State legislators should

-

avoid creating any preferential tax treatment for health insurance or medical care; and

-

eliminate existing tax preferences for health insurance and medical care while reducing the overall tax burden.

Congress should

-

avoid creating health insurance tax credits or any other preferential tax treatment for health insurance or medical care;

-

replace all existing health-related tax preferences with an income- and payroll-tax exclusion for “large” health savings accounts; and subsequently

-

adopt a new tax system that reduces tax rates by eliminating all tax preferences for particular forms of consumption.

One of the most far-reaching and damaging ways that government intervenes in the health sector of the economy is through tax laws. The U.S. government taxes incomes and payrolls. Many state governments tax incomes. In each case, governments exempt certain health-related uses of income from taxation. Treating health and nonhealth consumption differently under the tax code effectively penalizes taxpayers who do not spend their money on the goods and services government favors.

State and federal policymakers should eliminate all such targeted tax preferences, which have done enormous harm to consumers and patients. If government must tax incomes, it should tax all income equally.

The imperative of eliminating targeted tax preferences has bedeviled policymakers for decades. The best politically feasible option is to expand tax-free health savings accounts (HSAs).

The Tax Exclusion for Employer-Sponsored Health Insurance

By far the largest of these tax preferences is the exclusion from the federal income and payroll tax bases of employer-sponsored health insurance benefits. Workers who receive income from an employer in the form of health insurance pay no income or payroll tax on the money the employer pays toward the premium. Under so-called Section 125 plans, many workers pay no tax on the portion of the premium they pay, either. Federal and state governments exclude that spending from the income and payroll tax bases.

As a result of the tax exclusion for employer-sponsored health insurance, federal and state tax codes effectively penalize workers who choose not to enroll in employer-sponsored health insurance. Workers who do not enroll in such plans pay higher taxes than workers who do. If two jobs offer equivalent total compensation but one offers health coverage and the other offers higher cash wages, the tax code effectively penalizes the worker who chooses the job that offers higher cash wages. In 2021, the average annual premium for employer-sponsored family coverage was $22,221 (of which the employer pays $16,253 and the worker pays $5,969). Assuming a marginal tax rate of 33 percent, the tax code effectively penalizes the worker $7,333 for taking the second job. The additional income and payroll taxes the worker must pay are the functional equivalent of a penalty for making the “wrong” choice.

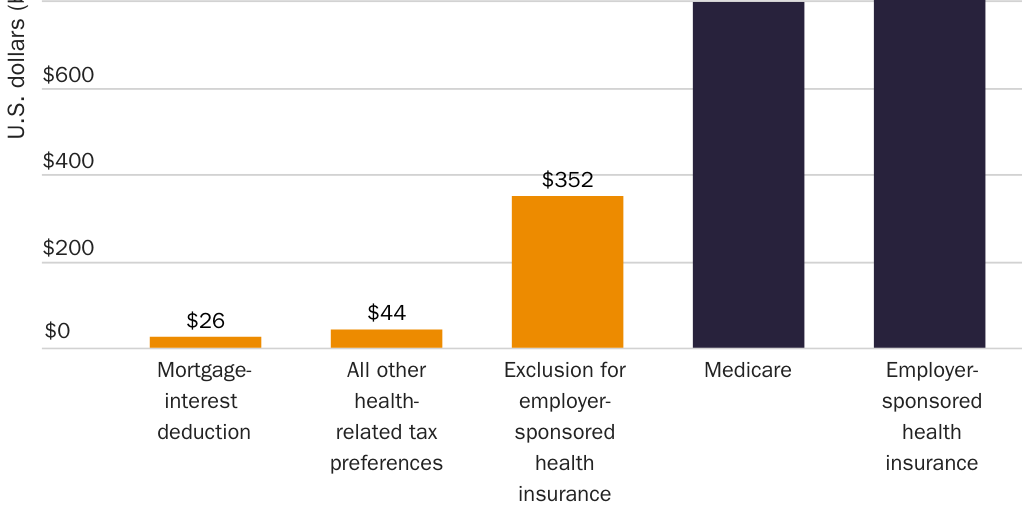

Economy-wide, employers and workers will spend $1.3 trillion on employee health benefits in 2022. Employers will pay $944 billion on their workers’ behalf; workers will pay $327 billion directly. If all workers declined their health benefits, they would retain that $327 billion and a competitive labor market would return the remaining $944 billion to them. The tax code would then treat all $1.3 trillion as taxable income and force workers to pay roughly an additional $352 billion in taxes, effectively penalizing workers for not allowing their employers to control $1.3 trillion of their earnings and their health insurance decisions.

