The “tax exclusion” for employer-sponsored health insurance shields workers from paying income or payroll taxes on such benefits. The exclusion is an accident of history that predates modern health insurance and is roughly as old as the income tax itself. It fuels excessive health insurance coverage, medical spending, and health care prices and ties health insurance to employment. It has required Congress to intervene countless times to address problems it creates.

The exclusion requires a worker to let her employer control a sizable share of her earnings, to enroll in a health plan that is likely not her first choice, and to pay the remainder of the premium out of pocket. Overall, the tax code effectively threatens U.S. workers with $352 billion in additional taxes in 2022 if they do not let their employers control $1 trillion of their earnings. The additional tax that workers pay if they do not accept those terms constitutes an implicit penalty.

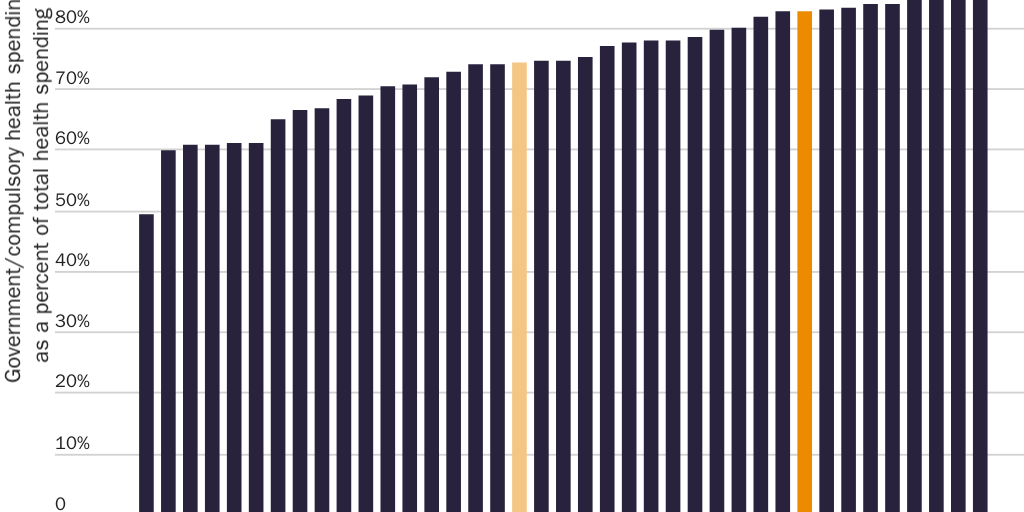

The tax code thus limits a worker’s ability to make her own health decisions. In the United States, compulsory health spending accounts for 83 percent of overall health spending, the ninth highest share among 34 advanced nations. The tax exclusion is the single largest contributor to compulsory health spending.

Reforming the exclusion would free U.S. workers to control $1 trillion of their earnings that employers currently control, give consumers more health care choices, and make health care more accessible. Building on the bipartisan success of tax-free health savings accounts appears to present the best politically feasible opportunity for reform. The United States will not have a consumer-centered health sector until workers control the $1 trillion of their earnings that the exclusion forces them to let employers control.

Introduction

The most important health care right is the right to make one’s own health decisions. A key component of that right is the right to control one’s earnings. Taxes deny the taxpayer the right to choose whether and how to spend those resources on medical care. Even if governments use the revenue to subsidize medical care, taxes deny workers the right to choose how to spend those funds.

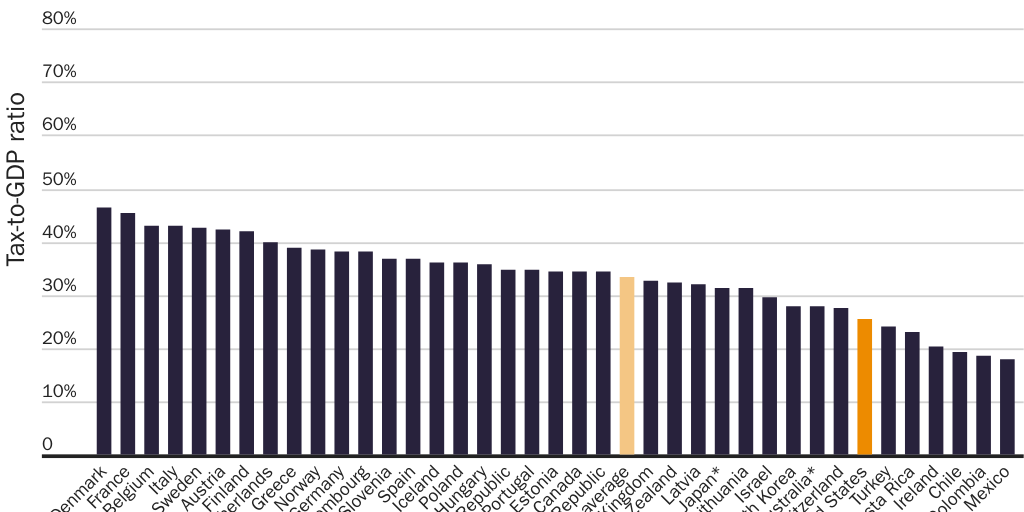

The United States would appear to fare well among advanced nations in terms of protecting this element of health care rights. Taxes consume a relatively small share of gross domestic product (GDP) in the United States. “The United States ranked 32nd out of 38 [Organisation for Economic Co-operation and Development] countries in terms of the tax-to-GDP ratio in 2020. In 2020, the United States had a tax-to-GDP ratio of 25.5% compared with the OECD average of 33.5%.”1 (See Figure 1.) The United States’ high debt-to-GDP ratio threatens this enviable tax ranking. In the United States, government debt is 162 percent of GDP, lower than only Japan (257 percent), Greece (238 percent), and Italy (184 percent) among OECD nations.2 If and when government begins to pay down the debt, the U.S. tax-to-GDP ratio could rise significantly.

The United States does not respect the right to choose whether and how to spend one’s resources on medical care as much as international comparisons might suggest. Forcing taxpayers to send their money to the government is not the only way tax laws infringe on taxpayers’ rights to control their income and make their own health decisions. The U.S. tax code contains a peculiar feature that allows workers to pay less in taxes, but only if they give up control of a sizable share of their earnings and their choice of health insurance. The “tax exclusion” for employer-sponsored health insurance shields workers from having to pay income or payroll taxes on compensation they receive in the form of health benefits. The exclusion predates modern health insurance and is roughly as old as the income tax itself.

From an accounting perspective, the exclusion is a tax break: it reduces the tax liability of workers who enroll in employer-sponsored coverage. It comes with conditions, however. To take advantage of the exclusion, a worker must let her employer control a sizable share of her earnings (typically more than twice the amount the exclusion saves her in taxes), enroll in a health plan that is likely not her first choice (or even her second choice), and pay any remaining share of the premium out of pocket. For some workers, the costs of those conditions completely offset the exclusion’s benefits.

The tax code coerces workers into accepting those terms. While the exclusion reduces the tax liability of workers with employer-sponsored coverage, it is equally accurate to say that the tax code presents workers with a choice: they can either enroll in employer-sponsored coverage or pay higher taxes. The additional tax liability that workers must pay if they do not enroll in employer-sponsored coverage constitutes an implicit penalty that the tax code imposes on not accepting the exclusion’s terms.

Even if that penalty is implicit and unintentional, it is inherently coercive. If a worker refuses to enroll in employer-sponsored insurance and refuses to pay the additional tax that comes with that decision, the government will prosecute her for willful failure to pay taxes, fine her up to $25,000 plus court costs, and imprison her for up to one year.3 The exclusion’s implicit penalties are coercive even in cases where workers would have enrolled in employer-sponsored health insurance anyway, because they are no longer free to change their minds.

At the level of the individual worker, the implicit penalties are substantial. In 2021, the average employer-sponsored family-plan premium was $22,221 per year.4 Assuming a worker faced a marginal tax rate of 33 percent, the exclusion let her avoid paying $7,333 in federal taxes if she enrolled in such a plan. Those tax savings represent the implicit penalty she would have paid had she not enrolled in such a plan. When she decides whether to enroll in employer-sponsored coverage, the threat of having to pay a $7,333 penalty pushes her toward enrolling. At the same time the exclusion expands her freedom by giving her an option she otherwise would not have, the tax code uses compulsion to push her into choosing that option.

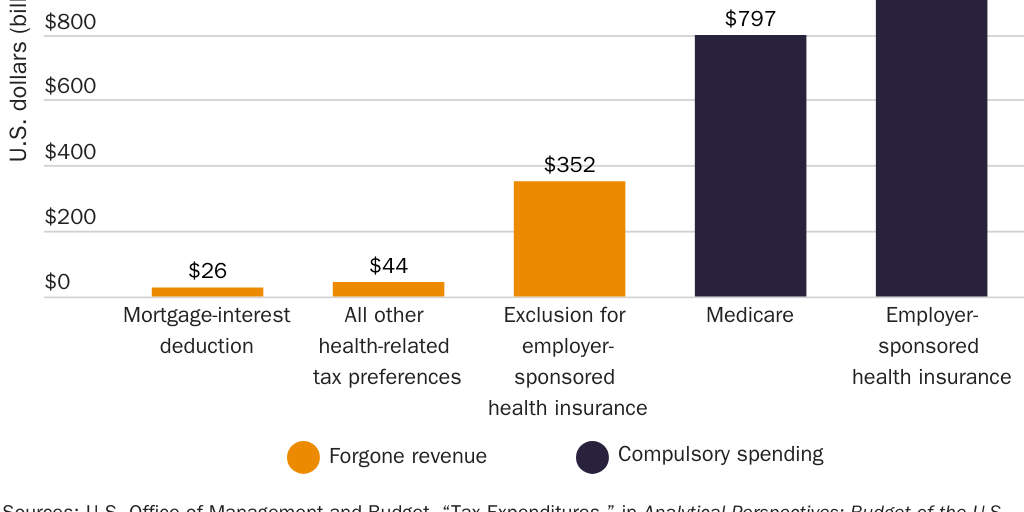

In the aggregate, the implicit penalties are massive. In 2022, employers and workers will spend approximately $1.3 trillion on employee health benefits.5 Without the exclusion, U.S. workers would have to pay approximately $352 billion in 2022 in additional federal taxes on that income.6 The federal government calls that $352 billion in forgone revenue a “tax expenditure.” More accurately, it is the sum of the penalties that the tax code threatens to impose on workers if they drop employer-sponsored coverage. That figure does not include the implicit penalties that workers who do not enroll in coverage through their employer are currently paying.

