Congress should

-

repeal all legislation and regulations that mandate public disclosures relating to the purchase and sale of securities;

-

replace those laws, if necessary, only with disclosure requirements that have been shown to actually promote price discovery or deter fraud without undue cost;

-

support initial public offerings by limiting disclosure obligations and promoting innovation in offering types;

-

open all private offerings to investment from any investor regardless of wealth; and

-

create a de minimis exemption for any offering of less than $500,000.

The world benefits from the innovations brought to market by the companies that develop new medical treatments, safety features, communication technologies, and other products and services that make modern life as safe and comfortable as it is. These companies, both in the United States and abroad, rely on the U.S. capital markets to fund their work. Capital markets exist to funnel resources to their best use. When functioning properly, the markets ensure that companies with the best ideas and best business models will attract the most resources.

Regulation, however, can snarl these processes, leading companies to waste resources in complying with inefficient or even counterproductive rules. During the roughly 100 years since the introduction of government-directed securities regulation, the securities laws and implementing rules have needlessly encumbered and often profoundly distorted the proper functioning of the capital markets. Those who advocate for increased regulation typically invoke the need for improved “investor protection” or, since the 2008 financial crisis, “financial stability.” But many of the existing rules, at best, have no bearing on investor protection and, at worst, harm investors by limiting the amount of risk (which includes the opportunity for gain) they may take on. Even rules that may promote investor protection are rarely evaluated to determine the harm they may pose to the greater society. Such rules may be reducing the ability of companies to bring lifesaving products to market or limiting growth, leading to lower employment levels and impaired economic growth.

Existing regulation of registered securities should be dramatically pared back. Ideally, each exchange would set the rules for what disclosures are required for listed securities. Investors interested in the kind of protection afforded by mandated disclosures could restrict themselves to investing in the securities on the exchanges whose rules they find best meet their needs. To the extent federally mandated disclosures continue, the information required should be only the minimum needed to deter fraud and promote price discovery. No disclosure should be required unless the benefit it imparts outweighs the burden it places on all parties. Recommendations for specific regulatory reform follow; however, the entire disclosure structure is ripe for overhaul.

Halt the Expansion of the Current Disclosure Regime

The federal securities laws are a disclosure regime. Instead of requiring that offerings be approved by the Securities and Exchange Commission (SEC) as “fair, just, and equitable to the investor,” as many state-level “merit review” regimes require, the Securities Act of 1933 and the Securities Exchange Act of 1934 require only that issuers provide certain disclosures to the public as part of registering an offering for public sale. The scope of these disclosures has long been understood to encompass information necessary for investors to value securities, primarily a company’s financial performance and information about its business. These disclosures are generally limited to material information—information for which there exists “a substantial likelihood that the disclosure … would have been viewed by the reasonable investor as having significantly altered the ‘total mix’ of information made available.”

In recent years, though, public companies’ mandatory disclosures have expanded, at times serving as vehicles to promote policy goals wholly unrelated to the original purpose of these disclosures. That sets a dangerous precedent. Congress should repeal rules currently in place and commit to enacting no future legislation with similar rules.

Notably, the 2010 Dodd-Frank Act included rulemaking requirements related to policy goals beyond the traditional ambit of the securities laws. The most notorious, the “conflict minerals” rule, mandates that public companies disclose whether certain minerals used in their products were sourced from specific geographic areas. The motivation behind the disclosure was, according to the SEC, congressional “concerns that the exploitation and trade of conflict minerals by armed groups is helping to finance conflict in the [Democratic Republic of the Congo] and is contributing to an emergency humanitarian crisis.” A second, similarly misguided new rule requires public companies to disclose the ratio of the chief executive’s pay to that of the company’s average worker. Whatever the merits of these policy aims, they stray far from the securities regulatory framework of providing information relevant to price discovery and are outside the SEC’s expertise.

In the years since Dodd-Frank, the calls for mandatory public disclosure of a wide variety of information have multiplied and intensified as environmental, social, and governance (ESG) investing has gained steam. ESG, which is shorthand for a number of investment strategies or theories, refers generally to taking into account a company’s environmental, social, and governance factors when making an investment decision. Although many companies voluntarily disclose ESG factors, the SEC is considering mandating disclosures from companies on issues ranging from climate change and workforce diversity to corporate political contributions and beyond.