Policymakers and scholars describe the exclusion as a tax break. It is more accurate and useful to recognize that it turns income and payroll taxes into an implicit penalty on workers who do not (a) surrender control of a sizable portion of their earnings to an employer; (b) enroll in a health plan that their employers choose, control, and revoke upon separation; and (c) pay the balance of the premium directly. Those implicit penalties collectively deny workers control of $1 trillion of their earnings per year.

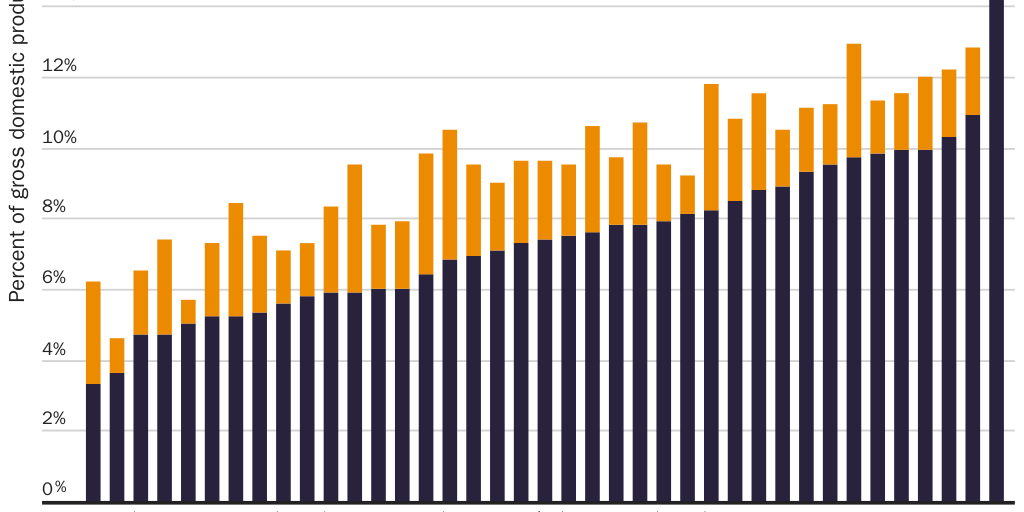

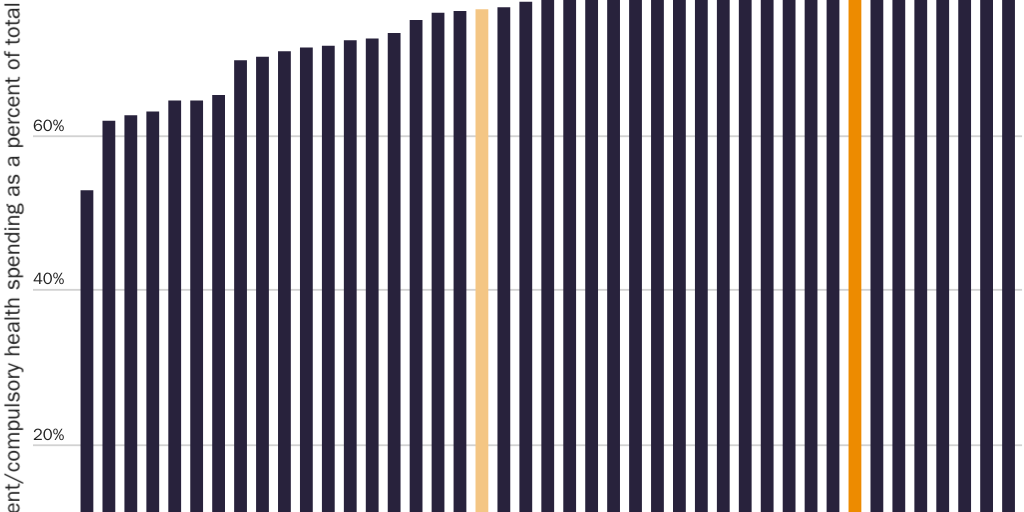

The tax exclusion for employer-sponsored health insurance is the largest source of compulsory spending in the United States, larger than the federal Medicare program (see Figure 1). It is the principal reason why the United States ranks far and away the highest among advanced nations in compulsory health spending as a share of GDP (see Figure 2) and eighth highest among advanced nations in compulsory health spending as a share of total health spending (see Figure 3), why 56 percent of the U.S. population obtains health insurance through an employer, and why only 10 percent obtain it directly from an insurance company.

Harms of the Tax Exclusion

The exclusion does enormous harm to consumers and patients. It generates excessive prices, premiums, and preexisting conditions. It restricts consumer choice: 80 percent of covered workers have only one or two plan types from which to choose. It inhibits wage growth and improvements in health care quality. It makes workers more vulnerable to public-health crises. It reduces economic productivity on the order of 1 percent of GDP each year.