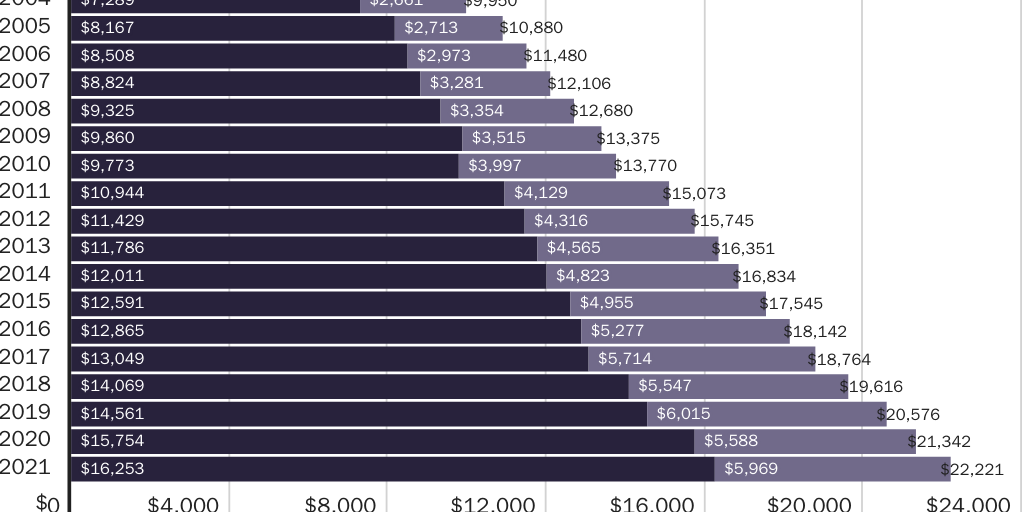

The threat of those penalties coerces workers into allowing their employers to control more of their money than the exclusion saves them. Again, the average annual employer-sponsored family-plan premium in 2021 was $22,221. On average, the employer paid $16,253 (73 percent) toward the premium. The worker paid the remaining $5,969 (27 percent) directly.7 Of the $1.3 trillion that employers and workers will spend on employee health benefits in 2022, employers will pay $944 billion on their workers’ behalf while workers will pay $327 billion directly.8

The nearly $1 trillion that employers spend on health benefits each year comes from workers, not from employers. Employers finance spending on health benefits by reducing other forms of employee compensation, typically wages.

At the same time the exclusion reduces a worker’s tax liability, then, it employs the coercive power of the tax code to deny her control of up to three times as much of her money as the code would otherwise claim. In 2021, the exclusion allowed a worker with the average employer-sponsored family plan and the average marginal tax rate to avoid paying $7,333 in taxes—but only if she let her employer control $16,253 of her income and then paid a further $5,969 of the premium directly. If she tried to control that $16,253 herself by working for a firm that offered that compensation as additional cash wages instead of health benefits, she would have had to pay an additional $7,333 in taxes. In 2022, the exclusion allows workers economywide to avoid paying $352 billion in federal taxes—but only if they let their employers control $1 trillion of their earnings and then pay a further $327 billion directly to enroll in health insurance plans their employers choose, control, and revoke upon separation.

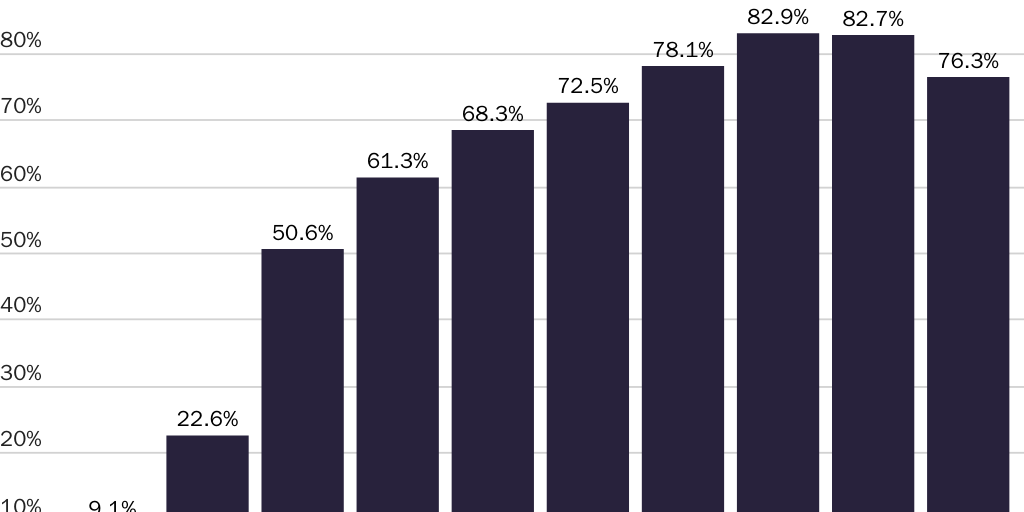

One may fairly describe the exclusion as creating an alternative type of tax. “The real cost of government—the total tax burden” includes “the cost to the public of … taking measures to avoid taxes.”9 Most (but not all) workers opt to pay the exclusion’s alternative “tax” because they believe it to be lower or less burdensome than the looming penalties. Ninety-one percent of workers work for firms that offer health benefits; 81 percent of those workers are eligible for those benefits. Among eligible workers, 77 percent—or 56 percent of all workers—enroll in the coverage their employer offers.10

Imperfect information may affect these decisions. Among the exclusion’s features is that it hides the costs of the conditions it imposes. Few workers understand how much money employers spend on health benefits or that the money comes out of their wages or that it is the exclusion denying them control over that income. Few workers research health insurance options outside those their employers offer. It is unclear how many workers would continue to take advantage of the exclusion if they had a fuller appreciation of the costs of its terms.

It is useful to compare the exclusion to an individual mandate to purchase health insurance. A mandate threatens an individual with financial penalties if she does not purchase the type of health insurance the government specifies. Given the exclusion, the tax code threatens an individual worker with thousands of dollars in additional taxes unless she enrolls in a specific type of health insurance (i.e., employer-sponsored). Supporters and critics may use different rhetoric to discuss the two types of measures. From an economic perspective, they are functionally equivalent.

The exclusion’s implicit penalties are indeed more coercive than Obamacare’s individual mandate. They apply to more people, allow the IRS more tools to coerce compliance, and have been using government compulsion to distort health insurance markets for a century, since before modern health insurance existed.

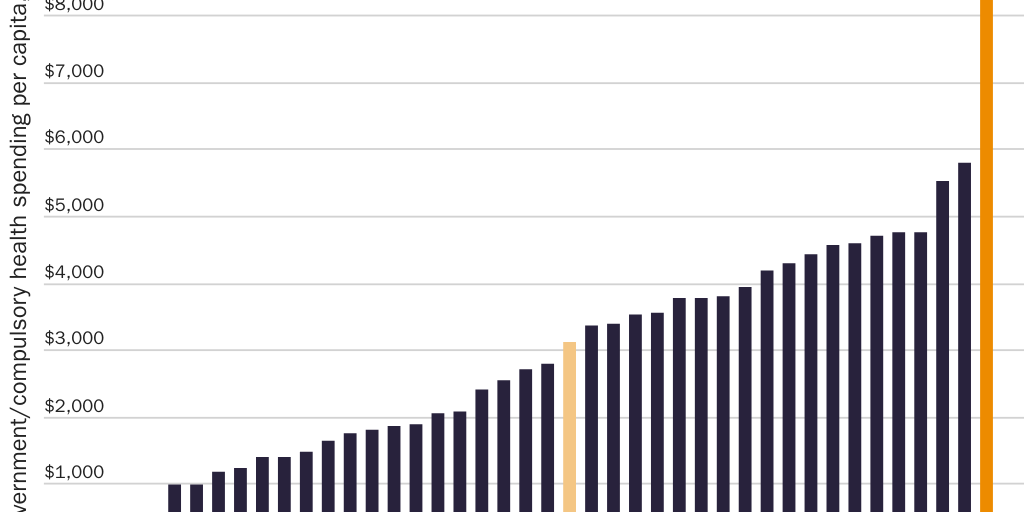

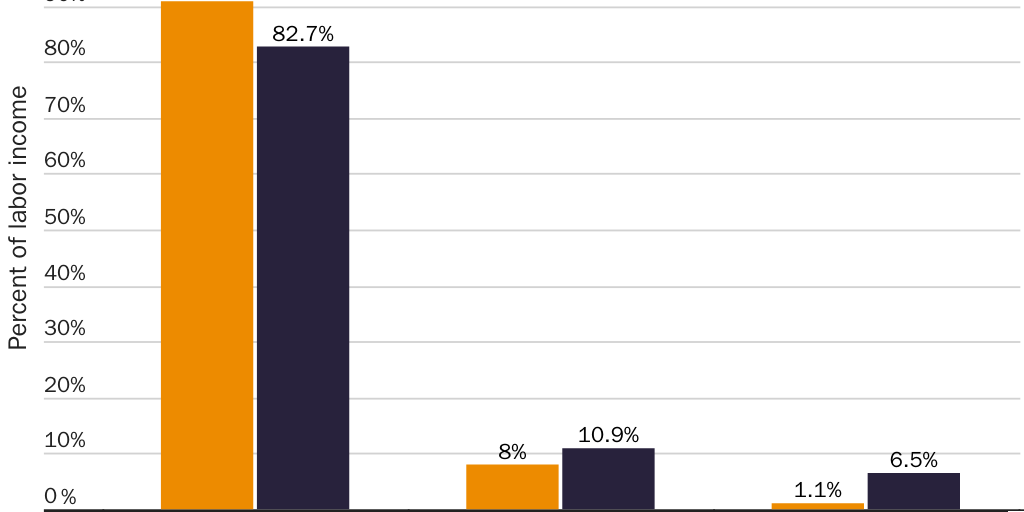

The exclusion is the largest contributor to compulsory health spending in the United States. According to the Organisation for Economic Co-operation and Development (OECD), in 2019 compulsory health spending accounted for 82.7 percent of U.S. health spending, the ninth-highest share among 34 member nations. (See Figure 2.) On both a per capita basis and as a share of GDP, compulsory health spending in the United States far exceeded that of any other OECD nation. Per capita compulsory health spending was $9,054 in the United States—56 percent more than in second-ranking Norway ($5,788) and nearly three times the OECD average ($3,117). (See Figure 3.) Compulsory health spending accounted for 13.9 percent of U.S. GDP—a 40 percent larger share than in second-ranking Germany (9.9 percent) and more than double the OECD average (6.6 percent). (See Figure 4.) The $1.3 trillion that the exclusion’s implicit penalties coerce workers into spending on health insurance is the largest single category of compulsory health spending in the United States.

