As Congress approaches the debt limit this year, legislators should consider a Better Budget Control Act (BBCA) to limit the growth in spending and the debt. Federal debt is at economically damaging levels and is growing at an unsustainable rate. Additional deficit spending threatens to make inflation worse and to reduce economic growth. A BBCA should aim to save at least $8 trillion over the next 10 years to stabilize the debt through a combination of new limits on discretionary spending, immediate reductions to mandatory programs, and reforms to Medicare and Social Security put forth by an independent commission. With a BBCA, Congress can responsibly raise the dollar-denominated debt limit without further inflating the public debt as a share of the economy.

The Budget Control Act of 2011

The last time Congress adopted a major deficit reduction deal was in 2011, following intense debt limit negotiations between then Republican House Speaker John Boehner and then Democratic President Barack Obama. The Budget Control Act of 2011 increased the debt limit, required Congress to vote on a constitutional balanced budget amendment, imposed spending limits on discretionary appropriations (separated into defense and nondefense), and set up a bipartisan fiscal commission—the Joint Select Committee on Deficit Reduction (the so‐called supercommittee).1 Should the supercommittee fail, the act imposed automatic spending cuts called sequestration.

The Budget Control Act (BCA) was a meaningful, albeit modest, attempt at making a downpayment toward a more sustainable fiscal future. At the time of enactment, the $2.1 trillion in savings required by the BCA would have reduced total federal spending by 5 percent over the following 10 years.2 A commensurate deal this year would mean reducing deficits by about $4 trillion over the next 10 years.

Yet such a deal is too small given that fiscal conditions have deteriorated significantly, especially due to massive emergency deficit spending during, and following, the COVID-19 pandemic. Congress would have to enact at least twice this level of deficit reduction to stand a chance at stabilizing the federal debt at its current share of gross domestic product (GDP). Public debt is just shy of 100 percent of GDP. Congress would have to reduce projected spending by 10 percent over the next 10 years, or by a total of $8 trillion, to stabilize debt as a percentage of GDP.

The BCA did not succeed in securing the required $2.1 trillion in deficit reduction for three main reasons: (1) Congress struck several bipartisan budget deals to raise spending above the caps established in law, without fully offsetting this higher spending with reductions elsewhere; (2) Congress abused emergency spending as a free-for-all category to increase spending above and beyond the levels agreed to in bipartisan budget deals; and (3) Congress responded to the COVID-19 pandemic with massive emergency spending at the end of the BCA’s term, undoing any earlier progress. Nevertheless, the law did initially control spending.3

A Better Budget Control Act

The Budget Control Act of 2011 suffered from several shortcomings that made it less effective than it could have been. The act was too narrow in size and scope. By placing separate limits on defense and nondefense spending, the act created the incentive to lift both limits as Republicans, who sought greater defense spending, formed alliances with Democrats, who sought greater domestic spending. By treating emergency spending as outside the spending limits, the act encouraged the abuse of emergency spending as a free-for-all to fund nonemergency objectives. By staffing the supercommittee with legislators, the act set up the commission for deficit reduction to fail, as partisan bickering and grandstanding replaced serious compromise negotiations. And while the supercommittee’s failure entailed automatic spending reductions or sequestration as enforcement, Congress only allowed sequestration to fully take place once, in 2013. Legislators cut compromise deals in future years to avoid automatic spending cuts and to increase discretionary spending beyond limits established in law.

A Better Budget Control Act (BBCA) would accomplish the following:

- Stabilize debt over the next 10 years, which would require $8 trillion in deficit reduction, by cutting discretionary and mandatory programs, limiting future spending growth, and putting in place an independent commission to reform Medicare and Social Security.4

- Enforce limits to total discretionary spending (instead of separate caps for defense and nondefense) for the next 10 years to encourage negotiations within topline spending levels (instead of encouraging the lifting of caps across categories). Congress should consider returning the topline discretionary spending level to pre-pandemic (fiscal year 2019) levels and to limit discretionary spending growth to no more than 2 percent annually.5 Congress should also consider eliminating unauthorized appropriations, ending the abuse of changes in mandatory programs (CHIMPs) to increase spending, and accounting for interest costs in legislative cost estimates.

