Now that the Senate has decided to avoid the pesky issue of calling witnesses in an impeachment trial, Congress will get back (after the break) to legislative business, and the first order of business will be President Joe Biden’s $1.9 trillion (with a T) “American Rescue Plan.” Congress got the ball rolling on the plan when both chambers passed a 2021 budget resolution instructing various committees to come up with their respective pieces of a final bill that would include up to $1.9 trillion in new spending and revenue loss (tax cuts). Those bills were released late last week, so this will not be a deep dive into every little detail (thank goodness). Instead, today we’ll focus on the bigger picture, including the debate that’s erupted about the plan’s size, timing, and effects, and try to answer one simple question: “what, exactly, are we rescuing here?”

What We’ve Done So Far

Before we get to that, however, it’s important to understand the pandemic-related actions that the U.S. government—the Federal Reserve, Congress, and the Trump administration—has authorized since last spring. For that purpose, I recommend this useful tracker by the Committee for a Responsible Federal Budget (CRFB), which allows you to play with various elements to see the billions (and billions) of dollars that have already been authorized and disbursed to fight COVID-19 and support ailing individuals and entities. I’ve expanded a few categories in the following table for ease of reference, but invite you to head over there and click around yourself:

As the chart shows, Congress has already appropriated about $4.1 trillion total to fight COVID-19, but so far only (only!) about $3 trillion has been spent. That number should climb in the coming weeks, however, as more funds are distributed. (There are also trillions more available through the Fed, if needed.) Second, Congress has already provided about $2.5 trillion directly to individuals (income support and direct payments) and businesses (most of the loan programs). To help you get an idea of how the individual help might shake out, I asked CRBP’s Marc Goldwein (who is a great follow on Twitter for all things budgetary) to run through two random scenarios to show that—contrary to the conventional wisdom—Congress has been quite generous so far:

As a result of these initiatives and the recession, the federal deficit has unsurprisingly skyrocketed:

And the near-term fiscal outlook—as explained by my Cato colleagues Jeff Miron and Erin Partin—is pretty dire:

A new report from the nonpartisan Congressional Budget Office (CBO) projects a $2.3 trillion budget deficit in 2021. This is $900 billion less than the 2020 deficit, but as a percentage of GDP it is still the second largest since World War II. In addition, the report states that the national debt will reach 102 percent of GDP this year and rise to 107 percent by 2031—an all‐time record.

They add that the CBO’s projected deficits after 2021 have shrunk a bit due to faster-than-expected economic growth. However, these rosy projections omit three big things: They don’t include Biden’s $1.9 trillion plan; they assume that a host of tax cuts will expire as scheduled (they rarely do); and they assume that future appropriations will track inflation instead of economic growth (they usually track the latter). As helpfully calculated by the CRFB, accounting for these factors—all of which are likely—makes the fiscal situation look a lot worse than what the CBO just predicted:

Where the Economy Is Right Now

Past government efforts, regardless of their generosity and fiscal impact, certainly don’t mean that more government assistance is unnecessary, but figuring what is necessary requires an honest assessment of the economy today. And here, I think, is where the massive Biden plan starts to falter, because this simply isn’t April 2020. In particular, the United States economy over the last year (1) has experienced a “K‑shaped” recovery in which growth overall has resumed (it was a good-not-great 4 percent in the fourth quarter of 2020) and large segments of workers and businesses are doing pretty well, but millions of others are still struggling mightily; and (2) appears primed for a serious (but uncertain) breakout once COVID-19 is under control.

On the former issue, industry surveys show continued weakness in the businesses—such as leisure/hospitality, restaurants, and brick-and-mortar retail—still experiencing reduced traffic due to local lockdowns or consumer reluctance, but better (if not strong) activity in less-affected services and manufacturing. As of early February, “strong consumer- and business demand are helping to offset the weakness of consumer-facing services, which are holding back overall economic growth.” This disparate activity has affected the job market in a similar way, as the following example shows:

(For a detailed look at the various labor market gyrations, I highly recommend this detailed Wall Street Journal analysis.)

It’s not just industries that have recovered differently from the pandemic: There is also a significant divergence in the fortunes of U.S. workers, with lower wage jobs still struggling but higher wage jobs at or above pre-pandemic levels due primarily to the prevalence of remote work:

On the bright side, that same research shows that “most of the gaps across demographic groups have narrowed considerably during the recovery, particularly as jobs have been added in the hardest-hit sectors”:

Because many workers are even getting raises right now, our two-tier labor market has led to the bizarre situation in which “Americans as a whole are now earning the same amount in wages and salaries that they did before the virus struck — even with nearly 9 million fewer people working.”

