State legislators should

-

eliminate government licensing of health insurance;

-

or, as preliminary steps, recognize insurance licenses from U.S. territories and other states;

-

remove all restrictions on “short-term, limited-duration” health insurance; and

-

remove “Farm Bureau” plans and “direct primary care” from the purview of state insurance regulators.

Congress should

-

repeal the Patient Protection and Affordable Care Act and other federal laws restricting health insurance choice;

-

eliminate states’ ability to use licensing laws to prevent residents from purchasing insurance from out-of-state insurers; and

-

relinquish any role as an insurance regulator.

Regulation Blocks Dependable Health Insurance

Federal and state governments impose countless regulations that increase health insurance premiums, reduce the quality of coverage for all consumers, and limit the right of consumers to purchase the health insurance plans of their choice.

Worse, the Patient Protection and Affordable Care Act’s supposed “protections” for preexisting conditions cause discrimination against the sick. Such discrimination “completely undermines the goal of the ACA.” Regulation-induced discrimination against the sick is so extensive, even “currently healthy consumers cannot be adequately insured against … one of the poorly covered chronic disease[s].”

Congress can and should make health insurance better, more affordable, and more secure by repealing the Patient Protection and Affordable Care Act (ACA, or Obamacare) and other federal health insurance regulations. States likewise can and should eliminate state-level health insurance regulations. At the very least, states should free their residents to purchase insurance from states and U.S. territories with more consumer-friendly regulations.

Community Rating: High Premiums, Junk Coverage

The heart of Obamacare’s supposed protections for patients with preexisting conditions is a requirement that insurers offer coverage to all applicants (“guaranteed issue”) and price controls on the premiums that insurers can charge (“community rating”). Guaranteed issue requires insurers to offer coverage even to applicants with preexisting medical conditions that by definition are uninsurable.

Community rating limits the ability of insurers to set premiums according to the health risk of individual enrollees. Obamacare requires insurers to cover all comers and to charge all enrollees of a given age the same premium, regardless of health status. Insurers may charge older enrollees no more than three times the youngest enrollees, even though the oldest typically cost six or seven times more. Community rating reduces premiums for enrollees with preexisting conditions at the cost of higher premiums and worse coverage for everyone else.

Obamacare’s community-rating price controls are the driving force behind the law’s rising premiums. Under Obamacare, premiums in the individual market doubled in four years, an average annual increase of 20 percent. In states like Florida, premiums continue to rise an average 12 percent per year. Women ages 55–64 saw the largest premium increases:

Total expected premiums and out of pocket expenses rose [in 2014] by 50 percent for women age 55 to 64—a much larger increase than for any other group—for policies on the federal exchanges relative to prices that individuals who bought individual insurance before health care reform went into effect.… Premiums for the second-lowest silver policy are 67 percent higher for a 55 to 64-year-old woman than they were pre-ACA.

By 2021, Congress was offering taxpayer subsidies of $12,000 to people earning $212,000 a year just to help them afford Obamacare plans.

Though the purpose of community rating is to make health insurance available to those who had never had health insurance or who lost it before they got sick, an unintended consequence is that it makes health insurance worse for everyone, even those who did purchase it before they got sick. Community rating degrades health insurance quality in several ways.

First, 83 percent of consumers value the freedom to choose when their coverage begins. Markets make this possible by allowing consumers to enroll and switch plans throughout the year. Community rating denies consumers this right by requiring insurers to sell coverage only during specific, brief periods. Outside those “open enrollment” periods, consumers may not purchase coverage. Obamacare’s community-rating price controls deny sick and healthy consumers alike the right to enroll in coverage for 9–10 months of the year. In many cases, it denies consumers coverage when they need it most.

Second, community rating penalizes high-quality coverage. Obamacare’s community-rating price controls penalize insurers if they offer high-quality coverage that attracts patients with nerve pain (penalty: $3,000 per patient), severe acne ($4,000 per patient), diabetes insipidus or hemophilia A ($5,000 per patient), substance abuse disorder ($6,000 per patient), multiple sclerosis ($14,000 per patient), infertility ($15,000 per patient), or other conditions.

The insurers who suffer those penalties are those that offer better coverage for the sick than their competitors. Community rating therefore forces insurers to eliminate health plans and plan features that sick people value to ensure that they provide worse coverage for the sick than their competitors. It even rewards insurers if they unintentionally make coverage worse for the sick, such as by not updating provider networks. If insurers fail to engage in such “backdoor discrimination,” community rating threatens them with insolvency.

