Congress should

-

phase out Medicare in favor of a better system as rapidly as possible;

-

take every opportunity to cut Medicare spending;

-

give Medicare’s entire budget directly to enrollees as cash (“Medicare checks”);

-

give higher payments to enrollees with lower lifetime incomes and higher disease burdens, in a budget-neutral manner;

-

eliminate quality-suppressing regulations (e.g., community-rating price controls) and regulations that favor particular levels or types of health insurance for Medicare enrollees;

-

limit the growth of Medicare spending to gross domestic product growth (at most);

-

allow current workers to save their Medicare payroll taxes in personal, inheritable accounts that would gradually replace Medicare checks; and

-

fund any transition costs by reducing other government spending.

Since 1965, the U.S. Medicare program has denied workers the right to decide whether and how to spend their money on medical care. It has increased prices for medical care and health insurance, including for nonenrollees, and has reduced health care quality.

Congress finances Medicare spending by taxing younger workers. The program currently spends roughly $1 trillion per year to subsidize health care for 64 million enrollees who are elderly, are disabled, or who meet other criteria. In dollar terms, Medicare is the largest purchaser of medical care goods and services in the world—in part because it pays excessive prices to health care providers and wastes hundreds of billions of dollars on medical care that provides no value to enrollees.

Perhaps worst of all, Medicare is junk insurance. For more than 50 years, Medicare has had a negative impact on the quality of health care that both enrollees and nonenrollees receive. When researchers complain about fee-for-service payment, wasteful care, low-quality care, harmful care, medical errors, health care fraud, excessive profits, high administrative costs, federal deficits and debt, the time bomb of entitlement spending, special-interest influence over health care, or the lack of innovation in health care delivery, evidence-based medicine, electronic medical records, accountable care organizations, telemedicine, or coordinated care—in every case they are complaining about Medicare.

Though neither Republicans nor Democrats like to admit it, Medicare is already a voucher program that allows enrollees to choose to receive their subsidy either through a government-run health plan (traditional Medicare) or private insurers (Medicare Advantage).

The key to improving health care for Medicare enrollees and reducing the burden Medicare imposes on taxpayers is to make that voucher explicit and as flexible as possible—that is, to subsidize Medicare enrollees with cash and trust them to spend it, just as Social Security does.

A Result, and a Font, of Government Failure

Congress created Medicare in 1965 to fix a problem that Congress itself caused. By 1964, private health insurance that covered workers into retirement was widely available. More than 70 insurance companies offered such coverage and “many Americans over sixty‐five were covered by health insurance policies that were guaranteed renewable for life.” Yet only one-third to one-half of seniors had meaningful health insurance. Why?

For 45 years leading up to 1965, the federal tax code penalized workers if they purchased seamless health insurance plans that covered them into retirement. In 1964, the federal government wrote, “Several factors contribute to th[e] lack of coverage among elderly people,” in particular, “many of these persons who had insurance coverage before retirement were unable to retain the coverage after retirement … because the policy was available to employed persons only.” (See “The Tax Treatment of Health Care.”)

Rather than fix the underlying problem that Congress itself created, Congress created Medicare, which made the underlying problem worse.

Low-Quality Medical Care

Much of the $1 trillion Medicare spends goes toward medical care that provides at least some value to patients. It would be difficult even for the federal government to spend that much money without producing any benefit. Yet Medicare spends vast sums on medical care that provides little or no benefit to patients. Medicare subsidies encourage the consumption of low-value care, while the rules Congress attaches to those subsidies reward low-quality care and discourage many quality improvements.

An enormous portion of what Medicare spends appears to produce no benefit at all. The Dartmouth Atlas of Health Care and other research estimate that one-third or more of Medicare spending provides no value whatsoever: it makes the patient no healthier or happier. Those estimates relate to medical services that provides zero value; they do not include spending on services that provide some benefit but whose benefits are so small that the patient would rather have spent the money on something else. Including those expenditures, even more than one-third of Medicare spending is on net harmful to society.

One potential reason so much Medicare spending does not benefit patients is that Medicare has had a profound negative impact on health care quality. Medicare notoriously pays providers more for low-quality care and less for high-quality care. In 2003, the Medicare Payment Advisory Commission warned Congress: “In the Medicare program, the payment system is largely neutral or negative towards quality.… At times providers are paid even more when quality is worse, such as when complications occur as the result of error.” A 2016 study, for example, found Medicare paid low-quality hospitals an average of $2,698 more per patient than it paid high-quality hospitals.

A landmark study by economists Amy Finkelstein and Robin McKnight found that, although Medicare undoubtedly purchases some life-saving medical care, it does not appear to have saved any lives in its first 10 years and that on balance it may produce no net societal benefits:

Using several different empirical approaches, we find no evidence that the introduction of nearly universal health insurance for the elderly had an impact on overall elderly mortality in its first 10 years.… Our findings suggest that Medicare did not play a role in the substantial declines in elderly mortality that immediately followed the introduction of Medicare.