![Figure 4 [print only]: Compulsory health spending comprised larger share of GDP in United States than in any other OECD nation in 2019](https://infogram-thumbs-1024.s3-eu-west-1.amazonaws.com/64b2c0ba-3942-4115-911f-5c267f62e368.jpg)

Though most workers take advantage of the exclusion, for some workers the costs exceed the benefits. Among workers whose employers offer coverage, 4 percent turn down the exclusion by declining that coverage (and all other coverage offers).11 Workers may decline to take advantage of the exclusion because they do not value health insurance, because they have such low incomes that the tax savings plus health insurance would not be worth sacrificing cash wages (equivalently, that the implicit penalties are too low to motivate them), or because of some combination of these or other factors. Among employers who do not offer coverage, 74 percent report that their employees would prefer a $2 per hour increase in taxable wages to untaxed health benefits.12 To the extent those employers accurately assess their employees’ preferences, it indicates workers would prefer to control that additional income themselves.

The costs of the exclusion can exceed its benefits even for workers who take advantage of it. In the simplest case, if the exclusion induces a worker to enroll in her employer’s coverage rather than an otherwise identical individual-market policy that would cover her between jobs, the cost of losing that coverage after she falls ill and separates from that employer (see Figure 12) could exceed the tax savings from enrolling in her employer’s plan. The price of one uninsured emergency department visit could easily wipe out the $7,333 in annual tax savings that the exclusion offers the average worker with family coverage.

From a societal perspective, the exclusion’s impact is unambiguously harmful. Economists have long argued that it distorts economic decisionmaking in ways that dramatically reduce social welfare. It distorts numerous sectors of the economy, none more than the markets for health insurance and medical care, where it increases prices for both. It is a major reason why 56 percent of the U.S. population obtains health insurance through an employer but why only 10 percent obtain it directly from an insurance company.13

The tax exclusion is one of the primary reasons the U.S. health sector is unaffordable and unaccountable to so many consumers. Diverting control over $1.3 trillion of insurer and provider revenue from consumers to employers leads the health sector to focus on the needs of employers at the expense of consumers. It leads to less consumer scrutiny of excessive prices and wasteful spending.

One version of the Golden Rule states, “Whoever has the gold makes the rules.”14 The societal-level equivalent is, “All economic systems serve those who control the money.” The United States will not have a consumer-centered health sector until workers control the $1.3 trillion per year that the tax exclusion coerces them into spending according to the government’s preferences.

How the Tax Exclusion Works

Employer-provided health insurance is a form of employee compensation. Unlike cash wages, Congress excludes what employers pay toward employee health benefits from the tax bases for federal income and payroll taxes. (Exemptions and deductions remove income from the tax base; an exclusion prevents income from entering the base.) The exclusion therefore shields workers from having to pay taxes on income they receive in the form of health insurance. A worker who received all of her compensation in the form of employer-sponsored health insurance would pay no income or payroll taxes.

The exclusion encourages employers to offer and pay for health benefits, and therefore to reduce cash wages, by penalizing workers unless they consent to these arrangements. In the aggregate, it coerces U.S. workers into letting employers control $1 trillion of their earnings each year by effectively threatening workers with $352 billion in additional taxes if they do not.

A Tax Differential between Health Benefits and Cash Wages

The exclusion shields labor income from the federal income tax and the Social Security and Medicare payroll taxes. Five out of six U.S. households and two-thirds of households in the lowest income quintile pay either federal income taxes, federal payroll taxes, or both.15 Since these taxes affect nearly the entire U.S. population, so does the tax exclusion.

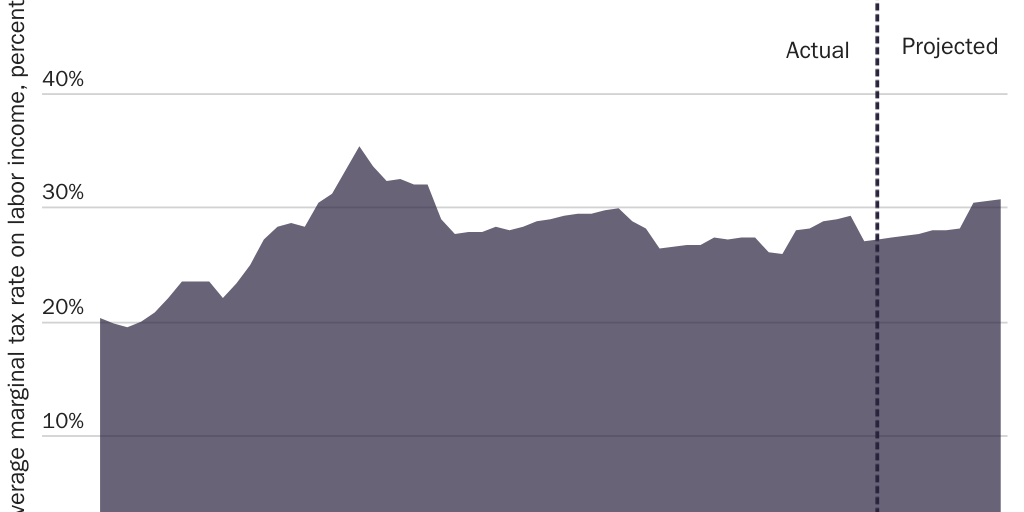

These taxes impose varying marginal tax rates that combine to produce an overall federal marginal tax rate on labor income for each taxpayer. The average federal marginal tax rate rises and falls over time. (See Figure 5.) The most recent Congressional Budget Office estimate suggests that the economywide federal marginal tax rate for cash labor income is 33 percent.16 That is, on average, Congress takes 33 cents from each additional dollar of cash that workers earn. The 42 states that impose an income tax push the overall marginal tax rate on cash labor income even higher.17

The exclusion thus creates a tax differential between the income that workers receive as cash versus health benefits. Workers pay a tax rate of 0 percent on income they receive as health benefits but (on average) a 33 percent marginal tax rate on income they receive as cash. If a worker takes $1,000 of income in the form of health benefits, she receives $1,000 in health benefits. If she takes that $1,000 as cash, Congress effectively penalizes her by taking $333 of it and leaving her with only $667. The worker may lose additional hundreds of dollars to state income taxes.

This tax differential is completely open-ended. It exists for every dollar workers earn. No matter how much a worker earns, or how much health insurance she already has, or how expensive, inefficient, and wasteful her employer’s health plan is, Congress effectively penalizes her for every additional dollar she takes as cash wages instead of additional health benefits.

Workers face this distorted tradeoff directly when choosing between more- versus less-expensive health plans that their employers offer. They face it directly when choosing between jobs that offer differing levels of health benefits. They face it indirectly when their employer makes changes to their health benefits each year.

The Flip Side of Any Incentive Is a Penalty

For every $1,000 in additional pay, then, the tax code effectively penalizes a worker $333 unless she lets her employer control all $1,000 and devotes it to health benefits. If two jobs offer equivalent total compensation but one offers health coverage and the other offers higher cash wages, the exclusion effectively penalizes a worker if she chooses the job that offers higher cash wages. In 2021, the average annual premium for employer-sponsored self-only (family) coverage was $7,739 ($22,221). At a marginal tax rate of 33 percent, the tax code effectively penalizes the worker $2,554 ($7,333) for taking the second job. The action the federal government takes in those scenarios is to tax. The exclusion turns that tax into the functional equivalent of a penalty for workers who make the “wrong” choice.

The exclusion can impose even larger effective penalties on workers who decline the coverage their employers offer. Labor markets will push employers to offer such workers additional, equivalent cash wages in lieu of coverage. (See the “Workers Bear the Full Cost of Health Benefits” section.) Like the compensating wage differential that another firm would offer, those additional cash wages are taxable. In certain cases, the IRS considers the mere offer of those additional cash wages to be taxable income to all workers—even those who enroll in the company health plan. A worker who accepts her employer’s offer of coverage can then end up paying taxes on the cash value of what the employer pays toward the premium, which subjects her to the implicit penalties that she had enrolled in the company health plan to avoid.

Featured Media Highlights

To enable those employees to avoid those implicit penalties, employers typically respond by not offering equivalent cash wages to workers who decline health benefits. Even though workers’ productivity presumably justifies that additional compensation, even though the offer of health benefits shows employers are willing to pay them that additional compensation, and even though another employer might lure those workers away by offering higher overall compensation, the desire of most workers to avoid the exclusion’s implicit penalties leads employers not to offer additional, equivalent cash wages to workers who decline health benefits.

In some cases, then, the exclusion’s implicit penalties lead employers to suppress compensation for workers who decline employer coverage. Those workers’ compensation can fall below the market level by an amount up to what the employer would have paid toward their coverage: on average, $6,440 a year for single workers and $16,253 for workers with families.18 Including the additional tax that those workers pay on the income they would have paid toward the premium directly, the exclusion effectively threatens workers who fail to enroll in employer-sponsored health insurance their employer offers with average penalties of $6,869 if they are single and $18,223 if they have families.19 A worker who declines her employer’s coverage because she enrolls in coverage through a spouse’s employer often simply absorbs those losses. This dynamic could help explain why “dual-earners may not be aware of the potential trade-off between wages and health benefits.”20

The Functional Equivalent of a Mandate

The tax exclusion has features in common with an individual mandate to purchase health insurance. Under a mandate, the government requires individuals to purchase a specific type of health insurance or pay a penalty. The same is true under the exclusion: either an individual enrolls in a particular type of health insurance that the tax code favors (i.e., employer-sponsored insurance) or she must pay more money to the government. The exclusion and other targeted tax preferences effectively turn the tax code into a mandate mill:

The tax system is … equivalent to a collection of individual mandates, like the one in the Obama health care law, with penalties for Americans who fail to buy insurance … You and your neighbor might have the same income, but if, unlike your neighbor, you fail to have a mortgage or buy as much health insurance, then you have to pay higher taxes.