- Account for emergency spending by tracking it and paying for it with offsetting spending reductions.6 Congress should consider accounting and paying for discretionary emergency spending that exceeds spending limits by reducing such limits over the following five years. If Congress authorized $50 billion (including interest) in emergency spending in FY 2024, Congress would subsequently reduce topline discretionary spending levels by $10 billion for the following five fiscal years (FY 2025–2029). Congress should also consider accounting and paying for mandatory emergency spending by including such spending on the pay-as-you-go or cut-as-you-go (PAYGO/CUTGO) scorecard and enforcing subsequent mandatory spending reductions.

- Establish an independent nonpartisan commission to reform Medicare and Social Security with fast-track authority.7

Stabilize the Debt

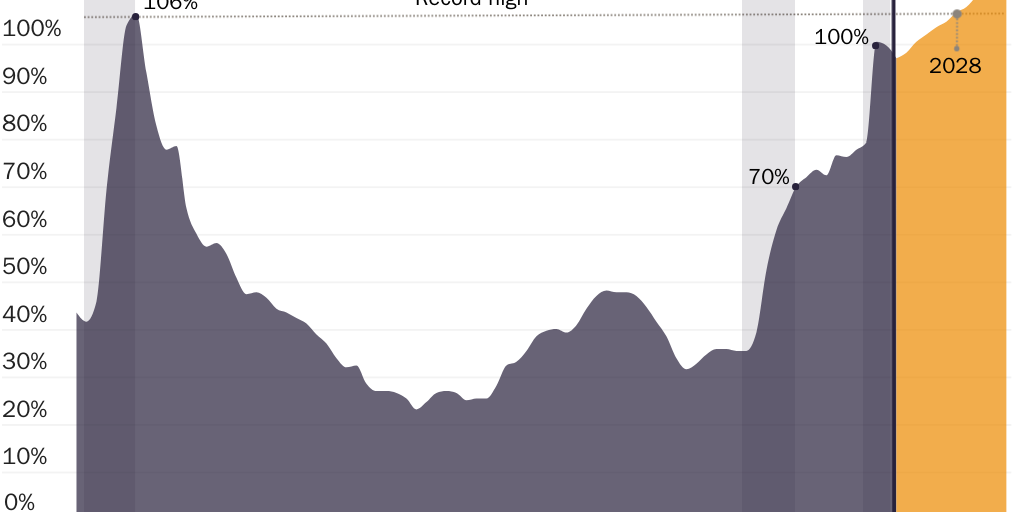

A BBCA would reduce deficit spending by at least $8 trillion over the next 10 years to stabilize the growth in the U.S. federal debt at no higher than the current level of nearly 100 percent of GDP.

According to the Congressional Budget Office (CBO), publicly held debt will exceed GDP next year. If current fiscal policy continues, publicly held debt will exceed its previous World War II record‐high of 106 percent of GDP by 2028 and rise to an unprecedented 118.2 percent of GDP by 2033 (Figure 1).

Most economic research finds that excessive public debt reduces economic growth.8 Studies focused on threshold effects identified that a debt‐to‐GDP ratio that exceeds 78 percent has a consistently negative effect on the economies of industrialized nations. High and rising debt increases interest rates, reduces incomes, crowds out private investment, and slows growth.9 It also increases the risk of a sudden fiscal crisis where bond holders lose confidence in the government’s ability or willingness to service debt without inflating away the debt’s value by reducing the purchasing power of the national currency.

Adopting a BBCA would signal to markets that the federal government takes fiscal stewardship seriously and is committed to reducing inflation and avoiding a future fiscal crisis. Such an agreement would boost economic growth and American incomes by unleashing greater investment as a direct result of reduced fiscal uncertainty.

Enforce Limits on Total Discretionary Spending

Under a BBCA, Congress would not adopt separate limits for defense and nondefense spending; instead, it would fund discretionary programs under one aggregate spending cap. This would allow for greater flexibility in funding decisions between these politically divisive categories without encouraging higher total discretionary spending. An aggregate spending limit would incentivize Congress to prioritize those funding categories of greatest import. Ideally, it would also encourage a deeper examination of the fiscal tradeoffs between current domestic discretionary funding objectives and core government priorities such as national defense.

The BCA placed separate limits on defense and nondefense discretionary spending. The resulting political dynamic strengthened the hands of big-spending politicians who secured higher defense spending levels (something Republicans supported) in exchange for higher domestic spending levels (something Democrats supported). Although politicians from both parties can be expected to advocate for higher discretionary spending, doing so within one aggregate spending limit increases the chance of legislators jockeying for a larger share of the overall amount rather than pushing up spending across the board.