Such disclosure requirements present two problems. The first and most pressing is that, if the SEC’s disclosure regime becomes entirely untethered from its original, price-discovery function, it can be bent to any purpose at all. Americans should feel secure that any disclosures the government requires are carefully cabined to encompass only that information directly related to the legislation’s initial intent.

Second, these disclosures often have unintended consequences, particularly where the purpose of the disclosure is to drive non-securities-related policy change. In addition, any disclosure by a public company carries the risk of litigation if the statement is found to be either false or missing key information, a risk that is heightened when the information required to be disclosed is qualitative or subject to evolving views about its usefulness.

Congress should clearly delineate the scope of disclosures that the SEC may require, tying them tightly to information relevant to a company’s prospects for financial success as originally contemplated by the 1933 and 1934 acts and preventing the SEC from enacting most ESG-related disclosures. It should also repeal those sections of Dodd-Frank that directed the SEC to promulgate the conflict minerals and pay-ratio disclosure rules and direct the SEC to repeal the relevant implementing regulations.

Streamline IPO Process

The U.S. capital markets are the envy of the world. But over the past 20 years, fewer companies have gone public, and those that have done so have tended to be well past their high-growth phases.

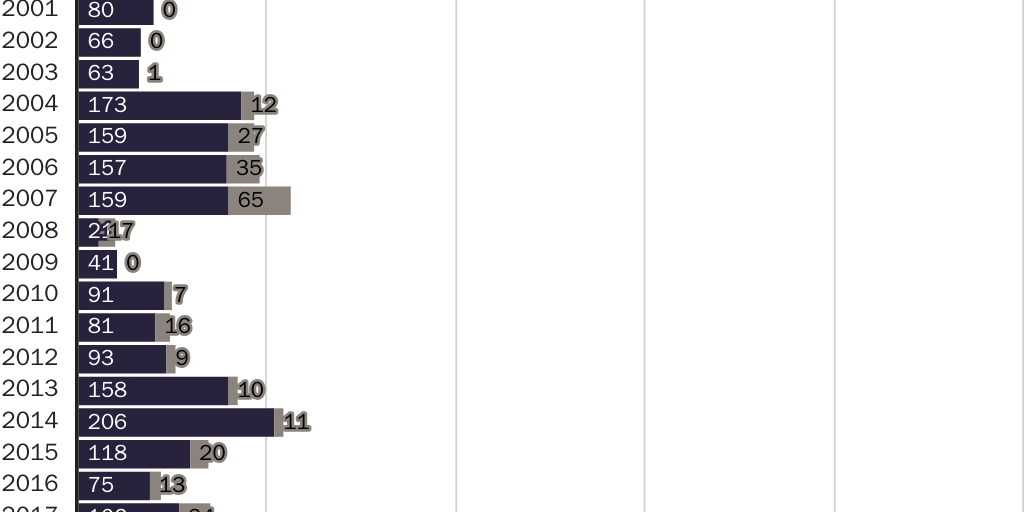

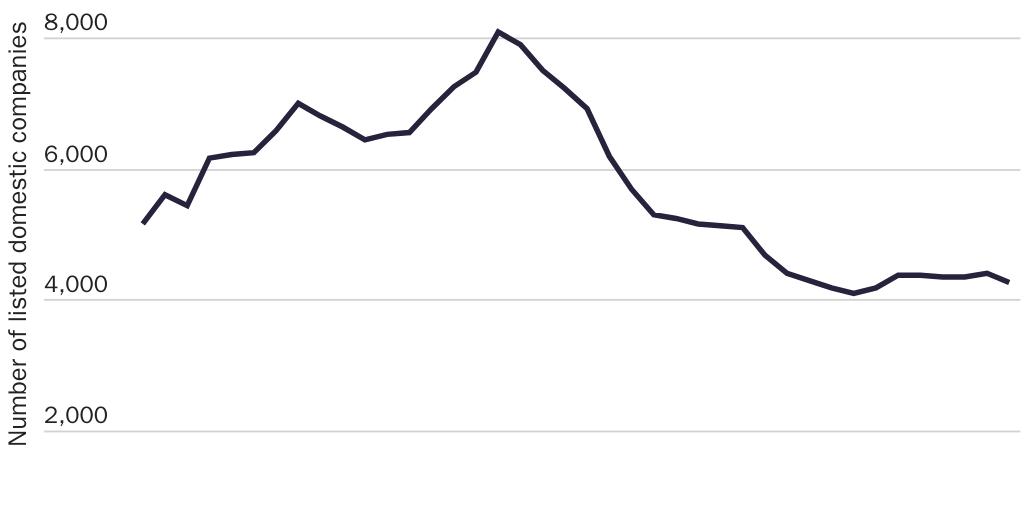

Beginning in 2000, the number of companies opting to go public was in steep decline. Although the number of initial public offerings (IPOs) has recently been more robust—in large part due to special-purpose acquisition companies (SPACs) raising money with the intention of merging with private companies—there are still far fewer public companies today than in years past (see Figures 1 and 2). Because private investments are limited principally to institutions and wealthy individuals, the decline in public companies contributes to wealth inequality by allowing only the wealthy to share directly in yet-to-be-public companies’ most explosive early growth.

Importantly, the IPO decline has not been caused by negative factors alone. For example, accessing private investment has become easier since the 2012 passage of the Jumpstart Our Business Startups (JOBS) Act. The capital raised through private offerings dwarfs the amounts raised through public (i.e., registered) offerings (see Figure 3). But the drop in IPOs cannot be attributed solely to companies freely choosing to raise only private capital.