You may feel very differently about tax deductions … and mandates backed by penalties. Economically, though, they are identical. They yield the same outcomes and provide the same incentives.21

The additional tax that workers must pay on each dollar they receive as cash effectively penalizes them for not spending that income on health insurance.

The exclusion shares features with the individual mandate that Congress created under the Affordable Care Act, or Obamacare. Each gives taxpayers a choice between enrolling in a type of health insurance the government specifies or paying more to the IRS. In both cases, the additional amount a worker must pay to the IRS (i.e., the implicit or explicit penalty) rises with income.

Where the two measures diverge, it is because the exclusion is more coercive. Obamacare permits a wider range of health plan types and sellers. Taxpayers could avoid Obamacare’s penalties by enrolling in any plan available on the individual market or in an employer-sponsored plan. Taxpayers can avoid the exclusion’s penalties only by enrolling in one of the few plans that their employer or their spouse’s employer happens to offer. When workers fail to enroll in employer-sponsored health insurance, the IRS uses fines, liens, and criminal penalties, including prison time, to collect the additional income and payroll taxes those workers must pay. Congress forbade the IRS to use those measures to collect unpaid individual-mandate penalties.

In addition, many taxpayers who were exempt from Obamacare’s explicit penalties have always been subject to the exclusion’s implicit penalties. Obamacare’s mandate exempted religious objectors, undocumented immigrants, indigenous tribes, those who could not afford health insurance, workers with coverage gaps, anyone who the Department of Health and Human Services determines would suffer a “hardship,” and workers who earn too little to file an income-tax return.22 It exempted so many groups, government officials estimated “90% of the nation’s 30 million uninsured won’t pay a penalty.”23

The exclusion’s implicit penalties apply to anyone who pays income or payroll taxes, including five out of six households overall and two-thirds of households in the lowest income quintile.24 “In 2019, 72.5% of nonelderly uninsured workers worked for an employer that did not offer them health benefits.”25 Each of those workers paid the exclusion’s implicit penalties, which are “increasingly unfair to those persons not employed by employers who provide compensation in the favored form.”26 By the time Congress enacted Obamacare’s individual mandate, the U.S. government had already spent decades using a far more severe form of coercion to control workers’ private health insurance choices.

Even so, researchers have traditionally overlooked the exclusion’s coercive character. The OECD did not begin to count private health insurance spending in the United States as compulsory until Obamacare’s individual mandate took effect in 2014. If Obamacare’s individual mandate was coercive enough to render spending on private, nonemployment-based health insurance compulsory, the exclusion is coercive enough to render spending on employment-based coverage compulsory. Indeed, it is plausible that, in combination with other laws that regulate health insurance, the exclusion may cause employer-sponsored health insurance to meet the U.S. Congressional Budget Office’s definition of “an essentially governmental program” (i.e., “tightly controlled by the federal government with little choice available to those who offer and buy health insurance” and without “flexibility in terms of the types, prices, and number of private-sector sellers of insurance available to people”).27

Violating Workers’ Rights

From a normative perspective, using coercion to prevent a worker from making her own health decisions violates her health care rights. The exclusion uses the coercive power of the U.S. tax code to force the worker to surrender her earnings and her health insurance decisions to someone else. To avoid an implicit $7,333 penalty, a worker who is eligible for family coverage must: let her employer control $16,253 of her income, let her employer choose her health insurance, enroll in health insurance that disappears at her employer’s whim or whenever her connection to that employer ends, and pay a further $5,969 for the privilege.

In the aggregate, the exclusion effectively threatens U.S. workers with $352 billion in penalties each year unless they allow employers to control $1 trillion of their earnings. Since workers must also pay an additional $327 billion toward their premiums directly, the exclusion ultimately coerces workers into spending an estimated $1.3 trillion each year according to the government’s preferences.28 That amount is roughly 60 percent more than the share of compulsory U.S. health spending attributable to the next-largest source, the U.S. Medicare program.29 (See Figure 6.) It is equivalent to 29 percent of national health expenditures and 5 percent of U.S. GDP.30 If the U.S. government counted compulsory spending on employer-sponsored health insurance as a tax, it would be the third-largest tax behind individual income taxes and payroll taxes and would raise the U.S. tax-to-GDP ratio from 25.5 percent to 30.5 percent.31 If it were an economy, it would be the 15th largest in the world (just ahead of Mexico).32

Workers Bear the Full Cost of Health Benefits

Public appreciation of the exclusion’s impact suffers from widespread misunderstanding about how much employers pay toward health benefits and who bears the cost of those payments. Economic theory, a growing body of economic research, and mainstream economic opinion all hold that the incidence of employer-sponsored health insurance falls entirely on workers. That is, workers bear the full cost of employer health insurance payments in the form of lower wages. While economists grasp this distinction, they typically discuss the exclusion using terminology that hides this reality from workers and policymakers.

Employer Payments toward Health Benefits

Employer payments toward employee health benefits are substantial. In 2021, average total premiums for employer-provided self-only and family coverage were $7,739 and $22,221, respectively. On average, employers paid $6,440 toward self-only coverage (83 percent of the premium) and $16,253 toward family coverage (72 percent).33 (See Figure 7.) Economywide, employers will pay an estimated $944 billion toward employee health benefits in 2022. Including $327 billion that employees will pay directly, spending on employer-provided health insurance will reach an estimated $1.3 trillion.34

Economic Theory: Workers Bear the Cost of Health Benefits

Economic theory holds that the $1 trillion that employers spend each year on employee health benefits comes from workers, not employers. A competitive labor market pushes employers to pay each worker according to her marginal productivity, or the additional value she adds to the production process.35 Regardless of how much compensation a worker receives as cash versus benefits, it is marginal productivity that determines her overall level of compensation. To the extent a firm offers health benefits, then, it must reduce other forms of compensation. When an employer pays $16,253 toward a worker’s health insurance, her cash wages and other compensation fall by the same amount.

Economic theory therefore implies that even if employers make payments for those health benefits, the cost of those benefits falls not on employers but on workers, because workers see reductions in other forms of compensation. Regardless of who makes the payment, all such funds come from employees.

Empirical Evidence: Workers

Bear the Cost of Health Benefits

Studies have shown the entire cost of employer-sponsored health insurance falls on workers in the form of lower cash wages. According to one study:

the average woman in our sample had to accept about a 20% wage reduction to move from a job that does not provide health insurance to a job that provides health benefits. This translates into an implicit value of health benefits that corresponds to about $4,000 per year (early 1990$). This estimate is very close to independent estimates of the cost of health care received by families with private health insurance coverage, and it is also close to what workers say they would need in a wage increase to voluntarily move from a job that provides health benefits to a job that lacks health benefits.36

Another study found that “male workers between the ages of 25 and 55 … who lose employer-sponsored health insurance are compensated with roughly a 10 to 11 percent increase in wages.”37 When Massachusetts required firms to offer health benefits and pay at least a third of the premium, “full-time workers who gained coverage … earned lower wages than they would have … by $2,812 per year” on average, an amount that “corresponds closely to the average” amount employers paid toward such coverage.38

Other studies have found that labor markets adjust compensation in response to incremental increases in employer-plan premiums. When the medical-malpractice liability system and hospital mergers caused health insurance premiums to rise, workers bore the full cost of those increases in the form of lower wages.39 Labor markets even adjust wages differentially for workers with easily identifiable health-risk factors (e.g., age, sex, obesity) versus workers without those characteristics to compensate for the additional costs the former impose on a firm’s health plan:

- When the government required employer plans to cover maternity care, women of child-bearing age bore the entire cost of the additional coverage. Their wages—and only wages for women of child-bearing age—adjusted downward to compensate for the costs of those benefits.40

- Wages adjust to account for the higher costs of insuring older workers. One study found average annual wage increases are 20 percent lower in firms that offer health insurance than in those that do not.41 This finding implies that firms increasingly divert compensation from wages to health benefits as workers age to pay for the higher cost of insuring older workers.

- Another study found that “in cities where health insurance costs are high, the age/wage profile is flatter, indicating that older workers do pay for their higher health costs in the form of reduced wages” and that “workers who choose family health insurance coverage pay for the added employer costs through reduced wages.”42

- Similarly, “The increased cost of insuring older workers results in their receiving 2.8% lower hourly wages, being 2% less likely to be employed and being 0.7% less likely to have employer-sponsored health insurance.”43

- Wages for obese workers adjust downward to account for the higher cost of insuring them. Obese workers receive lower cash compensation than non-obese workers when firms offer health insurance but not when firms do not offer health insurance: “the incremental health care costs associated with obesity are passed on to obese workers with employer-sponsored health insurance in the form of lower cash wages,” whereas “obese workers without employer-sponsored insurance do not have a wage offset relative to their non-obese counterparts.” Wages even adjust downward more for obese women than obese men, because women “have larger expected medical expenditure differences associated with obesity than male workers.”44

- A study comparing states that mandate that insurers cover diabetes care to states that do not found that “obese people pay for all of their own increased health costs in the form of lower wages, rather than passing them on to employers, insurers, and co-workers.”45

In effect, labor markets produce a form of risk-rating of health insurance premiums. Even when employers assign all workers the same nominal premium, workers with above-average health risks pay more for coverage than low-risk workers because the former accept a greater reduction in their cash compensation.46 With notable precision, supply and demand for labor naturally produce compensation arrangements that place the cost of insuring high-risk workers on those workers themselves.47

Economists are nearly unanimous on the question of whose money employers are spending. In 2018, a recurring survey of health economists found that 93 percent of respondents agreed with the statement, “Workers pay for employer-sponsored health insurance in the form of lower wages or reduced benefits.” Prior versions of the survey found that 92 percent (2012) and 91 percent (2005) of respondents agreed with the statement. Health economists agreed on this statement more than any other question.48 One health economist described the consensus:

Imagine yourself in a bar where a pickpocket takes money out of your wallet and with it buys you a glass of chardonnay. Although you would have preferred a pinot noir, you decide not to look that gift horse in the mouth and thank the stranger profusely for the kindness, assuming he paid for it.… Most economists believe that employer-based health insurance is an analogue of this bar scene.49

Other economists summarize the consensus: “Employees ultimately pay for the health insurance they get through their employer, no matter who writes the check to the insurance company.”50

The economics of labor markets support the normative conclusion that the money employers spend on employee health benefits belongs to workers in the same sense the workers’ cash wages do. Each is compensation that employers agree to provide workers in exchange for their labor. If employers did not offer health benefits, competition for workers would force them to return that $1 trillion to workers as cash wages or other compensation, just as employers who currently do not offer health benefits must offer higher cash wages to remain competitive. Withholding even part of that compensation—in effect, a pay cut—would create a disequilibrium that labor markets would correct by restoring that compensation. When employers spend $1 trillion on health benefits, they are controlling and spending their workers’ earnings on their workers’ behalf. The tax exclusion uses coercion to prevent workers from controlling that money.