The exclusion leaves many workers who should and could have had secure health insurance coverage with uninsured and uninsurable preexisting conditions. The average worker changes jobs a dozen times by age 52. Health insurance that consumers purchase directly from an insurance company covers the policyholder between jobs and into retirement. In 1964, “many Americans over sixty-five were covered by health insurance policies that were guaranteed renewable for life” because more than 70 insurance companies offered such coverage.

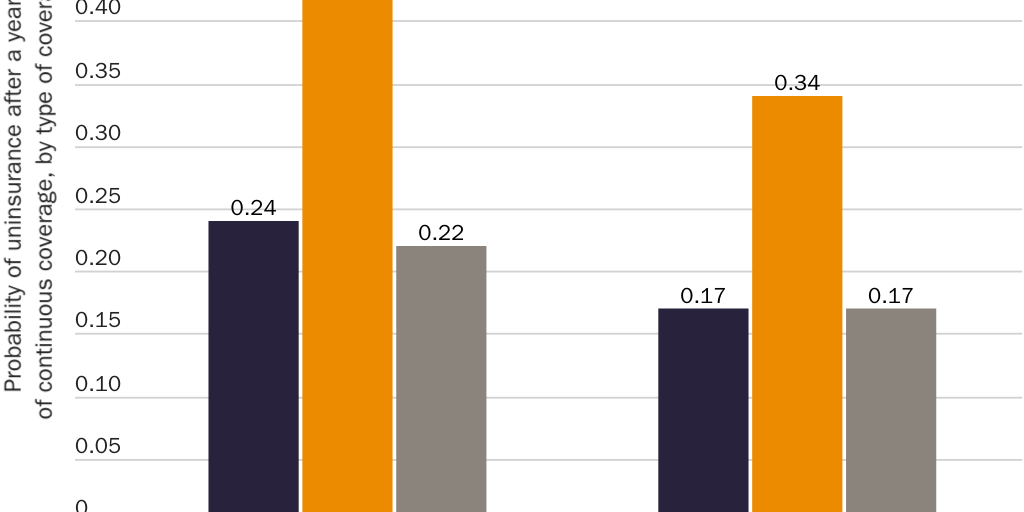

The exclusion penalizes workers unless they enroll in health insurance that automatically disappears when they quit their job, lose their job, keep their job but lose their benefits, lose a spouse to divorce or death, age off a parent’s plan, retire, or become too sick to work. The exclusion thus strips workers of their coverage after they develop an expensive medical condition. Workers in poor health are roughly twice as likely to end up with no insurance if they obtained coverage from a small employer versus purchasing it themselves (see Figure 4). In 1964, the elderly had lower rates of health insurance than the overall population. A principal reason was “many … who had insurance coverage before retirement were unable to retain the coverage after retirement … because the policy was available to employed persons only.” For decades, the tax code has literally penalized workers who choose more-secure health insurance.

Economists Martin Feldstein and Bernard Friedman write, “It can with justice be said that the tax [exclusion] has been responsible for much of the health care crisis.”

One Mistake That Launched Hundreds More

The exclusion has prompted Congress to intervene in the health sector again and again to mitigate its harmful effects.