Corporate leaders express frustration at both real and perceived burdens imposed on public firms, and scholars commonly cite increased regulation as a reason for the decline in IPOs. Decreasing the number and type of mandated public disclosures, as previously described, should alleviate some of these burdens. But the IPO process itself presents unique challenges to private companies that would otherwise choose to become public, including substantial burdens in time and money, heightened liability, and inefficient pricing for the securities they offer to the public.

IPO activity has recently been increasing, and while it remains to be seen if that increase will be sustained, at least some portion of that increase is due to recent innovations in the path to public listing. A large part of the increase has been driven by the popularity of SPACs. A SPAC raises money through an IPO with the intention of completing a merger with a private company, which then assumes the SPAC’s place as a publicly traded company––a particularly attractive option for private companies that have capital-raising needs pinned on technological advancement or other innovations. Although the SPAC boom is unlikely to provide a path to public listing for as many private companies as there are SPACs, it is indicative of the fact that the IPO process creates burdensome hurdles for private companies that would otherwise want to be public.

Direct listings—another recent innovation—have contributed to increased public listings on a smaller scale. This path permits companies to list directly on an exchange without engaging an underwriter; it has been viewed as attractive by providing cost savings to the listing company, by allowing companies to achieve more efficient pricing for their listed shares, and by permitting early investors an easier path to earning a return on their investment.

Although some aspects of the IPO process are governed by tradition, rather than mandatory legal requirements, supporting alternative paths to public listing is important to permit competition that drives changes to the traditional IPO process. It also implements the securities disclosure regime, which does not endorse any particular path or method for public listing. Efforts to conform these innovations to the existing traditional IPO process—either through interpretation or regulation—should be opposed.

Enticing more companies to pursue public listing will provide more choices to investors, and ensuring that companies can do so before they have passed their high-growth phases will create more opportunities for wealth creation among retail investors.