Public Misunderstanding

Despite the consensus among economists, many workers do not realize that the money their employers spend on health benefits is their money, and few have any concept of how much of their money employers control. A 2021 poll of U.S. residents found that only a bare majority (51 percent) of respondents knew that employers finance health benefits by reducing wages; 49 percent believed that the money comes from corporate profits, executive compensation, or somewhere else.

Even those who understood that workers bear the full cost of health benefits did not understand how much of workers’ income employers control. Seventy-eight percent of respondents incorrectly believed employers pay less than $16,000 toward family coverage. Ninety-one percent underestimated how much employers pay toward health benefits overall by an order of magnitude.51

The lack of understanding stems in part from the fact that that those funds are largely invisible to workers. Those funds never enter workers’ salaries. Federal law requires employers to disclose how much they spend on health benefits.52 Since workers have no control over those funds, however, they have little incentive to pay attention.

Another cause of public ignorance is that scholars and policymakers use language that obscures the exclusion’s effects and the incidence of employer spending on health benefits. It is common practice to describe the exclusion as an unqualified tax break. That convention glosses over how the exclusion compels workers to let employers control a share of their earnings that is more than twice the amount the workers save in taxes. Policymakers describe the exclusion as a “tax expenditure” or “tax subsidy,” as if the government were giving something to workers. Researchers describe employer payments for health benefits as the “employer portion” of the premium, or the “employer contribution,” and describe what employees pay directly as the “employee portion” or the “employee contribution.”53

These terms are all either inaccurate or misleading. If workers bear the full cost of their health insurance, employers contribute nothing. What employers pay toward health benefits is no more an “employer contribution” than what employers withhold from their employees’ paychecks and send to the IRS as income-tax withholding. These conventions are one reason “workers may not even be aware of how much their total health premium is” or that every penny of the $1.3 trillion they and employers spend each year on health benefits comes from them.54

History of the Tax Treatment of Health Insurance

The tax exclusion has had a dramatic impact on the markets for health insurance and medical care, as well as the U.S. political system. While not the initial or sole force behind the growth in employer-sponsored health insurance, it is likely the primary reason employer-sponsored health insurance came to dominate the market. Its impact on prices for health insurance and medical care have fueled dissatisfaction with the U.S. health sector. Congress has responded to that dissatisfaction by intervening further in those markets. With few exceptions, those interventions have tended to exacerbate the exclusion’s effects.

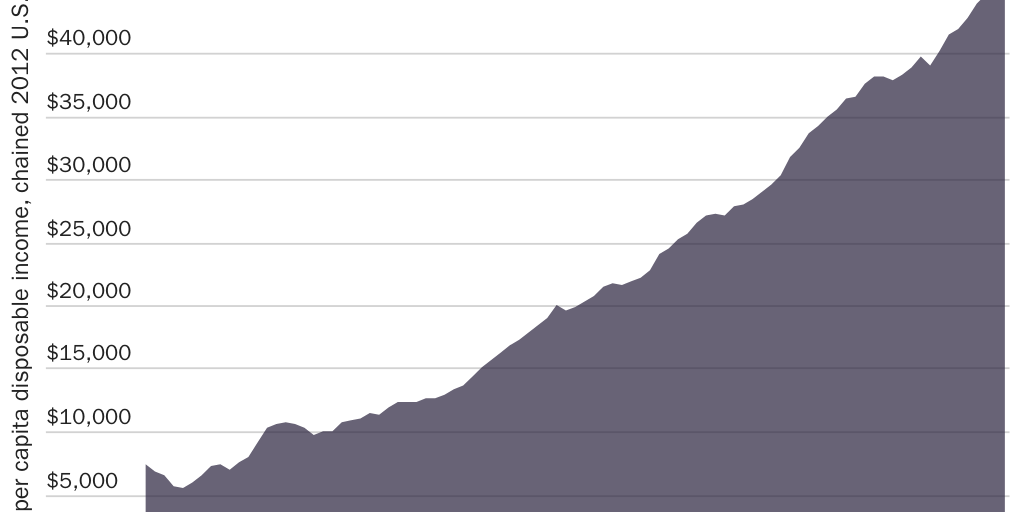

Private health insurance expanded to cover most of the U.S. population over the course of the 20th century. (See Figure 8.) The greatest contributor to this growth was likely rising incomes.55 Real per capita disposable personal income rose from $7,511 in 1939 to $10,860 in 1950 and to $21,584 in 1980.56 (See Figure 9.) As incomes grew, workers wanted to spend more on medicine, which innovation was making more valuable, and to protect their assets by purchasing it via health insurance.57

Rising incomes can explain growth in health insurance across the board (i.e., including health insurance that does not qualify for the exclusion). For example, the years between 1939 and 1951 saw robust growth in both employer-sponsored coverage and health insurance that consumers purchased directly from insurance companies.58 Even when employers facilitated health benefits for their employees, moreover, “employers rarely contributed to premiums during the period when most initial market penetration occurred. Employees opted into coverage individually, and the entire premium was in fact paid by a payroll deduction from the individual’s wages in the great majority of first-generation policies.”59

Indeed, employer purchasing of health insurance during this period was not the norm:

Early Blue Cross and commercial health insurance plans were paid for wholly by employees without help from their employers, although they were usually purchased at the job site on a group basis with employers withholding money from wages to pay premiums. Employers rarely contributed, and indeed, by the end of World War II, less than 10% of Blue Cross premiums were paid by employers.60

Years after World War II ended, employer purchasing of health insurance still was not prevalent. “By the end of 1950 only about 12 percent of Blue Cross’s 35.9 million enrollees received any employer [payment] toward their insurance coverage. Among the 32.3 million enrolled in commercial plans in 1949, only a few large groups received any employer payment, and these [payments] were small.”61

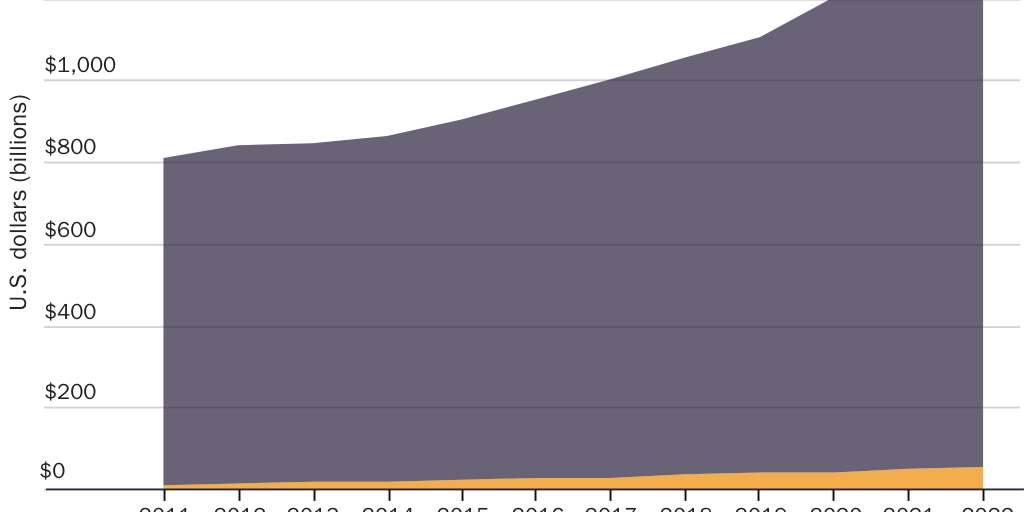

Over time, the exclusion’s implicit penalties steered the market toward arrangements where employers purchased health insurance for their workers with funds that otherwise would have gone to those workers. A 1979 survey found that employers paid part or all of the premium for 93 percent of covered workers.62 Employee health benefits came to consume an increasing share of compensation, growing six-fold as a share of labor income from 1.1 percent in 1962 to 5.8 percent in 2002 and 6.5 percent in 2022.63 (See Figure 10.) By 2019, 56 percent of the U.S. population obtained health insurance through an employer, while only 10 percent obtained it directly from an insurance company.64 Amid ups and downs, the exclusion’s implicit penalties remained substantial for a century. (See Figure 5.)

As the exclusion drove health care prices and health insurance premiums upward, Congress and federal regulators launched further interventions into the health sector, including the creation of new entitlement programs, in the hope of mitigating the exclusion’s negative effects. Rather than address the underlying problem, Congress ended up creating an increasingly complex set of interventions to address problems that the exclusion creates.

How It Started: The Federal Income Tax

When Congress created the current federal income tax in 1913, health insurance was rare and bore little resemblance to products that exist today. “Prior to 1930, most health insurance [only] provided income replacement in the event of disability, illness, or accident” because “lost wages for individual wage earners were about four times as great as medical costs.”65

The tax exclusion was an accident of history. Since few employers provided health benefits at the time, Congress gave no apparent thought to whether to count those benefits as taxable income. “The tax code was actually silent on whether employer-sponsored health insurance was to be considered income subject to federal income taxation.”66 The Treasury Department officials who implemented the new tax had to decide the question.