On the latter issue (where the economy is headed), there is ample evidence that U.S. economic activity should expand significantly when the pandemic finally wanes later this year (hopefully). For starters, the pandemic’s shock to global supply chains has caused a “once-in-a-lifetime drain on inventories, from retail to manufacturing and wholesale distribution,” and refilling those stockpiles will goose business activity for quite a while (indeed, it’s already started).

Perhaps more importantly, U.S. consumers are poised to spend—and spend heavily—once they can. Beyond the wage gains already noted, personal savings rates have exploded over the last year—thanks to consumers being unable to buy typical services (vacations, meals, manicures, etc.) and higher disposable income from government transfers (“which the federal government finances by borrowing”):

Many other Americans—including many making between $25,000-$74,999—are also in a better financial position today than they were before the pandemic began, having paid down student loans or credit cards with their stimulus checks. Thus, as one recent industry analyst noted when explaining the spike in U.S. lumber prices, “Household balance sheets are pretty spectacular right now.”

It’s very likely that consumers will eventually come off the sidelines in a big way and help many ailing businesses and workers in the process—the big question is when (though it may already be starting). While economic growth forecasts for the first half of the year are decent (between 2 percent and 5 percent), most experts believe that continued employment gains and a consumer/business spending spree should cause growth to be quite strong in the second half of 2021, regardless of any stimulus (though these same folks uniformly expect some government action). This outlook, of course, depends on the virus continuing to recede throughout 2021, due to a combination of vaccines, mitigation measures, and infection-related immunity.

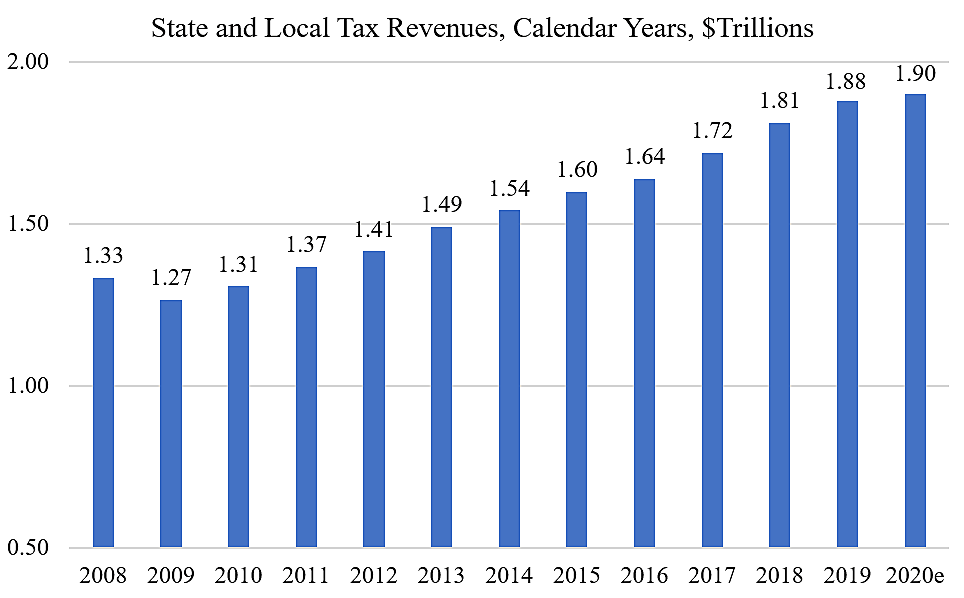

Finally, it’s important to note that the state and local government funding “crisis” never materialized, though the impacts again vary widely by state. Overall, Cato’s Chris Edwards notes that state and local tax revenues were actually up in 2020 and should increase even further in 2021 in line with the aforementioned economic growth:

{kind=link}

A state-by-state breakdown, moreover, shows only a handful of states in bad shape (shown in dark orange in the chart, primarily states that rely on sales taxes for revenue):

Thus, while the economy certainly isn’t in 2019 shape, it’s only still horrible for a discrete share of workers, companies and state/local governments and has plenty of post-pandemic upside without more government help.

What the Biden Plan Would Do

Unfortunately, the House reconciliation bill seems to ignore most of the points above. Instead of targeted relief to the individuals and entities who most need it (something even we libertarians can support), the legislation is a buffet of “relief,” “stimulus,” longstanding Democratic Party priorities, and good ol’ fashioned pork. The New York Times has a great summary of the House bill’s main pieces and how it compares to the Republican counteroffer:

Buried in here, of course, are all sorts of details—far too many for one newsletter (especially since many analyses are still in progress). But here, I think, are a few key issues:

Is This Relief? There is little doubt that millions of individuals and entities still need help, but the House plan provides extremely generous benefits to millions more. For example, it would send households another $1,400 per person (including dependents) in direct payments to individuals making up to $75,000 per year or couples making up to $150,000, with sums phasing out up to $100,000/$200,000. Thus, it would provide thousands of dollars to millions of people who are hardly “poor” and who may have experienced little to no financial hardship. But hey, free money, right?