- In 1965, Congress created Medicare largely to help seniors whom the exclusion stripped of their insurance. Since Congress based Medicare coverage on the (excessive) coverage employers offered, the exclusion indirectly increased the cost of Medicare. (Meanwhile, Medicare’s ever-rising payroll tax increased the exclusion’s impact by increasing its implicit penalties.)

- Also in 1965, Congress created Medicaid to help patients who could not afford the excessive prices that were the result of the exclusion.

- In 1973, Congress passed the Health Maintenance Organization (HMO) Act to subsidize and require certain employers to offer health plans that the exclusion discourages.

- In 1974, Congress enacted the National Health Planning and Resources Development Act, which encouraged states to enact “certificate of need” laws to curb the excessive health spending the exclusion encourages.

- In 1978, Congress made employee payments toward employer-plan premiums eligible for the exclusion—thereby trying to make health insurance affordable by expanding a policy that makes it more expensive.

- In 1985, Congress enacted the Consolidated Omnibus Budget Reconciliation Act (COBRA) to aid workers whom the exclusion strips of their coverage.

- In 1996, Congress enacted the Health Insurance Portability and Accountability Act (HIPAA) to help those who lose the coverage the exclusion forced them to take.

- In 1997, Congress created the State Children’s Health Insurance Program (SCHIP) to aid families for whom the exclusion made coverage too expensive.

- In 2009, Congress enacted the Health Information Technology for Economic and Clinical Health (HITECH) Act to encourage electronic medical records, which the exclusion discourages.

- In 2010, Congress passed the Patient Protection and Affordable Care Act (Obamacare) to aid patients whom the exclusion leaves with uninsurable preexisting conditions.

- In 2020, Congress passed the No Surprises Act to discourage surprise medical bills, which the exclusion encourages.

Since creating Medicare, Medicaid, SCHIP, and Obamacare, Congress has continuously expanded each to aid those who cannot afford health insurance or medical care at the excessive prices the exclusion generates. Federal antitrust authorities have repeatedly taken action against market consolidation that the exclusion encourages. Congress has enacted countless other pieces of legislation to counteract the exclusion’s cost-increasing and quality-suppressing effects. Rather than resolve the situation, each of these efforts makes the exclusion’s underlying problems worse.

Congress has also expanded the exclusion with various spending or savings vehicles that allow workers to purchase medical care tax-free. One of those vehicles—tax-free HSAs—creates an opportunity to return to workers control of the $1 trillion of their earnings that the exclusion denies them.

Reforming the Tax Exclusion with Large HSAs

Individuals have a right to choose for themselves whether, where, and how much health insurance and medical care to purchase without government penalizing them. The tax system should offer no special tax breaks or penalties for health-related expenditures or any other type of consumption.

The best way to eliminate tax-based distortions of workers’ health care decisions is to eliminate income and payroll taxes, which have done enormous harm to workers. Barring that, federal lawmakers should eliminate the exclusion for employer-sponsored insurance and other health-related tax preferences. Those options do not appear politically feasible at present. The repeal of the “Cadillac tax,” which would have merely limited the exclusion, suggests workers will resist reforms that merely eliminate health-related tax breaks.

The best politically feasible way to reform the tax treatment of health care is by changing the current exclusion into an exclusion for larger, more flexible HSAs.

HSAs enable workers to save money for their health care expenses tax-free. At present, employer contributions to a worker’s HSA enjoy the same tax-free status as employer-paid insurance premiums. As a result, workers do not have to surrender those earnings to their employer to avoid the exclusion’s implicit penalties. Taxpayers can also make tax-preferred contributions themselves. Account holders can use HSA funds to purchase qualified medical expenses, tax-free, from any source. HSA funds belong to the individual, follow the individual from job to job, and grow tax-free.

Still, HSAs enable workers to control only a small portion of the dollars and decisions that tax laws allow employers to control. HSAs create tax parity only for the funds that account holders contribute to the HSA to cover out-of-pocket medical expenses. If workers want to purchase their own health insurance, generally they must still pay the premiums with after-tax dollars. Only consumers with insurance that meets Congress’s rigid definition of a “qualified high-deductible health plan” can make tax-free HSA deposits. HSAs are small comfort to workers whose employer doesn’t offer them, or who dislike the one narrow type of health plan Congress permits HSA holders to obtain.