The issue was less than straightforward.67 For example, “health insurance at the time often included wage continuation payments for periods of illness; since rights for this were forfeited when employment was terminated, it was not clear whether coverage by itself (in contrast to actual receipt of payments) constituted income.”68 Some observers believed that the Treasury could and should have taxed employer payments for health benefits as income to the employee.69

Though early rulings were inconsistent, they suggest the exclusion is as old as the income tax itself.70 A 1954 law review article concludes that the exclusion

merely “crept” into the law. [An early interpretive regulation] revised April 17, 1919 provided that premiums on … health insurance were income to the employees. The provision was later omitted … [In] 1920, a Solicitor’s Law Opinion created the exception by holding that the premiums on group insurance were not paid as compensation but as an investment in group efficiency.71

Other scholars have concluded, “Employer contributions for … health insurance plans were nontaxable in the original income tax in 1913” and that “employer contributions to such arrangements were generally not taxable to the employee.”72 Given that the “modern health insurance developed in the 1930s,” it appears there never was a period when the income tax applied to employer-purchased health insurance.73

The exclusion would have had little impact in 1913 anyway because the marginal tax rates from which it shielded income (and therefore the implicit penalties it creates) were relatively low. By the end of 1913, federal income tax rates ranged from 1 percent on the first $20,000 of annual income to 7 percent on income above $500,000 per year.74 More importantly, “due to exemptions and deductions, less than 1 percent of the population paid income taxes.”75 Marginal income-tax rates soon grew, however. By 1918, the lowest marginal rate was 6 percent and the highest was 77 percent, with 54 marginal rates (or brackets) in between.76 Marginal tax rates have fluctuated since. (See Figure 5.) The federal income tax currently imposes marginal tax rates ranging from 10 percent for low-income earners to 37 percent for high-income earners, with five brackets in between.77

In 1942, the federal government created an additional incentive for employers to purchase health insurance for workers.78 As part of its efforts to wage World War II, the U.S. government froze wages but “ruled that the employer’s provision of pension and health insurance benefits were not subject to wage controls, a policy that reinforced the IRS rule that such benefits were not to be treated as taxable income.”79 While wage controls prevented employers from offering higher cash wages, the exemption for employer-purchased health benefits created an incentive for employers to compete for workers by offering health benefits. Even so, employer purchasing of health benefits was still not prevalent even years after the war ended and did not see robust growth until after the federal government lifted all wage ceilings in 1953 (see the block quote that starts with “Early Blue Cross” in the previous section).80

Prior to 1954, the exclusion existed only by bureaucratic dictate. In that year, Congress codified the exclusion.81 One study found that simply codifying the exclusion “led to a shift from individual to group insurance and increased the amount of health insurance coverage purchased by households, especially households with high marginal tax rates” (whom the exclusion effectively threatens with higher taxes).82

Social Security Increases the Exclusion’s Penalties and Effects

When Congress created Social Security in 1935, it financed the program with a 2 percent tax on payrolls up to $3,000.83 Since then, Congress has repeatedly increased the Social Security tax rate and expanded the tax base. At present, the Social Security payroll tax rate is 12.4 percent and applies to the first $147,000 of wages, leaving workers less able to afford health insurance and medical care.84

Social Security increases the impact of the exclusion. As with the income-tax base, the federal government excluded employer-paid health insurance premiums from the Social Security payroll tax base. The result was that the exclusion shielded income from a higher overall marginal tax rate. Equivalently, Social Security increased the implicit penalties that the exclusion imposes on workers who do not enroll in employer-sponsored health insurance.

As a result, at the same time Social Security helped the elderly obtain medical care by providing them with regular cash subsidies, it also worked against that purpose by increasing the ways the elderly might suffer health care–related financial hardship. By increasing the implicit penalties that the exclusion imposes on workers who purchase health insurance that stays with them through retirement, Social Security increased the likelihood that workers would lose their health insurance upon retirement. By increasing the distortionary effects of the exclusion, including the upward pressure the exclusion exerts on medical prices, Social Security exacerbated the problem of the elderly facing excessive health care prices.

The Medical Expense Deduction Mimics the Exclusion

In 1942, Congress created the medical expense deduction to help taxpayers with high health care spending afford rising health care prices (and to shield them from rising wartime tax rates85). To the extent a taxpayer’s qualified medical expenses (including after-tax payments toward health insurance premiums86) exceed a certain percentage of her income, the taxpayer may deduct those expenses for income-tax purposes. Congress has adjusted that threshold over time.87 It is currently 7.5 percent of adjusted gross income.88

The medical expense deduction does little to restore a worker’s right to control her earnings. For qualified medical expenses above the threshold, it reduces the implicit penalty the exclusion imposes on income the worker controls. A taxpayer does not pay income taxes on that income, but she continues to pay payroll taxes on it. It does not alter the exclusion’s implicit penalties nearly enough to allow her to reclaim control of her income. Only about 6 percent of tax returns claim the medical expense deduction.89

Worse, the medical expense deduction counterproductively puts upward pressure on health care prices. Above the threshold, it effectively penalizes taxpayers for each additional dollar they do not spend on qualified medical expenses. This feature has the effect of increasing demand for medical care and increasing prices, though each effect is likely small relative to the exclusion’s impact.

Medicare Increases the Exclusion’s Penalties

By 1963, U.S. residents aged 65 and older had significantly lower rates of hospital insurance (54 percent) and surgical insurance (45.7 percent) than the overall population (70.3 percent and 65.2 percent, respectively).90 In 1965, Congress created Medicare to help the elderly access medical care. Medicare is both a cause and an effect of the exclusion, as well as a government program that exacerbates the problem it purports to solve.

To a large extent, Congress created Medicare to fix problems that Congress itself created or exacerbated. The income tax and Social Security payroll tax leave workers with less income to purchase and save toward medical expenses in retirement. While the exclusion encourages workers to enroll in health insurance, which should expand access to medical care for workers, it also increases health care prices, which reduced access for workers and seniors.

The exclusion further reduced seniors’ access to care by increasing the likelihood that they would lack health insurance. “Several factors contribute[d] to th[e] lack of coverage among elderly people” in the years leading up to 1965. In particular, “many of these persons who had insurance coverage before retirement were unable to retain the coverage after retirement … because the policy was available to employed persons only.”91 Employment-based coverage was not the only option. “Before the passage of Medicare, many Americans over sixty-five were covered by health insurance policies that were guaranteed renewable for life.” In 1964, there were 72 insurance companies that offered guaranteed-renewable health insurance that covered individuals through retirement and until death.92 By 1965, however, the federal government had spent decades penalizing such coverage in favor of job-based coverage, which dramatically increases the risk of becoming uninsured upon retirement. Part of the reason so many seniors lacked health insurance in 1965 is that government had spent decades penalizing health insurance products that cover seniors.

Rather than fix those problems, Medicare created more.93 Medicare exacerbated the tax exclusion’s effects on consumption. Congress patterned Medicare coverage on existing private health plans. The exclusion’s encouragement of excessive coverage and medical consumption in the private sector therefore led to excessive coverage and spending in Medicare.94

To finance Medicare, Congress imposed an additional payroll tax of 0.7 percent. Congress initially applied the Medicare payroll tax to the same base as Social Security: in 1966, income up to $6,600 per year, excluding employer-purchased health insurance. Congress has since increased the Medicare payroll tax rate and base many times, but the exclusion still applies. The rate is currently 2.9 percent and applies to every dollar of labor income, without limit.95 An additional Medicare tax of 0.9 percent applies to all labor income in excess of $200,000 for individuals and $250,000 for married couples.96

Like the Social Security payroll tax, Medicare’s payroll tax increases workers’ marginal tax rates and thus the exclusion’s implicit penalties. Medicare thus increases the impact of the exclusion, including the penalties it imposes on workers who purchase secure coverage that stays with them into retirement.

Employee Premium Payments Become Eligible for the Exclusion

In 1978, Congress again attempted to fix problems that it had created via the income tax and the exclusion. The exclusion encourages excessive health insurance, excessive medical consumption, and higher health care prices. Congress responded to the resulting rise in health insurance premiums not by eliminating the exclusion but by expanding it.

Initially, only employer premium payments qualified for the exclusion. In 1978, Congress made employee premium payments eligible. Section 125 cafeteria plans that employ “premium conversion” allow employees to exclude from income and payroll taxes the portion of their employer-sponsored health insurance premiums that they pay directly. As of 2011, 80 percent of covered workers had access to premium-conversion plans that shield their premium payments from taxation.97 The share is likely higher today.

Making employee premium payments eligible for the exclusion both reduced taxes on workers with employer-sponsored health insurance and increased the exclusion’s implicit penalties on those who decline employer-sponsored health insurance. Along the way, it encouraged even more excessive insurance and medical consumption and pushed health care prices higher.

Flexible Spending Accounts

Section 125 also allowed employers to offer flexible spending accounts (FSAs). Several different kinds of FSAs exist today. “Health” FSAs make certain out-of-pocket medical expenditures eligible for the exclusion.

Workers can decide how much of their cash wages to devote to a health FSA, up to a limit. In 2022, individual workers could allocate up to $2,850.98 Deposits are eligible for the exclusion. Disbursements for qualified medical expenses are tax-free. In 2020, 46 percent of civilian workers had access to a health FSA.99

FSAs give employees only a small measure of additional control over their incomes. The fact that deposits are eligible for the exclusion gives workers greater control over those funds. But a worker generally forfeits to her employer any FSA funds she does not spend. A worker with a “use-it-or-lose-it” FSA (or alternatively a “grace-period” FSA) forfeits to her employer all unspent FSA funds up to $2,850 at the end of the plan year (2.5 months after the plan year ends). A worker with a “rollover” FSA forfeits all unspent funds in excess of $550.100 In 2019, 37 percent of workers with “grace-period” FSAs forfeited an average $355 of their earnings to their employers; 48 percent of workers with “use-it-or-lose-it” FSAs forfeited an average $341; and 49 percent of workers with “rollover” FSAs surrendered an average $328.101 This feature exacerbates the exclusion’s incentives encouraging excessive medical consumption and low-value care.