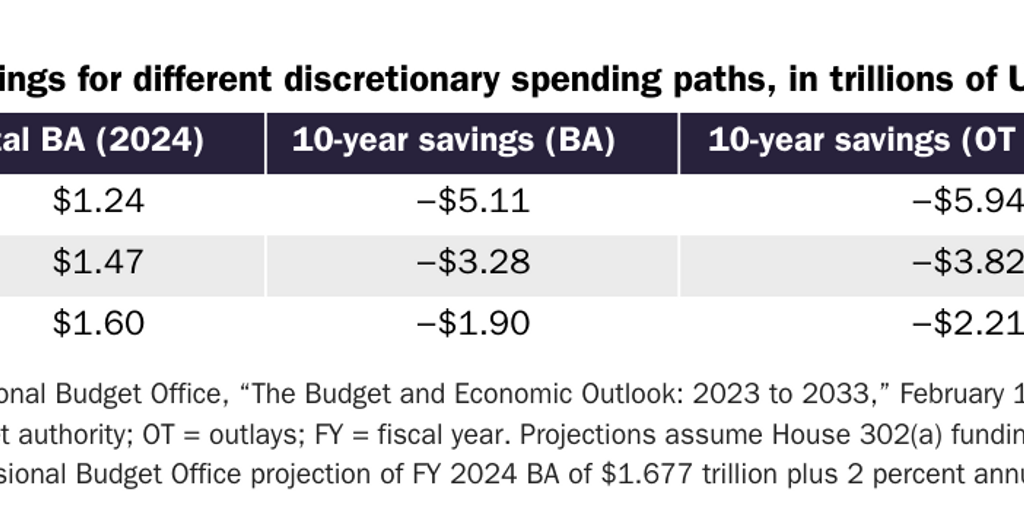

A BBCA would first reduce discretionary spending to pre-pandemic (FY 2019) levels by cutting back on programs that Congress vastly expanded during the COVID-19 pandemic. As the pandemic has ended, so should related federal government largesse.

As Table 1 illustrates, returning to pre‐pandemic discretionary levels and limiting growth to no more than 2 percent annually (beginning in FY 2024) would save American taxpayers $6 trillion over the next 10 years.

Ideally, Congress would eliminate spending that is unnecessary, wasteful, ineffective, or outside the scope of federal power under a BBCA. Spending limits encourage legislators to prioritize and to act on recommendations made by governmental and advisory groups. Unauthorized appropriations are one good source for potential savings, as Congress should either reauthorize programs that fulfill core governmental functions or eliminate them.10 Scholars at diverse think tanks have offered many good ideas for spending cuts.11 The nonpartisan CBO includes several discretionary options to reduce the federal deficit that legislators should seriously consider.12

Account and Pay for Emergency Spending

Although the Budget Control Act of 2011 limited discretionary spending, it allowed for spending above those limits if Congress designated such spending for disaster response, emergencies, and overseas contingency or war spending. While escape valves to address unexpected, sudden, and urgent needs are sensible exceptions to otherwise firm spending limits, Congress abused the allowance.

Congress should not use emergency designations to fund nonemergency objectives. Spending limits are only effective when Congress abides by them, and excluding emergency spending from such limits turned what was meant as a “in case of emergency break glass” category into a convenient way to increase spending beyond limits established in law. During the period the BCA was in effect, Congress repeatedly propped up the State Department and Defense Department budgets, using overseas contingency operations funding that did not count against spending limits. Congress also abused disaster and emergency funding designations to shore up disaster accounts to free up spending for nonemergency objectives under existing spending limits.13 Regular funding for disasters and other emergencies should be accounted for within agencies’ base budgets, reserving any additional funds for truly unforeseen, catastrophic events that fall within the responsibility of the federal government.