The result is a race to the bottom. Researchers have shown that community rating eliminated comprehensive health plans for employees of Harvard University, Stanford University, the Massachusetts Institute of Technology, the State of Minnesota, and the federal government. In Obamacare, patient advocacy groups have identified backdoor discrimination against patients with cancer, cystic fibrosis, hepatitis, HIV, and other illnesses as community rating generates “poor coverage for the medications demanded by [sick] patients,” restricts patients’ choice of doctors and hospitals, and rewards other plan features that make coverage worse for the sick.

Community rating’s race to the bottom “undoes intended protections for preexisting conditions,” creates a marketplace where even “currently healthy consumers cannot be adequately insured,” and “completely undermines the goal of the ACA.” Community rating replaces a form of discrimination that affects few patients with an arguably worse form of discrimination that harms all patients.

Prior to Obamacare, innovations like guaranteed renewability enabled insurers to profit by building up reserves and offering quality coverage for enrollees who became ill. Community rating led insurers to give those reserves away to healthy people. Insurers will always face incentives to renege on their commitments to the sick. Community rating increases those incentives.

Finally, community rating can ultimately cause health insurance markets to collapse, leaving consumers with no way to afford medical care. It has caused the total or partial collapse, for example, of health insurance markets in California, Kentucky, Maine, Massachusetts, New Hampshire, New Jersey, New York, Vermont, and Washington.

Obamacare’s community-rating price controls caused markets for child-only health insurance to collapse totally in 17 states and partially in 22 states. Obamacare’s community-rated long-term-care insurance program collapsed before launch. The Obama administration exempted U.S. territories from community rating lest those markets collapse as well.

The only thing keeping Obamacare from completely collapsing under the weight of community rating is $79 billion in annual taxpayer subsidies, including subsidies of $12,000 for people earning $212,000 a year.

Community Rating Blocks Affordable, Secure, Quality Coverage

Community rating has destroyed innovative insurance products and prevented the development of further innovations that provide secure coverage to people who develop preexisting conditions.

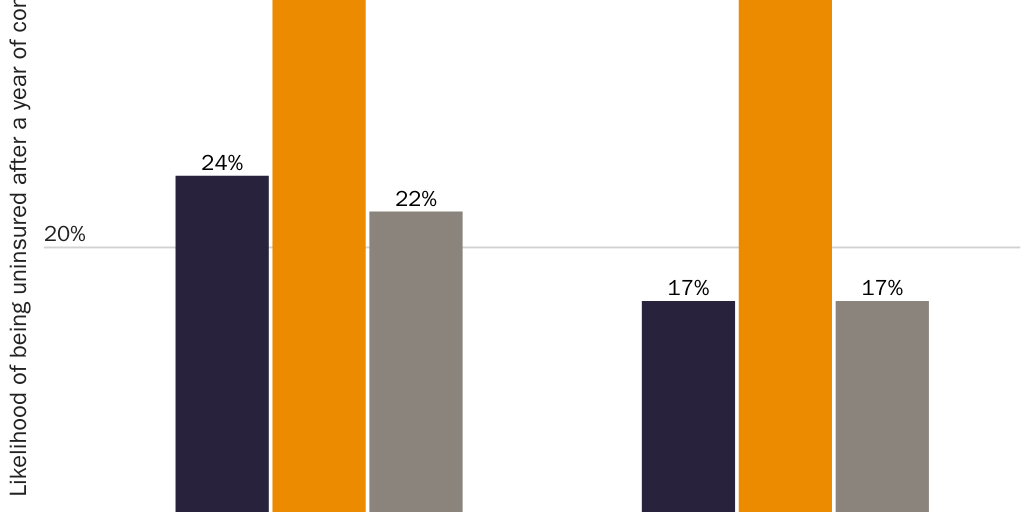

Guaranteed-renewable health insurance is an innovation that allows consumers who develop preexisting conditions to keep purchasing coverage at healthy-person premiums. Prior to Obamacare, even though insurers could deny coverage or charge higher premiums to those with preexisting conditions, consumers in poor health with guaranteed renewable coverage were less likely to lose their coverage and end up uninsured than consumers in poor health who had employer-sponsored coverage (see Figure 1). Insurers build up reserves to cover those costs. When Obamacare imposed community rating, it made guaranteed-renewable health insurance impossible and transferred resources away from the sick. Blue Cross and Blue Shield of North Carolina, for example, had accumulated a $156 million guaranteed-renewability reserve fund to cover its sickest enrollees. Community rating led the insurer to return that money to policyholders as refunds averaging $725 each—that is, to take money that markets had set aside for the sick and give it away to the healthy.