Even for workers who have been hit, the plan’s significant extension and expansion of supplemental unemployment insurance—from $300 a week to $400 a week—could lead to government compensation that far exceeds a worker’s lost income, thus potentially discouraging him or her to return to work even when conditions allow for it. According to a rough estimate from American Action Forum, in fact, around 50 percent of eligible workers would make more on unemployment under a $400 per week federal benefit than at work. (Others estimate an even higher percentage.) This, of course, depends on the generosity of each state’s unemployment program and its overall economic/virus situation, but it unquestionably goes beyond mere “relief”—especially when combined with other parts of the Democrats’ bill, such as the expansion of the child tax credit (CTC).

Indeed, using the two scenarios above, Goldwein reran the numbers with the additional relief that Democrats have proposed and shows that our two (very sympathetic) families would not just be made whole but actually come out way ahead:

Other Democratic proposals appear similarly overbroad. For example, the Biden plan provides a whopping $525 billion in aid to state and local governments, even though (a) the vast majority of states are doing just fine; (b) billions in previous federal government support have still not been disbursed to these entities; and (c) there are much better, more targeted ways to help the few states that really need it. (Even supporters of more state aid think the package is way too big.)

Furthermore, the House relief bill contains a whole host of provisions that reflect not near-term emergency “rescue” priorities (e.g., business/family relief or public health/vaccine funds) or even long-term government investments (e.g., infrastructure) but longstanding progressive socioeconomic priorities and handouts to favored interest groups. Perhaps most egregiously, the bill bails out mismanaged multiemployer pensions, undermining “years of bipartisan good-faith negotiation to responsibly address the issue” and providing no reforms to prevent the problem from recurring in the future. (Hooray, moral hazard!) Given that the House reconciliation instructions capped the Ways and Means Committee’s disbursements at $941 billion, inclusion of this pension bailout forced the committee to cut a month of unemployment benefits from Biden’s initial plan. That’s just ridiculous.

Other questionable provisions include funds for “environmental justice,” Affordable Care Act (Obamacare) and Medicaid expansions, and a host of “temporary” provisions on taxes and other progressive priorities that have little to do with COVID-19. (A $15/hour federal minimum wage proposal is also included but is expected to be dropped.)

Or Is This Stimulus? Supporters of the package counter the aforementioned concerns by noting that this package, contrary to its branding, is really more about broad, long-term fiscal stimulus than it is about targeted relief. But this claim also runs into problems. For starters, even if you buy into the stimulus argument (more on that another time), the $1.9 trillion price tag could far exceed the amount needed to get U.S. economic growth back on track:

Currently the economy is below full employment—GDP is below potential GDP, and the difference between the two is called the “output gap.” In the theory, above, stimulus plus the multiplier effects is supposed to close the output gap. According to the CBO estimates, the output gap is a bit above $650 billion. According to the administration and Hill Democrats, a stimulus of $1.9 trillion—three times the size of the output gap—is needed to get the economy back to pre-pandemic shape.

If this were true, then the stimulus “multiplier effect”—the number of dollars of economic growth generated by one dollar of stimulus—would be well under 1 (the bare minimum for stimulus efficacy). That’s a pretty bad deal for taxpayers and the economy more broadly.

If, on the other hand, the multiplier is higher, then much less stimulus would be needed to close the output gap. This remains true even if the multiplier remains way under 1 and the output gap is much larger than what the CBO estimates. The following chart from the CRFB shows various multiplier scenarios (including one from the Brookings Institution):

In all cases, the stimulus goes way beyond merely closing the “output gap.”

Now, several people—including some on the right—say that the Great Recession taught us that it’s better for government stimulus to overshoot than undershoot, but this ignores (1) that the pandemic recession is likely different—in cause, effect, and duration—than the deeper, more systemic Great Recession (see, e.g., this new paper from Michael Strain and Jay Shambaugh on the latter); (2) that the $4.1 trillion in authorized pandemic recession fiscal support has already doubled the fiscal policy responses (about $1.8 trillion) to the Great Recession; (3) that Federal Reserve actions during the pandemic recession have also been, in the words of Chairman Jerome Powell, “unprecedented”; and (4) that overshooting the output gap by two- or three-fold carries its own risks.

This recent Wall Street Journal piece hits at the first three points (and provides some ammo for the fourth):

Investors’ near-insatiable demand for even the riskiest corporate debt is fueling a Wall Street lending boom, offering lifelines for struggling companies even as the coronavirus pandemic still drags on the economy. … The most striking aspect of the current lending boom is its timing. Typically, it can take years after recessions for the market to reach its present level of exuberance, analysts said. In this case, it has taken less than 12 months and has arrived just as economic data has revealed a winter slowdown in the recovery.