Open Private Offerings to All Investors

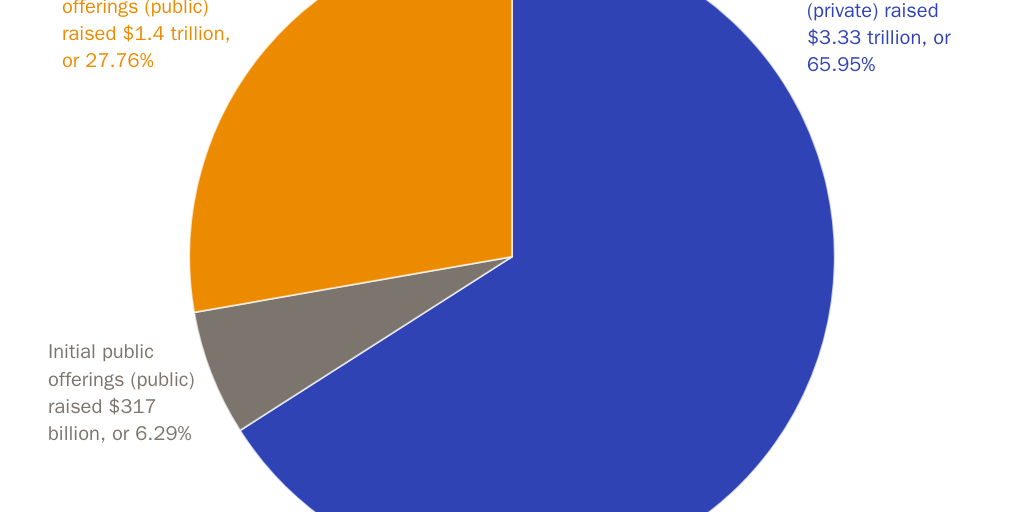

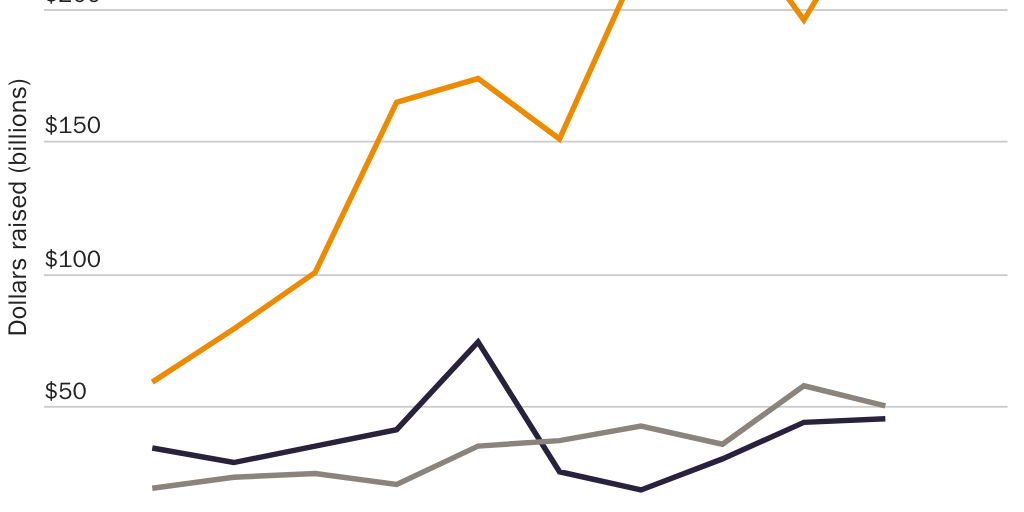

Private offerings have become increasingly popular with issuers and investors alike (see Figure 4). In fact, far more capital is raised in private offerings than by IPOs; for example, between July 1, 2020, and June 30, 2021, IPOs raised approximately $317 billion, whereas private offerings raised more than $3.2 trillion.

Private offerings are characterized by their lack of required disclosures, making them both cheaper to issue and less transparent to competitors. Most are offered under Regulation D, a 1982 regulation that exempts private offerings from state-level registration requirements. More than $1.9 trillion was raised through Regulation D offerings between July 1, 2020, and June 30, 2021.

Participation in most private offerings is restricted to certain “accredited” investors. Currently, only individuals with more than $200,000 in annual income (or $300,000 jointly with a spouse) or assets in excess of $1 million excluding primary residence, and certain institutions, may invest directly in private offerings. The rule was recently amended to permit a limited number of individuals who hold certain securities licenses to invest in these offerings without regard to their income or assets.

The focus on the individual investor’s wealth has created a regime in which investors are arbitrarily barred from investing in certain offerings. The focus on wealth does not protect investors from fraud but rather from losses that they purportedly cannot afford. Making the SEC the judge of who is and is not fit to invest subverts the federal securities laws’ disclosure regime that permits making any offering to the public if the issuer provides the right disclosures.