Obamacare destroyed another innovation that markets had just begun to introduce. In 2008 and 2009, insurance regulators in 25 states approved the sale of “preexisting-conditions insurance.” These products protected workers with employer-sponsored health insurance against higher premiums if they transitioned to an individual-market plan after falling ill. Like guaranteed renewability, preexisting-conditions insurance allowed those who developed an expensive, long-term medical condition to keep paying healthy-person premiums. UnitedHealth Group offered this revolutionary product for 20 percent of the cost of the underlying individual-market policy.

Community rating is blocking additional innovations. Two examples illustrate the possibilities. Law professors Peter Siegelman and Tom Baker explain how insurers could make health insurance more attractive to so-called young invincibles, and thus induce them to purchase it voluntarily, by offering cash back to people who don’t file claims. Economist John Cochrane explains how insurers could offer total satisfaction guarantees. Insurance contracts could allow sick enrollees who grow dissatisfied with their coverage to fire their insurance company, receive a large cash payout, and then choose from among other carriers who would compete to cover rather than avoid them. Markets protect the sick from incentives that insurers face to renege on their commitments. Obamacare increases those incentives.

For all the damage guaranteed-issue and community-rating regulations cause, they appear to offer little benefit when it comes to expanding coverage to the sick. After studying community rating versus unregulated markets (i.e., before Obamacare-imposed community rating in all states), economist Mark Pauly and his colleagues concluded:

We find that [community rating] modestly tempers the (already-small) relationship of premium to risk, and leads to a slight increase in the relative probability that high-risk people will obtain individual coverage. However, we also find that the increase in overall premiums from community rating slightly reduces the total number of people buying insurance. All of the effects of regulation are quite small, though. We conjecture that the reason for the minimal impact is that guaranteed renewability already accomplishes a large part of effective risk averaging (without the regulatory burden), so additional regulation has little left to change.

If Obamacare has expanded coverage, its vast subsidies for insurance companies are the reason.

Additional Harmful Regulations

State and federal governments have enacted additional health insurance regulations that harm patients.

“Any-willing-provider” laws increase prices for medical care and health insurance. Insurers frequently negotiate discounts from providers. In exchange, they steer enrollees toward those providers. More than half the states have enacted any-willing-provider laws, which require insurers to offer the same payment levels to all providers. “Any-willing-provider legislation removes the incentive to compete aggressively on a price basis,” writes health economist Michael Morrisey. “No one has an incentive to offer much of a discount since discounts will result only in lower prices with little or no expanded volume.” The results are higher prices for medical care and higher health insurance premiums.

State and federal governments make health insurance less affordable by requiring consumers to purchase coverage they do not want. Many states require consumers to purchase coverage for services that some may consider quackery, such as acupuncture, chiropractic, and naturopathy. Thirty-three states require consumers to purchase at least 40 types of mandated coverage. States have also required consumers to purchase coverage for medical treatments that later proved harmful to health, such as hormone replacement therapy and high-dose chemotherapy with autologous bone marrow transplant for breast cancer.

States impose many additional regulations on insurance pools, from premium taxes to rules that reduce insurers’ ability to limit fraud and wasteful services. The nonpartisan Congressional Budget Office has estimated that, on average, state health insurance regulations increase premiums by 13 percent. States then prevent individuals and employers from avoiding unwanted regulatory costs by prohibiting them from purchasing health insurance from jurisdictions with more consumer-friendly regulations.

Repeal Obamacare

Congress should repeal Obamacare and replace it with reforms that allow better, more affordable, and more secure health care. Premiums would fall for millions of Americans who would no longer have to buy coverage they do not want or pay the hidden taxes that further increase their premiums. Consumers could purchase coverage that is more secure than either ACA coverage or employer-sponsored insurance. They would have the option to purchase preexisting-conditions insurance, which would provide protection from the financial costs of long-term illness at a fraction of the cost of a standard health insurance plan. Consumers could look forward to the day when health insurance comes with total-satisfaction guarantees that force insurers to compete aggressively on quality.