Nevertheless, HSAs present an opportunity to enact reforms that would make health care better, more affordable, and more secure. Congress should take these steps to expand HSAs:

- eliminate all other health-related tax preferences;

- apply the tax exclusion for employer-sponsored health insurance solely to funds that individuals or employers contribute to an HSA;

- increase HSA contribution limits dramatically, from $3,650 for individuals and $7,300 for families to (say) $9,000 for individuals and $18,000 for families;

- remove the requirement that HSA holders obtain a qualified high-deductible health plan, or any health plan; and

- allow HSA holders to purchase health insurance, of any type and from any source, tax-free with HSA funds.

Replacing all existing health-related tax preferences with one tax break for “large” HSAs would limit the exclusion and all tax-based distortions of the health sector. It would free workers to choose their doctor and their health plans without penalty.

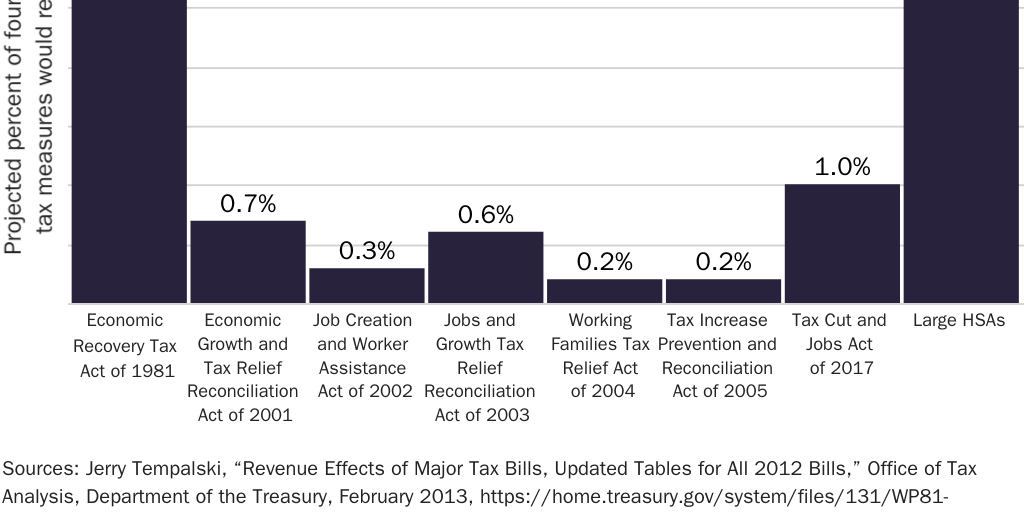

Large HSAs would minimize political resistance to reform. First, rather than increase taxes as the Cadillac tax did, large HSAs would give all workers an effective tax cut. Even if large HSAs were revenue neutral, and even though some workers whose prior health benefits spending exceeded the higher contribution limits would face a higher explicit tax liability, nearly all workers would receive an effective tax cut because they would get to control a large portion of their income that their employer currently controls. Workers with family coverage would gain control of an average $16,253 that they currently do not. That effective tax cut would swamp any additional tax liability that some workers might pay. Economy-wide, large HSAs would allow workers to gain control of $1 trillion of their earnings each year. Large HSAs are the only reform that includes a mechanism to return those earnings to workers immediately. They would return to workers a larger share of GDP than even the Reagan tax cuts of 1981 (see Figure 5). Second, workers and employers who like their current health insurance arrangements could keep them.