When Congress authorizes additional emergency spending, such spending should be accounted for by reducing future discretionary spending accordingly. In addition, new mandatory spending should be included on the relevant PAYGO or CUTGO scorecards to trigger future spending cuts. PAYGO is a statutory rule that requires Congress to pay for deficit increases from new mandatory spending or tax cuts with other mandatory spending cuts or revenue increases. CUTGO is an internal House rule that prohibits consideration of legislation that would increase mandatory spending and requires offsetting mandatory spending reductions for any violations. Emergency spending has significant implications for overall spending and debt levels. Congress has spent a combined $1 trillion through emergency supplemental appropriations over the past five years, after adjusting for inflation.14

To limit emergency spending growth in the future, Congress could adopt notional emergency spending accounts to track supplemental appropriations and enforce offsetting spending reductions. This promising approach worked well for Switzerland, as part of that country’s commitment to limit spending and debt growth with the so-called Swiss debt brake (SDB).15 When a crisis arises, Swiss legislators can spend beyond established legal limits while recording all such supplemental spending in a notional account that requires offsetting spending reductions in future years. This limits the propensity to abuse emergency spending for nonemergency objectives. The SDB provides an as-needed emergency spending valve with consequences.

Congress could apply the SDB model to the United States by accounting and paying for discretionary emergency spending by reducing discretionary spending limits over the following five years. For example, if Congress authorized $50 billion (including interest) in emergency spending in FY 2024, Congress would reduce topline discretionary spending levels by $10 billion for the following five fiscal years, from 2025 to 2029. Thus, Congress would pay for emergency spending today with lower discretionary spending tomorrow. This tradeoff makes it more likely that politicians think twice before opening the taxpayers’ purse in response to regularly recurring natural disasters and other emergencies that Congress could better plan for.

Relatedly, Congress could account and pay for mandatory emergency spending by including such spending on the PAYGO or CUTGO scorecard and enforcing subsequent mandatory spending reductions. Emergency spending that increases mandatory spending should be subject to these rules, despite Congress regularly waiving statutory PAYGO required spending reductions, including most recently in the Omnibus bill that passed in December 2023.

Establish an Independent Bipartisan Commission to Reform Medicare and Social Security

Social Security and Medicare are two of the largest federal government programs, and they are growing rapidly. Together, federal health care programs and Social Security will be responsible for 60 percent of the growth in projected spending over the next decade.16 Both programs are governed by trust funds. Medicare’s Hospital Insurance trust fund is projected to run out of borrowing authority by 2031.17 At that time, Medicare Part A providers would face an 11 percent benefit cut. Social Security’s Old‐Age and Survivors Insurance trust fund is projected to run out of borrowing authority by 2033.18 At that time, Social Security beneficiaries would face a 23 percent benefit cut.

Election-focused politicians from President Biden to House Republicans are declaring that cuts to Medicare and Social Security are off the table. And yet, these two programs are responsible for 95 percent of long-term U.S. unfunded obligations.19 Without congressional action, seniors will face indiscriminate benefit cuts when recorded trust fund balances are depleted within a decade.20 The longer legislators wait to address the unsustainable growth of Medicare and Social Security, the fewer options will remain to sensibly adjust benefits without economically damaging tax increases on American workers or sudden large benefit reductions.

An independent, nonpartisan commission can help Congress overcome entitlement reform gridlock by providing politicians with political cover to approve the necessary changes sooner. Acting sooner rather than later allows for more gradual changes to old-age entitlement programs that preserve benefits for the most vulnerable seniors without economically damaging tax increases on American workers.

The nonpartisan Government Accountability Office (GAO) surveyed entitlement reform efforts by developed, high‐income Organisation for Economic Co‐operation and Development (OECD) countries to distill lessons for U.S. policy consideration. The GAO report explains that “since the early 1990s, almost all of the 30 OECD countries restructured their pension programs, with a clear trend toward reduced benefits.”21 Several factors made a successful reform effort more likely, including

- a broad consensus across parties and groups that reform is necessary;

- the development of proposals in commissions that insulate policymakers from political risk; and

- the establishment of iterative reform processes, such as standing commissions and mechanisms to automatically adjust benefits if adopted reforms prove insufficient to achieve sustainability.

Several congressional commissions have failed, including the most recent 2011 Budget Control Act’s supercommittee and the 2010 Simpson-Bowles commission.22 One thing these failed commissions had in common is that they were composed of members of Congress who either could not overcome their political differences or whose recommendations were not adopted by the broader Congress. That is in stark contrast to another recent experience with a successful reform commission in a different, politically tricky area: the Defense Department’s Base Realignment and Closure (BRAC) commission. The BRAC commission provides important lessons for how Congress can overcome gridlock and special interest politics to achieve bipartisan entitlement reform.23

To be successful, an entitlement commission modeled on the BRAC commission should focus on achieving clearly defined goals. Such a commission should be independent and composed of citizens who follow clear criteria for their decisions. And that commission’s recommendations should have fast-track authority: they should become operative by default after the president approves them—unless Congress explicitly rejects them. This is sometimes referred to as “silent approval.”