Merely repealing Obamacare is not enough to improve quality and expand access for everyone currently receiving subsidies under its auspices. Federal and state policymakers must take additional steps (see the remainder of this chapter plus “Health Care Regulation,” “The Tax Treatment of Health Care,” “Medicare,” and “Medicaid and the Children’s Health Insurance Program”).

As Congress takes these steps to transition the U.S. health care sector from a government-run system to a market system, political necessity may require Congress to offer transitional assistance to the relatively small number who receive coverage under Obamacare but would not see their premiums fall after repeal. The block grants that “Medicaid and the Children’s Health Insurance Program” recommends could provide such assistance. If repealing Obamacare is politically infeasible at the moment, state and federal lawmakers can allow alternatives to free consumers from Obamacare’s junk coverage. Alternative coverage options can coexist alongside Obamacare, reduce its premiums by giving sicker patients a better alternative, and provide a benchmark against which to measure Obamacare’s performance.

Congress already exempts certain health plans from Obamacare’s harmful regulations. Federal law has exempted “short-term, limited-duration” insurance (STLDI) from nearly all federal regulation for decades. Such plans often cost 70 percent less than Obamacare plans and offer a broader choice of doctors and hospitals. In 2018, federal regulators clarified that the exemption is broad enough that insurers can pair these plans with renewal guarantees to provide secure, long-term coverage. (A better descriptor of such plans is “renewable, term health insurance.”) Congress should encourage insurers to enter the market and prevent future regulators from later denying consumers these choices by codifying that interpretation. States should likewise exempt such plans from their own regulations and give consumers full flexibility to take advantage of these plans. Specifically, states should let consumers (1) purchase STLDI with an initial term of up to 12 months, (2) renew the initial STLDI contract for up to 36 months, and (3) purchase stand-alone “renewal guarantees” that protect them from reunderwriting in perpetuity.

The Obama administration allowed another alternative to Obamacare. In 2014, it ruled that Obamacare’s most expensive regulations—“guaranteed availability, community rating, single risk pool, rate review, medical loss ratio and essential health benefits”—do not apply in U.S. territories. States can and should make health insurance better, more affordable, and more secure by allowing their residents (including employers) to purchase health plans available in American Samoa, Guam, the Northern Marianas Islands, Puerto Rico, or the U.S. Virgin Islands. Major insurers with networks in the 50 states—including Aetna, UnitedHealthcare, Humana, and Blue Cross Blue Shield—already do business in the territories. Restoring the right of state residents to purchase such plans would also provide an economic boost to struggling territories.

Several states allow associations of farmers (“Farm Bureaus”) to offer health insurance free from costly state regulations. Farm Bureau coverage presents another opportunity for insurers to choose lower-cost plans that provide secure coverage through innovations such as renewal guarantees, and that can therefore improve Obamacare risk pools and reduce Obamacare premiums. All states should allow Farm Bureaus and other associations to offer such coverage.

State insurance regulators often inhibit entry by defining innovations in health care delivery as insurance, and therefore subjecting them to onerous and inappropriate regulation. “Direct primary care” (DPC) allows consumers to get quicker access to primary care by paying a monthly or yearly subscription fee. Since DPC involves some pooling of medical expenses, regulators often define it as insurance. Dozens of states have enacted laws putting DPC outside the reach of insurance regulators. All states should do so.

Repeal State Insurance-Licensing Laws

State insurance-licensing laws give each state’s insurance regulators a monopoly over providing consumer protections to insurance purchasers. Regulators then do what all monopolists do: provide a low-quality product at an excessive cost.

The best solution is for states to repeal insurance-licensing laws. Full liberalization would maximize quality, affordability, and innovation. It would eliminate government’s ability to use insurance regulations to redistribute income, or to shower rents on favored special interests. Competition and government enforcement of contracts would continue to provide the financial solvency protections and other safeguards that insurance purchasers demand.

If repealing insurance-licensing laws is politically infeasible, preliminary steps could provide nearly as much benefit to consumers. Under one approach, the federal or state governments would allow individuals and employers to purchase health insurance licensed by other states. If purchasers are content with their own state’s consumer protections, they could continue to purchase a policy their state licenses. If their state imposes too many mandates, or prevents insurance pools from protecting participants from irresponsible or opportunistic behavior, they could choose an insurance plan from a state with more consumer-friendly regulations.