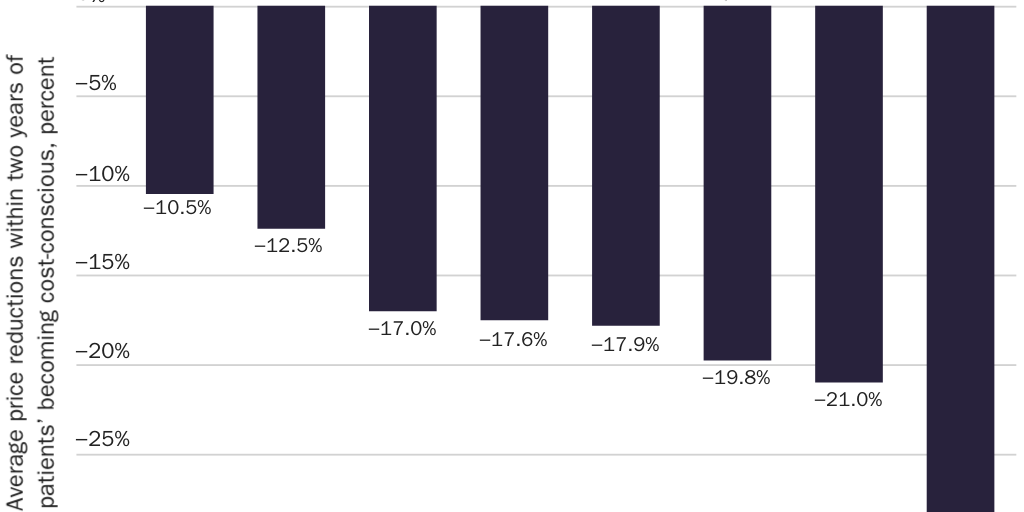

Large HSAs would reduce barriers to innovative insurance products. Workers could choose any health plan they like and would become cost-conscious when shopping for insurance in a way they have never been. This dynamic would eliminate the tax code’s barriers to prepaid group plans and thereby bring innovations like comparative-effectiveness research, electronic medical records, and coordinated care within the reach of hundreds of millions of Americans. The change would drive down prices by encouraging the growth of retail clinics and removing barriers to reverse deductibles, which have saved consumers thousands of dollars on medical procedures (see Figure 6). Large HSAs could change the politics of health care by making consumers more conscious of the costs of government regulation.

Endgame: Tax Neutrality for Health Care

Large HSAs would facilitate the transition to a tax system that contains no special preferences—exclusions, deductions, exemptions, or credits—for health care or any other form of consumption. They would allow such fundamental tax reform to proceed in two steps. First, they would give workers immediate control of the $1 trillion that employers now spend on their workers’ behalf. All other reforms of the exclusion create uncertainty about what will become of those funds. Large HSAs eliminate that uncertainty by immediately delivering those funds to workers. Second, once workers control those funds, Congress could enact fundamental reform without the obstacle of consumers’ anxieties about whether they will be able to keep their health insurance or whether employers will return to them what is rightfully theirs. With large HSAs, it would be far easier for Congress to transition to a flat, fair, or national sales tax.

The tax exclusion for employer-sponsored health insurance is why the United States does not have, and never has had, a private or voluntary or market-based health insurance system. The United States will not have a consumer‐centered health sector until workers control the $1.3 trillion of their earnings that the exclusion now lets employers control.

Congress should act immediately to eliminate the exclusion. At a minimum, it should reduce the harms that the exclusion causes by taking serious steps to reform it. Replacing the exclusion with large HSAs is the best politically feasible option.

Suggested Readings

Abelson, Reed. “UnitedHealth to Insure the Right to Insurance.” New York Times, December 2, 2008.

Cannon, Michael F. “End the Tax Exclusion for Employer-Sponsored Health Insurance.” Cato Institute Policy Analysis no. 928, May 24, 2022.

———. “Health Care’s Future Is So Bright, I Gotta Wear Shades.” Willamette Law Review 51, no. 4 (2015): 559–71.

———. “Large Health Savings Accounts: A Step toward Tax Neutrality for Health Care. ” Forum for Health Economics & Policy 11, no. 2 (2008): 1–29.

Cochrane, John H. “Health-Status Insurance: How Markets Can Provide Health Security.” Cato Institute Policy Analysis no. 633, February 18, 2009.

Herring, Bradley, and Mark V. Pauly. “Incentive-Compatible Guaranteed Renewable Health Insurance Premiums.” Journal of Health Economics 25, no. 3 (2006): 395–417.

Pauly, Mark V., and Robert D. Lieberthal. “How Risky Is Individual Health Insurance?” Health Affairs 27, no. 3 (2008): 242–49.

Silver, Charles, and David Hyman. Overcharged: Why Americans Pay Too Much for Health Care. Washington: Cato Institute, 2018.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.