Medical and Health Savings Accounts

In 1996, Congress enacted bipartisan legislation allowing 750,000 taxpayers to open tax-free medical savings accounts (MSAs). In 2003, Congress expanded on MSAs by creating tax-free health savings accounts (HSAs). HSAs mitigate the exclusion’s economic distortions by extending the exclusion’s preferential tax treatment to—and, equivalently, reducing the exclusion’s implicit penalties on—a limited amount of health care savings and spending that workers control.

Taxpayers who enroll in qualified health plans can deposit limited amounts into an HSA tax-free. In 2022, qualifying self-only (family) plans must have had deductibles no lower than $1,400 ($2,800) and total cost-sharing no greater than $7,050 ($14,100). An enrollee could deposit up to $3,650 ($7,300) per year. Enrollees aged 55 and over could deposit up to an additional $1,000.102

Funds that employers and employees deposit via payroll deduction qualify for the exclusion just as premium payments do. Otherwise, deposits are deductible only against income taxes. Congress taxes neither growth in HSA balances nor withdrawals for qualified medical expenses. It subjects withdrawals for nonmedical expenses to income taxes plus a 20 percent penalty. The latter penalty disappears when the account holder turns 65, becomes disabled, or dies.103 It is testament to how punitive the exclusion’s penalties are that shielding HSA deposits from them results in greater tax advantages than any other savings vehicle.104

Like any other savings account, HSA funds belong to account holders and move with them from job to job and from health plan to health plan. In 2020, HSA holders contributed $42 billion to their accounts. In effect, this means that HSAs reclaim for workers only about 4 percent of the $1 trillion that Congress coerces workers into letting their employers control. (See Figure 11.) As of mid-2021, 31 million Americans had accumulated a combined $100 billion tax-free in HSAs.105

HSAs reduce the exclusion’s distortions in favor of employer-sponsored health insurance and third-party payment generally. But since HSAs do so by extending the exclusion’s preferential tax treatment to additional uses of income (i.e., to out-of-pocket medical spending and savings for future medical expenditures), they reduce those distortions at the cost of expanding the overall amount of economic distortion the exclusion creates. Since Congress conditions tax-free HSA deposits on enrollment in a specific type of health insurance, moreover, HSAs also present taxpayers with a choice similar to the exclusion or a mandate to purchase health insurance: enroll in a government-defined health insurance plan or pay more to the government.

Health Reimbursement Arrangements

In yet another attempt to provide relief from rising medical prices that the federal government itself exacerbated, in 2002 the Treasury Department created tax-free health reimbursement arrangements (HRAs).106 HRAs created yet another way to extend the exclusion to out-of-pocket medical expenses.

HRAs eliminate the penalty the tax exclusion imposes on earnings that workers control but in a manner that preserves significant employer control over workers’ earnings. An HRA is not a savings account. It is more like a line of credit. The employer does not put money into an account a worker owns. Instead, if an employee incurs qualified expenses, including medical expenses and in some cases health insurance, the employer promises to reimburse her up to a limit. The employee receives no money unless she incurs qualified expenses. HRA reimbursements qualify for the exclusion. Employers decide how much credit to extend, how employees may use it, and whether workers can carry over unspent credit from year to year.

Similar to FSAs, employees generally forfeit any unspent HRA credit when they leave their jobs.107 Again, this use-it-or-lose-it incentive exacerbates the exclusion’s incentives encouraging excessive consumption and low-value care.

The federal government permits different types of HRAs. Traditional HRAs allow employers to reimburse only qualified medical expenses and only for employees who enrolled in health insurance through the firm or their spouse’s employer.108 In 2017, Congress allowed small employers who don’t offer health benefits to offer “qualified small employer” HRAs to employees who elsewhere enroll in Obamacare-compliant coverage.109 In 2022, qualified-small-employer HRAs can reimburse individual workers up to $5,450 per year and families up to $11,050 per year for qualified medical expenses.110

In 2020, the Treasury Department allowed employers to offer “individual coverage” and “excepted benefit” HRAs. Individual-coverage HRAs “extend the tax advantage for traditional group health plans … to HRA reimbursements of individual health insurance premiums” such as Obamacare plans.111 Employees must enroll in health insurance to use these HRAs. In the case of off-Exchange plans, employers can combine individual-coverage HRAs with a premium-conversion option to allow employees to pay more of the premium with excludable income.

Employers who provide health insurance can offer “excepted benefit” HRAs, and employees can use them even if they decline their employer’s coverage.112 Excepted-benefit HRAs can reimburse up to $1,800 in qualified medical expenses (and therefore mimic HSAs) and/or premiums for dental coverage, vision coverage, or short-term, limited duration insurance.113

Health Insurance Tax Credits

Congress has also tried to mitigate the exclusion’s ill effects by creating health insurance tax credits. Where a $1,000 exclusion, deduction, or exemption reduces taxable income by $1,000, and therefore reduces a worker’s tax liability by the product of that amount and her marginal tax rate (on average, $333), a $1,000 tax credit reduces her tax liability by $1,000.

The exclusion increases prices for health insurance and medical care and penalizes workers unless they enroll in coverage that disappears when they change jobs. Rather than fix those problems, tax credits create a new tax preference for health insurance that workers purchase directly from insurance companies. While tax credits may reduce the implicit penalty that the exclusion imposes on nonemployer coverage, they also create new distortions that exacerbate rather than correct the exclusion’s distortions.

In 2002, Congress offered “health coverage tax credits” to a small number of taxpayers who lost their health insurance when they lost their jobs or suffered other hardships. Recipients received a reduction in their tax liability equal to 65 percent of the premium for approved coverage, including individual-market coverage. Congress later increased the credit amount to 80 percent and then reduced it to 72.5 percent. In 2018, fewer than 19,000 households claimed the credit.114 After many extensions, the credit expired on December 31, 2021.

Featured Event

In 2014, the IRS began offering “premium assistance tax credits” to enrollees who purchase Obamacare coverage through an Exchange. In 2022, more than 11 million Obamacare enrollees will have received $75 billion in tax credits.115 In many cases, Obamacare’s tax credits can cover the enrollee’s entire premium.

Both types of credit are “refundable.” Refundable tax credits are not tax breaks at all but instead a government spending program. If the amount of a refundable tax credit exceeds the recipient’s tax liability, the government pays the recipient the balance. Obamacare’s tax credits are almost entirely government spending. Just 15 percent of Obamacare’s tax credits represent a reduction in recipients’ tax liabilities. The remaining 85 percent is government spending (i.e., a burden on other taxpayers).116

Health insurance tax credits do not eliminate the exclusion’s economic distortions. In some ways, they exacerbate them. Obamacare’s tax credits encourage excessive coverage, medical spending, and prices by requiring recipients to enroll in more comprehensive coverage than many would choose on their own or than they would obtain through an employer. To the extent that Congress must raise marginal tax rates to finance the spending inherent in refundable tax credits (or to offset the revenue loss from the nonrefundable portion of the credit), health insurance tax credits exacerbate the effects of the exclusion much like Social Security and Medicare do. Tax credits even create entirely new distortions. The amount of Obamacare’s credits falls as a taxpayer’s income rises, which creates a disincentive for workers to climb the economic ladder.

Finally, to the extent health insurance tax credits offer tax relief, they present the same choice as the exclusion or a mandate to purchase health insurance. Eligible taxpayers may either enroll in a government-defined health insurance plan or pay more money to the IRS. A health insurance tax credit “is essentially a mandate to purchase health insurance, with the cost of violating the mandate equal to the value of refundable credit.”117

The Cadillac Tax

Economists warn that the exclusion encourages workers to demand and employers to provide excessive levels of health benefits. In 2010, Congress attempted to reform the exclusion with a new tax on overly comprehensive “Cadillac” plans. The “Cadillac tax” was a 40 percent tax on employer-sponsored health insurance premiums that exceeded certain thresholds.118 It would have mitigated some of the exclusion’s effects, but in some cases, it would have replaced the implicit penalty on worker-controlled health care dollars with an implicit penalty on employer-paid health premiums.

In 2022, the Cadillac tax would have applied to premiums in excess of $11,200 for self-only coverage and $30,150 for family coverage. Below those thresholds, the tax code would have continued to penalize workers for every dollar of compensation that they took as cash instead of health benefits. Above the thresholds, the tax would have had different effects depending on the worker’s marginal tax rate. For workers whose marginal tax rates exceeded 40 percent, it would have reduced but not eliminated the exclusion’s implicit penalty. For those with marginal tax rates below 40 percent, it would have flipped the script by imposing an implicit penalty on each additional dollar that workers allocate to health benefits versus cash wages.

Economic efficiency requires equalizing the tax treatment of health benefits and other forms of compensation. The Cadillac tax would have substituted one economic distortion for another. As a straight tax increase, the Cadillac tax sparked considerable political resistance. Congress repeatedly delayed its effective date and then repealed the tax in 2019.119

Harmful Effects of the Exclusion

The tax exclusion creates distortions across and within economic sectors that dramatically reduce social welfare. By redirecting $1 trillion of health spending each year from the workers who earned it to their employers, the exclusion has altered incentives in the health sector. Those distorted incentives have made health insurance and medical care less affordable and have had a negative impact on quality.

The exclusion creates distortions across economic sectors by artificially lowering the after-tax price of employer-sponsored health insurance—and thereby of medical care—relative to other types of health insurance and to nonmedical consumption. It distorts the financial sector by annually shunting $1.3 trillion of workers’ earnings directly to insurance companies, employers, and benefits managers and preventing savings institutions from competing to manage those funds. Previous work suggests that by encouraging excessive medical consumption, the exclusion creates a deadweight economic loss on the order of 19.2 percent of total spending on employer-sponsored health insurance.120 In 2022, that amounted to roughly $245 billion, or 1 percent of GDP.121

The tax exclusion distorts labor markets. It distorts the makeup of compensation packages in favor of health benefits over cash wages. It denies workers a clear measure of how the market values their labor by obscuring their total compensation. It distorts how workers sort themselves into jobs: “those who potentially would buy family coverage tend to sort themselves into jobs based on preferences for health insurance.”122 It encourages part-time work where firms and workers might prefer full-time arrangements: “as the costs of benefits rise, firms and workers have an incentive to move from full-time jobs with benefits to part-time jobs without.”123 It locks workers into jobs for fear of losing their health insurance.124 One study found that the exclusion “reduces voluntary job turnover by 20% per year.”125 It distorts competition and entry by favoring large employers over their smaller competitors. It makes discrimination against older, female, and obese workers appear worse than it is. (See the “Empirical Evidence: Workers Bear the Cost of Health Benefits” section.)