Debt investors are hardly alone in their enthusiasm. Investors across a range of asset classes have poured money into risky wagers, even as the frenzy around videogame company GameStop Corp. and other popular stocks for individuals calms. Commodities such as oil and copper have surged lately, and more than $58 billion went into mutual and exchange-traded funds tracking global stocks during the week ended Wednesday, the largest such inflow on record, according to a Bank of America analysis of data from EPFR Global.

Investors’ optimism rests largely on the idea that current economic challenges aren’t normal and can be resolved quickly once coronavirus vaccines are more widely distributed. The combined efforts of the Federal Reserve and Congress have also helped by depressing benchmark interest rates and pumping trillions of dollars into the economy,

This is not your father’s (older brother’s?) recession.

The risks of adding even more fiscal stimulus to the current market have even some left-leaning economists, such as former Treasury Secretary Larry Summers, former chair of the Obama’s Council of Economic Advisers Jason Furman and former IMF chief economist Olivier Blanchard urging caution (if not outright opposition to the stimulus package as written). In particular, they and other experts warn that even more front-loaded stimulus, plus the aforementioned economic conditions (consumer spending, etc.), could spark a serious bout of inflation, thus triggering a harsh response from the Federal Reserve (higher interest rates, monetary “tightening”), and possibly causing another painful recession.

As the New York Times Neil Irwin explains, these risks aren’t certain to materialize—inflation has been subdued for years, the bond market isn’t freaking out (yet), and Powell has said he’s willing to tolerate a near-term spike in prices without raising rates—but the truth is that nobody knows what will happen, and it’s important to understand the tradeoffs and very real potential downside risks. Nobody seems to want to do that.

(Markets, for what it’s worth, are starting to expect higher inflation.)

Even assuming that inflation and overheating (and a painful Fed response) don’t come to pass, other pragmatic and ideological risks warrant consideration. First, there’s the risk that a gargantuan, poorly targeted, partisan package now will imperil future federal relief efforts regardless of the conditions on the ground later this year. The economy’s looking up, but there’s still a ton of uncertainty out there. But ramming through another $1.9 trillion right now could mean that federal relief is absent in, say, fall 2021 even though certain localities, companies, or workers are still reeling—and previous (again, poorly targeted) relief didn’t fully compensate them. This is particularly a concern since other non-COVID items, such as that ridiculous pension bailout, cause supplemental unemployment benefits to end much sooner than they might be needed.

Second, the package could exacerbate the United States’ deepening fiscal problems. As Miron explains in a new research paper, the United States’ fiscal situation is unsustainable in the long term not because of temporary COVID-19 spending but because of runaway entitlement spending. However, the additional deficit spending could be a drag on future economic growth (as the very respectable Penn-Wharton Budget team expects) and long-term fiscal pressure would arise to the extent that the American Rescue Plan’s “temporary” spending ends up being not-so-temporary at all.

And there’s the final risk: that much of this “temporary” spending becomes permanent, thus leading to a long-term expansion of size and scope of the federal government. (Yes, I understand this won’t upset some of my left-leaning readers, but—c’mon—you knew what you were getting into when you signed up.) Once a certain government program and/or spending level is established, political inertia (and baseline budgeting) makes repeal or reform extremely difficult, as new constituencies are established and any “cuts”—no matter the size, effect or historical context—are deemed heartless, draconian Social Darwinism (or whatever). As Milton Friedman once observed, “nothing is so permanent as a temporary government program,” and history is littered with examples proving him right.

But, hey, no need to take my libertarian word for it. CNN’s John Harwood reported on Sunday that this is precisely the Democrats’ plan:

“There’s more Democratic unity than ever on taking bold steps on an economic dignity compact,” said Gene Sperling, who authored a 2020 book on that subject after working for both previous Democratic presidents. “(It’s) possible for 2021 to be one of the greatest years of progressive accomplishment in the past century.”

In a capital accustomed to legislative gridlock, the scale of Biden’s opportunity has largely escaped notice. That’s partly because those economic provisions in emergency legislation to combat the coronavirus pandemic are drafted to be only temporary.

But Biden and fellow Democrats don’t intend them to be temporary. … Like Republicans with tax cuts, Democrats will count on the looming expiration “cliff” to persuade Congress to extend those temporary benefits for low-income families when the time comes.

Maybe you think this type of long-term change is a good thing, but we should all at least be clear about what’s really going on here—and it certainly isn’t just emergency “rescue” relief for those still reeling from the pandemic.

* * *

P.S. In case you’re wondering what I’d do, (a) I’ve supported (and continue to support) direct cash transfers to individuals since March, but obviously the target group is now narrower; and (b) beyond that, this CRFB provides, I think, some very sane and nonpartisan guidelines. I’m not optimistic that Congress will listen.

About the Author