In other words, from 1966 through 1975, Medicare appears to have spent $333 billion on medical care without saving a single life. Data limitations prevented the authors from estimating any other potential health benefits from that spending. The authors nevertheless found the benefits of reducing out-of-pocket medical spending among seniors could justify no more than 40 percent of Medicare’s cost. The study raises the very real prospect that Medicare as a whole has been harmful on net to society.

Higher Taxes, Prices, Premiums, and Spending

Though Medicare heavily subsidizes medical care for enrollees, it makes health care harder for nonenrollees to afford. Medicare has dramatically increased taxes, private-sector medical prices, and premiums for private health insurance.

To keep pace with explosive Medicare spending, Congress has increased taxes on workers an average of once every two years. In part, this increase is to finance vast quantities of low- and zero-value medical care. Medicare also forces taxpayers to cover the excessive prices the program pays for low- and high-value care alike. Ambulatory surgical centers perform cataract surgeries for an average $1,000, for example, yet Medicare pays hospital outpatient departments an average $2,000 for the same services. The federal government reports, “The Medicare program pays nearly twice as much as it would pay for the same or similar drugs in other countries.” From 2010 through 2017, the excessive prices Medicare paid hospitals for evaluation and management services in just eight states cost taxpayers at least $1.3 billion and enrollees in those states $334 million.

Medicare even drives up prices in the private sector, sticking nonenrollees with higher prices for everything from drugs to physician services. Economist Martin Feldstein found that “after introduction of Medicare and Medicaid, physicians’ fees rose at 6.8 percent per year in 1967 and 1968 in comparison to a 3.2 percent annual rise in [prices],” while hospital prices increased by nearly 15 percent per year from 1966 to 1970. Those higher prices increase private insurance premiums.

Medicare also increases the volume of services nonenrollees receive, which also increases private health insurance premiums. Finkelstein found evidence that Medicare increased total hospital spending by 37 percent within five years. Much of that increase—perhaps 16 percentage points, or nearly half of the effect—was because Medicare increased hospital spending among nonenrollees. How? When the average level of insurance coverage rises, providers treat all patients more intensively. “For example,” Finkelstein writes, “if Medicare induces a hospital to incur the fixed cost of adopting a new technology, the new technology, once adopted, may also be used on nonelderly individuals.” Medicare subsidies for elderly patients thus increased prices, health spending, and insurance premiums for nonelderly patients. Finkelstein further found that “the impact of Medicare on health spending rises over the second five years of its existence.”

Efforts to improve quality or reduce spending in Medicare generally have not been successful.

Apply “Public Option” Principles to Medicare

Congress can reduce the burden Medicare imposes on taxpayers and reverse Medicare’s negative impact on quality by applying traditionally Democratic “public option” principles to the program, such that traditional Medicare and private insurers compete on as level a playing field as possible.

One consequence of the mind-boggling complexity of medicine is that no single method of paying health care providers or organizing the delivery of medical care is capable of containing all costs or rewarding all dimensions of quality. Doing both requires open competition on a level playing field between different payment rules and modes of delivery. Public-option principles demand exactly that: a level playing field where consumers are the ultimate arbiters of quality and efficiency. Heavily favoring just one method of payment or delivery system, as Medicare does, predictably and persistently leads to excessive costs, rewards certain forms of low-quality care, and discourages improvement on those dimensions of quality.

Traditional Medicare is a government-run plan that already competes against private insurers. Economist Mark Pauly explains that Medicare “is essentially a risk-adjusted voucher program” that lets enrollees choose between a public option and private Medicare Advantage plans.

That playing field, however, is anything but level. Congress bars certain plans, tilts the playing field toward excessive coverage, and tilts the field against high-quality coverage. It further violates public-option principles by offering larger subsidies to healthy enrollees if they choose Medicare Advantage while offering larger subsidies to sicker enrollees if they choose traditional Medicare.

Public-option principles demand eliminating all such distortions, including the benefits mandates and community-rating price controls Congress imposes on private health insurance plans that serve Medicare enrollees.

Most important, public-option principles require that each enrollee’s subsidy neither rise nor fall depending on which health plan, or how much coverage, the enrollee chooses. Only one type of subsidy can do that: cash.

Public-option principles thus require that Medicare mirror Social Security, which gives enrollees cash and trusts them to spend it. In 2022, Medicare will spend enough to give each enrollee an average cash subsidy of $12,100. Income- and risk-adjustment would give poorer and sicker enrollees thousands more than the average enrollee to ensure they could afford coverage.