In addition, these restrictions—especially when paired with reduced IPO volume and longer waits for companies to tap the public markets—can exacerbate wealth inequalities by limiting investment opportunities in potentially higher-growth enterprises. These restrictions also dampen growth in small businesses by limiting the pool of investors available to entrepreneurs; that effect is borne disproportionately by would-be entrepreneurs in less wealthy communities, both minority and rural, who have fewer opportunities to recruit investors from their own communities.

Congress should open investment in private offerings to all investors. It could require that anyone offering securities in a private offering disclose to potential investors that the offering is private and that it therefore lacks the protections afforded by public offerings. Investors could then choose for themselves whether to invest only in public offerings—if they prefer the protections in the 1933 and 1934 acts—or in more loosely regulated private offerings.

Exempt Family and Friends Offerings

Although past guidance recommended a consideration of all facts surrounding an offering to determine whether it is “public,” this understanding has largely faded. Regulation D and its predecessors helped cement the notion that whether an offering is public or private turns principally on whether or not the investors are rich. The absurd result is that even a tiny offering to a tiny group of investors who are close personal friends and relatives of the issuer’s executives may still be deemed a “public” offering, requiring registration. These offerings—in which an aspiring restaurateur or a couple of friends building an app ask their parents, cousins, and good friends to “go in on” the enterprise with the hope of getting “a cut of the profits” down the road—still happen, however. And they happen without registration, often without the issuer ever understanding that the transaction being proposed is in fact a sale of securities.

It is arguably within the SEC’s authority to deem such offerings exempt, either as nonpublic offerings or through its authority to exempt “any class of securities … if it finds that the enforcement of [the registration requirements of the Securities Act] with respect to such securities is not necessary in the public interest and for the protection of investors by reason of the small amount involved or the limited character of the public offering.” The SEC has not, however, used this authority to provide such an exemption and considers these offerings to be in violation of the securities laws.

It is unclear, however, why the SEC should be involved with extremely small offerings, especially if those offerings are made exclusively to friends and family. Because few issuers are even aware that their actions are governed by securities laws, the current proscriptions do little to prevent such offerings. Instead, they only complicate the process when an issuer grows and moves on to more formal methods of raising capital, often resulting in having to unwind those early investments.

A better solution would be for Congress to enact an explicit de minimis exemption. The exemption could include a cap, for example $500,000, on the amount raised. This type of exemption would free the offerings that have already happened, and will continue to happen, of legal encumbrance, allowing entrepreneurs to focus on building the business and ensuring that their friends’ and families’ investments are sound ones.

Conclusion

Capital markets direct the flow of resources to enterprises. Ideally, these resources flow freely, attracted to the companies that will put them to best use based on the needs and wants of consumers. Regulation functions like rocks in a stream, redirecting the flow. Too much regulation—especially regulation implemented without regard to its effects—risks choking the flow of capital entirely or artificially flooding one area of the economy while leaving another dry. The trend toward ever more regulation in the financial sector has resulted in regulation that provides little good while imposing great cost. Continued economic growth and progress toward healthier, more comfortable lives depend on eliminating those regulations that neither deter fraud nor improve price and only serve to stymie growth and innovation.

Suggested Readings

DeWitt, C. Wallace. “Saving Securities Regulation.” National Affairs 30 (2017): 100–14.

Knight, Thaya Brook. “A Walk through the JOBS Act of 2012: Deregulation in the Wake of Financial Crisis.” Cato Institute Policy Analysis no. 790, May 3, 2016.

Mahoney, Paul G., and Julia D. Mahoney. “The New Separation of Ownership and Control: Institutional Investors and ESG.” Columbia Business Law Review 2021, no. 2 (2021): 840–80.

Rodrigues, Usha. “Securities Law’s Dirty Little Secret.” Fordham Law Review 81 (2013): 3389–437.

Schulp, Jennifer J. “IPOs, SPACs, and Direct Listings, Oh My!” RealClearPolicy, May 21, 2021.

———. “Let’s Not Backtrack on Loosening ‘Accredited Investor’ Rules.” MarketWatch, January 29, 2021.

———. “Public Comments on the Request for Public Input on Climate Change Disclosures.” June 11, 2021.

Vollmer, Andrew. “Does the SEC Have Legal Authority to Adopt Climate-Change Disclosure Rules?” Policy brief. Mercatus Center at George Mason University, August 2021.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.