The exclusion distorts the markets for health insurance and medical care. It penalizes secure, portable coverage that consumers purchase directly from insurance companies in favor of employer-sponsored coverage. It encourages excessive levels of insurance. One study estimated that simply codifying the exclusion in 1954 “increased the amount of coverage purchased by 9.5 percent.”126 By insulating consumers from medical prices, it encourages excessive medical consumption, excessive health care spending, excessive prices, opaque prices, and price discrimination.127

Harvard economist Martin Feldstein explained how the tax exclusion fuels excessive health insurance and health care prices: “The spread of insurance causes higher prices and more sophisticated services which in turn cause a further increase in insurance. People spend more on health because they are insured and buy more insurance because of the high cost of health care.”128 Writing with Bernard Friedman, Feldstein continued: “Because the growth of insurance has been the primary cause of the exceptional rise in health care prices, it can with justice be said that the tax [exclusion] has been responsible for much of the health care crisis.”129

Among the exclusion’s costs is that it reduces choice and innovation in health care financing and delivery. Some scholars argue that employers don’t even try to pick the best health plan for their employees but instead “select a plan that is acceptable to the CEO’s family—a stratagem known as ‘CEO’s Partner’s Plan’ … to limit complaints from the [CEO’s] partner.”130 One study estimates “the average ‘welfare loss’ attributable to the mismatch between group and individual purchases … may actually be in the neighborhood of 5–10 percent, about equal to the estimated difference in loading between the nongroup and small-group insurance markets.”131 Since “most employers lock their employees into traditional FFS without a choice and without an opportunity to keep the savings if they choose a more economical system,” the exclusion distorts workers’ choices by encouraging fee-for-service payment and fragmented delivery of medical care at the expense of other payment systems (e.g., prepayment) and delivery systems (e.g., integrated health systems and coordinated care).132

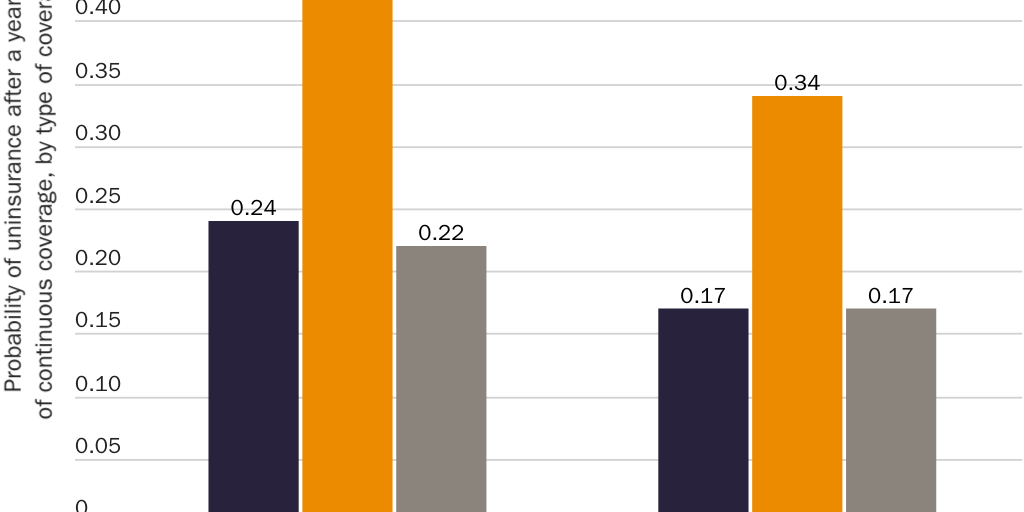

At the same time the exclusion encourages health insurance policies to cover a broader range of services and providers than consumers would purchase on their own, it penalizes health insurance products that cover a broader range of risks. Americans change jobs on average a dozen times by age 54.133 Health insurance policies that consumers purchase directly from insurance companies on the individual market are portable. They do not automatically disappear when the policyholder changes jobs. Individual-market coverage therefore insures against a risk that employment-based coverage does not: the risk of needing expensive medical care after an employment separation. One study found that patients in poor health were roughly twice as likely to end up uninsured if they had obtained insurance from a small employer versus purchasing it directly from an insurer.134 (See Figure 12.) The tax exclusion penalizes policies that insure against this risk and inhibits innovative insurance products that would protect against even more risks.135

The exclusion made workers more vulnerable to COVID-19 in at least three ways. First, it ties health insurance to employment, which “is one of the many ways the U.S. health care system has made us so much more vulnerable to the effects of the pandemic than other countries. In other countries, you don’t hear about people losing health insurance when they lose their jobs.”136 Between February and June 2020, approximately 7.3 million Americans unnecessarily lost their health insurance when government lockdown orders and changes in consumption patterns caused them to lose their jobs. Millions more lost jobs and coverage in subsequent months.137 Second, the exclusion encouraged the sickest, most vulnerable workers to return to work because they feared losing their coverage, thereby putting them at higher risk for contracting COVID-19.138 Third, when those newly uninsured workers and COVID-19 patients needed medical care, they had to face the excessive health care prices that the exclusion generates.

The tax exclusion reaches deep into workers’ lives. It distorts marriage markets by increasing the cost of ending unhealthy unions. According to one study, “because employers will remain the main source of coverage for the nonelderly population, marital disruption is likely to continue to lead to substantial instability in insurance coverage.”139

Finally, the exclusion distorts the political system. It has created problems that have led Congress to intervene in the health sector again and again. It has led some participants in the political process to argue that not taxing employer-sponsored insurance is a “subsidy” or a gift from government. It leads those who benefit from the exclusion (e.g., large employers, unions, health insurers, health care providers) to spend vast resources blocking proposals that would return control of those funds to workers.

End the Exclusion Now

Congress should eliminate all targeted tax preferences—equivalently, implicit penalties—that coerce workers into devoting income to what Congress values rather than what they value. The benefits of eliminating the exclusion include returning control of more than $1 trillion annually to the workers who earned it, better economic performance, and a health sector that makes medical care better, more affordable, and more secure. Educating the public on the benefits of eliminating the exclusion will expand the range of politically feasible options.

A $1 Trillion Effective Tax Cut

The tax exclusion denies workers control of $1 trillion of their earnings each year. Regardless of whether those dollars flow into government coffers, one may fairly describe this effect of the exclusion as an alternative type of tax, because it uses government coercion to deny workers control of a sizable portion of their income. Eliminating or reforming the exclusion in a manner that returns those funds to workers would therefore be akin to a large effective tax cut.

Removing the tax differential that penalizes workers if they demand that compensation as cash would allow workers to control those funds. Economic theory holds that to the extent employers stopped offering health benefits, they would return those funds to workers as additional cash wages or other compensation. On average, a worker with employer-sponsored family coverage would gain control of an additional $16,253 of her earnings each year, with which she could make her own health insurance decisions.

Workers would still benefit even if employers did not cash out all workers fully or immediately. One study estimates that the benefits of being able to choose one’s health plan are so great that “the median employee would be willing to forego 16 percent of her employer [premium payment] simply for the right to use what remains toward a plan of her choosing.”140 If workers wished to remain in their employer-sponsored plans, they would be free to do so. Workers’ needs, not government dictate, would decide where those funds go.

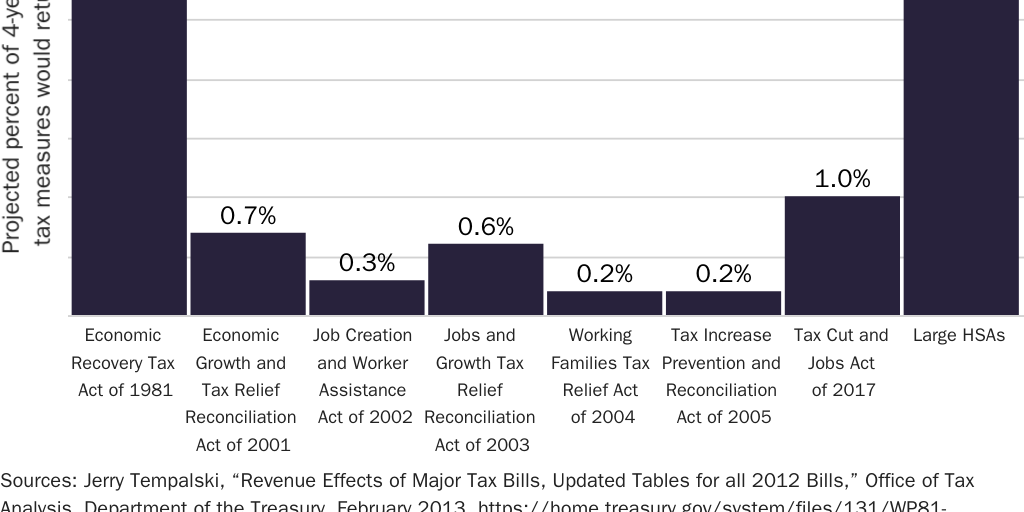

By allowing workers to control $1 trillion of their earnings that they currently do not control, reform of the exclusion would amount to a $1 trillion effective tax cut. As a share of the economy, this effective tax cut would be larger than the tax cuts that Congress enacted in 1981 and any tax cut since. (See Figure 13.) The sooner reform can put that $1 trillion in the hands of workers, the more politically feasible it will be.

A Better Economy

Eliminating the tax exclusion would also improve economic performance. In particular, by eliminating the exclusion’s incentives to purchase excessive coverage, reform would lead workers to choose less comprehensive coverage and to consume less wasteful medical care.141 The reduction in these expenditures would enable workers to purchase goods and services that they value more. “American families are in general overinsured against health expenses. If insurance coverage were reduced, the utility loss from increased risk would be more than outweighed by the gain due to lower prices and the reduced purchase of excess care.”142

Reform of the exclusion is essential to realizing those gains in consumer welfare. “Large reductions in spending will not actually be achieved without fundamental changes in the financing and delivery of health care. The government can spur those changes … by significantly limiting the current tax [exclusion] for health insurance.”143