. The shift cannot be deemed good because if less is produced, then at least some individuals will have less.

We see here what distinguishes the economist from the moral or political philosopher: the former refuses to make value judgments. The economist tries to stay in the realm of the positive, while the moral philosopher dwells in the domain of the normative. For the economist who takes this distinction seriously, only a situation where at least some people gain and no one loses can be considered unambiguously good; and only a situation where at least some people lose and no one gains can be considered unambiguously bad. When a change is seen as an improvement by some individuals and a loss by others, the economist cannot make a welfare evaluation.

Some claim that this approach itself relies on a particular value judgment, namely that the subjective preferences of all individuals count equally or (to put things another way) that unanimous consent to a change in conditions is necessary. If we consider this to be a value judgment, it is a minimal one.

Cost-benefit analysis is a way to avoid any indeterminacy, but it does require the analyst to weigh the benefits of some individuals against the costs borne by others. In that case, one could say that a shift outward of the production frontier is unambiguously good and a shift inward is unambiguously bad. But I think this confuses the moral and the economic.

So what do we conclude from an economic approach that excludes or minimizes moral considerations? That little can be said about a mere change in the relative price of oil except that it should be determined on free markets if it is to play its coordinating role. But if a drop in oil prices is generated by an outward shift in the production frontier, one cannot say it is bad. From an economic viewpoint, such a change is potentially good and, at worst, indifferent.

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.