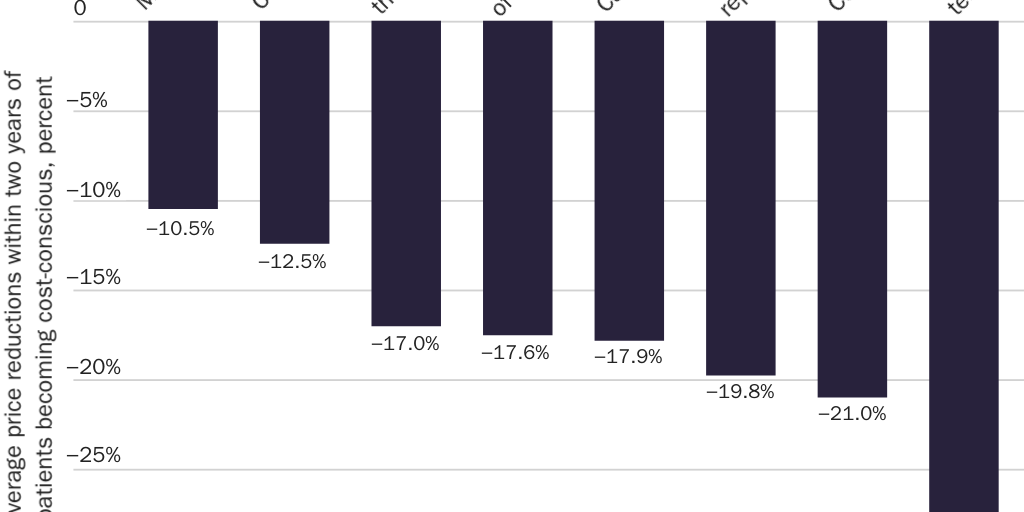

Enrollees would spend that money better than government bureaucrats do. Evidence shows that cost-conscious patients force providers to reduce prices (see Figure 1) and that when seniors control their health decisions, even those with cognitive limitations make good choices.

The size of individual enrollees’ Medicare checks should vary with health status and income. When an individual enrolls, Medicare should use competitive bidding and its current risk-adjustment program to adjust the amount of that enrollee’s check according to that individual enrollee’s health status. It should use Social Security Administration data to adjust the amount of the enrollee’s check according to the enrollee’s lifetime income. Low-income and sicker enrollees would get Medicare checks large enough to enable them to afford a standard package of insurance benefits; healthier and higher-income enrollees would get smaller checks.

Congress should restrain overall Medicare spending by limiting per-enrollee Medicare spending to gross domestic product growth. Health care prices would likely fall so dramatically that Congress could reduce Medicare spending growth even more without harming access or enrollee health.

Critics worry that if risk adjustment is imperfect, some enrollees would have insufficient funds to purchase health plans. Yet Medicare’s imperfect risk-adjustment formulas are already harming sick enrollees by punishing Medicare Advantage plans that provide high-quality coverage to those enrollees. Subsidizing enrollees with cash would benefit sick enrollees by reducing prices and creating incentives for insurers to find innovative ways to cover the sick, rather than to avoid them.

Prefund Retiree Health Care

After converting Medicare to a Social Security–like cash-transfer program, Congress should replace Medicare’s inequitable system of intergenerational transfers with a system in which workers invest their Medicare taxes in personal accounts for their health needs in retirement.

Congress should allow workers to put their full Medicare payroll tax payment (generally 2.9 percent of earnings) in a personal savings account. Workers could invest those funds in a number of vehicles and augment those funds in retirement with other savings. For most workers, those savings could replace the subsidies they receive through Medicare. Over time, Congress could make contributions to these personal accounts voluntary.

As with some Social Security reform proposals (see “Social Security”), diverting workers’ payroll tax payments into personal accounts would reduce federal revenues, making it more difficult to finance current Medicare subsidies. Public-option principles would go a long way toward solving this problem by reducing health care prices and encouraging enrollees to eliminate wasteful medical consumption, each of which would enable Congress to reduce overall Medicare outlays significantly. To the extent that these efficiency gains do not cover all transition costs, Congress should make up the gap by cutting other government spending (see “Cutting Federal Spending,” “Special Interests and Corporate Welfare,” and other chapters in this volume)—not by raising taxes.

Suggested Readings

Cannon, Michael F. “Entitlement Bandits.” National Review, July 4, 2011.

———. “M4A Would Deliver Authoritarian, Unaffordable, Low-Quality Care.” Cato Unbound, April 6, 2020.

———. “Personal Medical Accounts: An Alternative to Compulsory Health Insurance.” In Developing the Potential of the Individually Funded Pension Systems. Edited by the International Federation of Pension Fund Administrators. Santiago, Chile: International Federation of Pension Fund Administrators, 2010, pp. 173–84.

Cannon, Michael F., and Jacqueline Pohida. “Would ‘Medicare for All’ Mean Quality for All? How Public-Option Principles Could Reverse Medicare’s Negative Impact on Quality.” Quinnipiac Health Law Journal 25, no. 2 (2022): 181–258.

Early, John F. “Unplugging the Third Rail: Choices for Affordable Medicare.” Cato Institute Policy Analysis no. 871, June 6, 2019.

Hyman, David A. Medicare Meets Mephistopheles. Washington: Cato Institute, 2006.

Hyman, David A., and Charles Silver. “Paying Beneficiaries, Not Providers.” Regulation 43, no. 1 (2020): 34–39.

Pauly, Mark V. Markets without Magic: How Competition Might Save Medicare. Washington: American Enterprise Institute, 2008.

Silver, Charles, and David A. Hyman. Overcharged: Why Americans Pay Too Much for Health Care. Washington: Cato Institute, 2018.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.