A clearly defined goal for the entitlement commission would be to secure the 75-year solvency of the Social Security trust fund in an equitable and sensible manner that protects the most vulnerable beneficiaries while reducing benefits for higher-income earners who are able to rely on other sources of retirement income. Because all Social Security benefits are paid based on inflows into the Old-Age and Survivors Insurance and the Disability Insurance trust funds, this is a straightforward and attainable goal.

The commissioners’ goals would be more complicated with respect to Medicare because only Medicare Part A spending is governed by a trust fund. All the while, Medicare will impose unsustainable burdens on current and future taxpayers beyond Part A. As such, a clearly defined goal for the commissioners would be to focus on Medicare’s fiscal sustainability by stabilizing Medicare as a share of the economy, in an equitable and sensible manner, which would protect access to care for the most vulnerable beneficiaries, improve quality of care, and reduce subsidies for higher-income retirees who are able to pay for more of their health care costs.

To ensure the entitlement commission’s independence, the commissioners would have to be unelected appointees instead of members of Congress. That would allow elected officials to find political cover under a cloak of “following expert recommendations.” Moreover, the entitlement commission’s recommendations should reach Congress as part of one holistic package, without allowing for any amendments to prevent dilution of the reforms. Following the BRAC commission’s model, the entitlement commission’s recommendations should be submitted to the president for approval. Once approved by the president, the recommendations would be sent to Congress. Unless Congress rejects the proposal in its entirety, it should become law. Default adoption or silent approval of the commission’s recommendations in Congress matters because it allows politicians to put up a performative fight without undermining the proposal’s implementation.24

Additional Reforms

A successful BBCA would address the following ongoing concerns with the current appropriations process and fix apparent flaws in the 2011 law:

- Eliminate unauthorized appropriations. Congress regularly appropriates funding to programs with expired authorizations and to programs that were never authorized. The authorization process exists for Congress to seriously scrutinize proposed government programs. Authorizations will expire, so Congress takes a second look at current government spending and reconsiders it in light of changing priorities. By eliminating unauthorized programs as the default, Congress would face greater incentives to act on its oversight function to regularly reauthorize legitimate government functions and eliminate other programs that no longer serve federal taxpayers.

- Include interest costs in spending limit adjustment scores. Current scorekeeping conventions do not include the interest incurred from additional deficit spending in congressional cost estimates. This creates a discrepancy between the actual costs of legislation and what the CBO reports. This discrepancy distorts decision-making in favor of greater spending and higher debt accumulation. The House and Senate Budget Committees could request that the CBO include interest costs in future estimates. Better yet, a statutory requirement would ensure that all future cost estimates account for interest costs. A BBCA would hold Congress accountable for increases in spending limits or for emergencies and would specify that offsetting spending cuts must consider the total spending increase, including the associated interest.

- Prohibit the abuse of CHIMPs to increase spending. Changes in mandatory programs are a recurring budget gimmick in congressional appropriations. Most CHIMPs provide no real savings. Instead, they facilitate increases in discretionary spending without running afoul of current spending limits. A BBCA would prohibit the use of CHIMPs that provide no real outlay savings. This would eliminate one obvious loophole Congress has abused to increase spending beyond statutory intent.

Conclusion

Congress should consider a Better Budget Control Act at the debt limit this year to reduce inflationary pressures and take steps toward avoiding a future fiscal crisis. A BBCA would have to save at least $8 trillion through a combination of new limits on discretionary spending, immediate reductions to mandatory programs, and future savings from reforms to Medicare and Social Security put forth by an independent commission in order to stabilize the federal debt. Congress could responsibly raise the dollar-denominated debt limit without further inflating the public debt as a share of the economy by pursuing such a credible fiscal agreement this year. This action would signal to consumers and markets that the federal government intends to be a sound fiscal steward, which would enhance confidence in U.S. policymaking. This would boost economic growth and American incomes by unleashing greater investment as a direct result of legislators reducing uncertainty over future tax increases and inflation.

About the Author

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.