“Regulatory federalism” would increase competition in health insurance markets. Insurers would face lower barriers to introducing products into new states. As a result, consumers would have much greater choice among cost-saving features (e.g., cost sharing and care management), provider financial incentives (fee-for-service, prepayment, and hybrids of the two), and delivery systems (integrated, nonintegrated, and everything in between). (See “Health Care Regulation.”) Insurance pools would be more stable, and consumers would have more freedom to obtain coverage that fits their needs.

Perhaps most important, regulatory federalism would force insurance regulators to compete with one another to provide the optimal level of regulation. States that impose unwanted regulatory costs on insurance purchasers would see their residents’ business—and their premium tax revenue—go elsewhere. The desire to retain premium tax revenue would drive states to eliminate unwanted, costly regulations and retain only those regulations that consumers value. One or a handful of states would likely emerge as the dominant regulators in a national marketplace, just as Delaware created a niche for itself by offering a hospitable regulatory environment for corporate chartering, and South Dakota did the same with credit card operations.

Some critics claim that letting individuals and employers purchase coverage from other states would lead to a race to the bottom as states eager to attract premium tax revenue would eliminate all regulatory protections or skimp on enforcement. On the contrary, it is regulatory monopolies and specific regulations like community rating that create a race to the bottom. Competition prevents a race to the bottom. As producers of consumer protections, states are unlikely to attract or retain premium-tax revenue by offering an inferior product. Consumers and ultimately insurers would avoid states whose regulations prove inadequate. The first people to suffer from insufficient consumer protections, moreover, would be residents of that state, who would then demand that their legislators enact better consumer protections. Regulatory federalism would not produce a race to the bottom but a race to consumer satisfaction where states only adopt consumer protections whose benefits justify the costs.

To enforce consumer protections, states could require insurers to incorporate the licensing state’s regulations into the insurance contract. That way, consumers could enforce other states’ regulations in their own state, rather than in the state that licensed the insurance policy. Such “choice-of-law” decisions are complex but rest on extensive legal doctrine and precedent. A state’s insurance regulators could even play a role in policing and enforcing other states’ regulatory protections.

Ideally, each state would unilaterally give its residents the right to purchase insurance from any other state. All that each state and territory need do is deem insurance policies that hold licenses from other states or territories as being in compliance with that state’s laws.

A surer approach might be for Congress to act. The U.S. Constitution grants Congress the power to regulate commerce among the states largely to prevent states from erecting trade barriers that keep out products from other states. Insurance-licensing laws are a clear example of such trade barriers. Congress need not alter any state’s health insurance regulations. All that is necessary is for Congress to require states and territories to recognize the insurance licenses from other states and territories.

The Constitution does not grant Congress the power to regulate health insurance, however. Thus, the same legislation should relinquish any role for Congress as an insurance regulator. When Congress assumes that role, it becomes a monopoly provider of consumer protections. The result is high-cost, low-quality coverage that is far more difficult to dislodge than state regulation.

Any federal law aimed at regulatory federalism must do nothing more than allow consumers to purchase health insurance regulated by another state and ensure that those are the only regulations that govern. If Congress uses the opportunity to regulate health insurance itself, reform will not have been worth the effort.

Suggested Readings

Abelson, Reed. “UnitedHealth to Insure the Right to Insurance.” New York Times, December 2, 2008.

Baker, Tom, and Peter Siegelman. “Tontines for the Young Invincibles.” Regulation 32, no. 4 (2009–2010): 20–26.

Butler, Henry N., and Larry E. Ribstein. “The Single‐License Solution.” Regulation 31, no. 4 (2008–2009): 36–42.

Cannon, Michael F. “BCBSNC’s Premium Refunds Show the Perils of ObamaCare.” Charlotte Observer, October 6, 2010.

———. “Remarks Regarding Kansas Senate Bill 199—Short-Term Limited Duration Plans.” Testimony Before the Kansas House Committee on Insurance and Pensions, February 7, 2022.

Cochrane, John H. “Health‐Status Insurance: How Markets Can Provide Health Security.” Cato Institute Policy Analysis no. 633, February 18, 2009.

Pauly, Mark V., and Bradley Herring. Pooling Health Insurance Risks. Washington: AEI Press, 1999.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.